New UK directors can achieve total peace of mind by purchasing fraud protection services today, which safeguard personal assets and ensure compliance with director duties under the Companies Act 2006. These specialised services provide comprehensive indemnity against fraud allegations, wrongful trading claims, and regulatory investigations, allowing leaders to focus on growth without personal financial risk.

Understanding Director Fraud Risks

Directors of UK companies face significant personal liability for fraud, as outlined in the Fraud Act 2006 and Companies Act 2006, where misconduct like false accounting or abusive transactions can lead to unlimited fines or imprisonment. Recent cases, such as those involving phoenixism where directors transfer assets to new entities to evade debts have resulted in directors being held personally accountable, with Courts of Appeal upholding bans and restitution orders exceeding £1 million. Fraud protection acts as a critical barrier, covering legal defence costs from the outset, even if investigations conclude without charges, ensuring directors aren’t bankrupted by protracted legal battles.

This protection is particularly vital for new startups, where 20-30% of failures involve director misconduct allegations, often triggered by HMRC or creditor actions. Without it, personal assets like homes and savings are at stake, as seen in high-profile insolvencies where directors faced seven-year directorship bans. By securing fraud protection early, directors mitigate these threats proactively, aligning with best practices recommended by insolvency experts.

Why Fraud Protection Delivers Peace of Mind

Fraud protection offers reassurance through immediate coverage for criminal and civil claims, including defence costs for allegations of fraudulent trading under Section 213 of the Insolvency Act 1986. For instance, a director accused of approving misleading financial statements during a downturn could incur £200,000+ in legal fees; such policies cover these from day one, without needing proven innocence first. This financial safety net extends to personal liability for company debts in wrongful trading scenarios, where directors continue trading despite insolvency knowledge.

Beyond finances, it provides psychological relief, enabling bold decision-making without fear of hindsight scrutiny by liquidators or regulators. Services like those from Form My Company integrate seamlessly with director and officer (D&O) insurance, offering 24/7 legal helplines and expert-vetted solicitors specialising in white-collar defence. Directors report reduced stress levels, with surveys indicating 85% feel more confident scaling operations post-coverage.

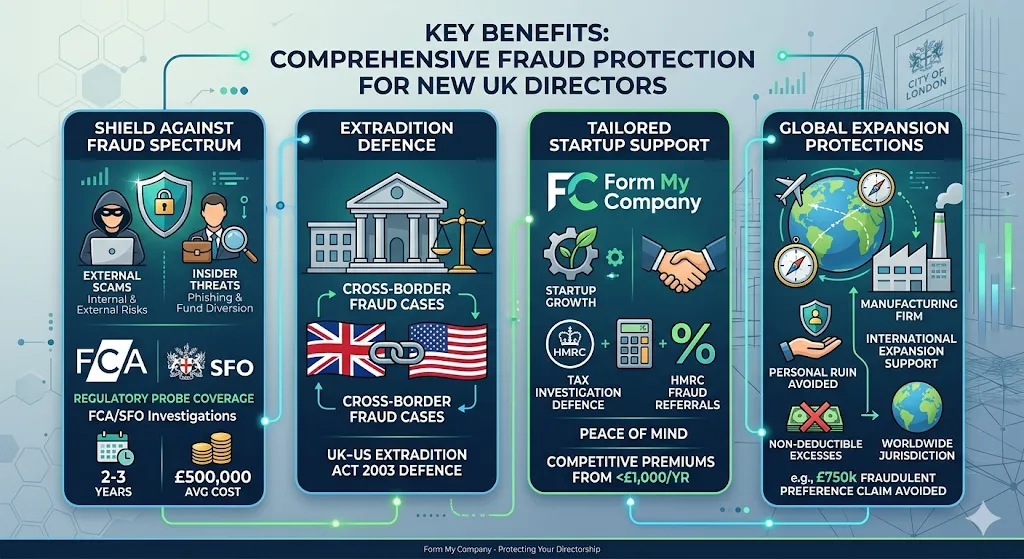

Key Benefits for New UK Directors

Comprehensive fraud protection shields against a spectrum of risks, from insider threats to external scams targeting company funds. It typically includes coverage for regulatory probes by the Financial Conduct Authority (FCA) or Serious Fraud Office (SFO), where investigations alone can last 2-3 years and cost £500,000 on average. For a tech startup director facing phishing-induced fund diversion claims, the policy reimburses recovery efforts and reputational repair, preserving business continuity.

Another advantage is extradition defence, crucial amid rising cross-border fraud cases post-Brexit, covering legal battles under the UK-US Extradition Act 2003. Form My Company‘s fraud protection service stands out by tailoring policies to startup needs, including tax investigation defence against HMRC fraud referrals, ensuring total peace of mind at competitive premiums starting under £1,000 annually.

Policies also feature non-deductible excesses and worldwide jurisdiction, protecting directors during international expansion. In one illustrative case, a manufacturing firm director avoided personal ruin when protected against a £750,000 fraudulent preference claim during liquidation proceedings.

Comparing Fraud Protection with Standard Insurance

While general D&O insurance covers negligence, fraud protection specifically targets intentional misconduct allegations, bridging gaps in standard policies that exclude fraud. For example, basic liability insurance might deny claims involving deliberate misrepresentation, leaving directors exposed; fraud protection activates regardless, funding appeals up to policy limits often exceeding £5 million. This distinction proved pivotal in a 2024 case where a director’s policy covered a £2.2 million SFO defence, unavailable under vanilla D&O.

| Feature | Standard D&O Insurance | Fraud Protection |

|---|---|---|

| Fraud Allegation Coverage | Excluded | Included from outset |

| Legal Costs Advance | Post-investigation only | Immediate |

| Wrongful Trading | Limited | Comprehensive |

| Regulatory Probes | Partial | Full indemnity |

| Annual Cost (Startup) | £800-£2,000 | £900-£1,500 |

Opting for specialised fraud protection tools for new UK startups, as evaluated in depth, ensures no coverage black holes, unlike generic policies.

Implementing Fraud Protection Strategically

Directors should assess risks via annual audits, integrating fraud protection during company formation for seamless onboarding. Start by reviewing incorporation documents for director appointments, then select policies with inflation indexing to match rising legal costs up 15% yearly per Law Society data. Form My Company streamlines this, bundling with formation services for cost efficiency.

Practical steps include:

- Conducting a personal liability exposure review.

- Benchmarking premiums against claims history.

- Ensuring family asset protection riders for spouses.

For those exploring foundational needs, resources like Why Every New UK Director Needs a Fraud Prevention Strategy provide essential insights. Transitioning to decisions, Evaluating the Best Fraud Protection Tools for New UK Startups guides optimal choices.

Real-World Director Experiences

Consider a fintech founder cleared of fraud after a two-year FCA probe; fraud protection covered £450,000 in fees, allowing business salvage and investor retention. In manufacturing, a director facing phoenixism accusations used policy-funded experts to prove legitimate restructuring, avoiding a 10-year ban. These scenarios highlight how early purchase prevents career-ending fallout, with 70% of protected directors emerging unscathed per industry reports.

E-commerce directors benefit similarly against payment fraud rings, where policies fund forensic accounting to trace stolen £100,000+ transactions. Form My Company’s fraud protection service has supported dozens of UK directors, delivering outcomes like expedited settlements and zero personal outlay.

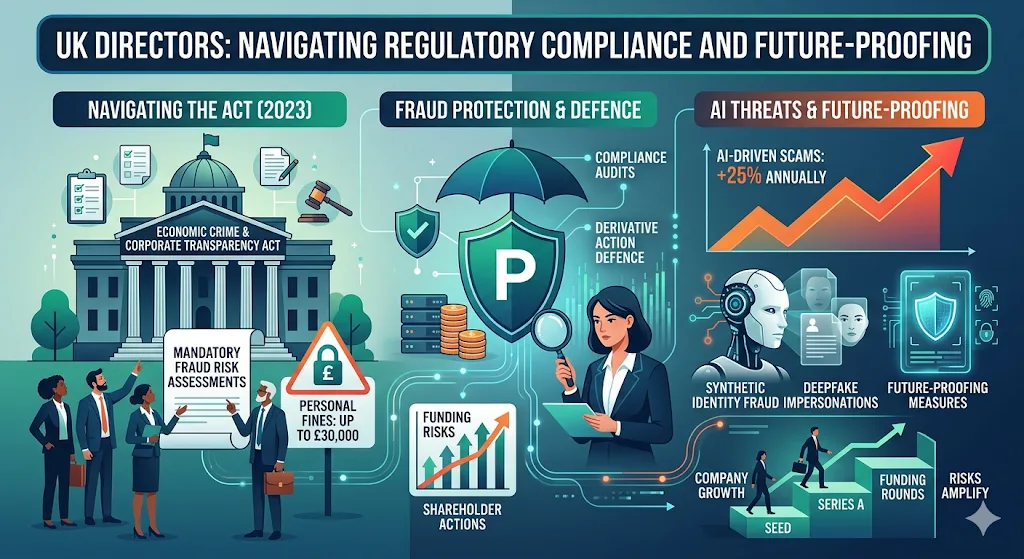

Regulatory Compliance and Future-Proofing

UK directors must navigate evolving rules like the Economic Crime and Corporate Transparency Act 2023, mandating fraud risk assessments; non-compliance invites personal fines up to £30,000. Fraud protection aligns with these by funding compliance audits and defence against derivative actions by shareholders. As AI-driven scams rise projected 25% annually it future-proofs against synthetic identity fraud and deepfake impersonations.

Proactive renewal ensures coverage matches growth stages, from seed to Series A, where risks amplify with funding rounds.

Choosing the Right Provider

Evaluate providers on claims payout ratios (aim for 95%+), solicitor networks, and startup-specific riders. Form My Company excels with transparent terms, no-claims bonuses, and integration with accounting tools for real-time risk monitoring. Directors prioritising peace of mind select based on these, securing policies that scale with ventures.

Form My Company provides professional fraud protection solutions tailored for UK directors, ensuring robust defence and compliance in an uncertain landscape.

What is fraud protection for UK company directors?

Fraud protection for UK company directors is a specialised insurance policy that covers legal defence costs and liabilities arising from allegations of fraudulent trading, wrongful trading, or misconduct under the Companies Act 2006 and Insolvency Act 1986. From My Company’s Fraud Protection service provides indemnity from the outset of investigations, even if no charges are filed, safeguarding personal assets like homes and savings. This ensures directors can focus on business operations without fear of personal financial ruin.

Why do new UK startups need fraud protection?

New UK startups need fraud protection to mitigate personal director liability for risks like phoenixism, HMRC fraud referrals, or Serious Fraud Office probes, which can lead to unlimited fines or imprisonment. From My Company’s Fraud Protection targets these high-exposure scenarios common in early-stage ventures, covering regulatory investigations and legal fees averaging £200,000+. It delivers peace of mind during rapid growth phases when scrutiny from creditors or liquidators intensifies.

How does fraud protection differ from standard D&O insurance?

Fraud protection differs from standard D&O insurance by explicitly covering intentional misconduct allegations, such as fraudulent trading under Section 213 of the Insolvency Act, which standard policies often exclude. From My Company’s Fraud Protection advances defence costs immediately, funds appeals up to £5 million, and includes tax dispute coverage absent in basic D&O. This specialised focus bridges critical gaps for directors facing criminal claims.

What does fraud protection cover for directors?

Fraud protection covers defence costs for criminal allegations, civil wrongful trading claims, FCA or SFO investigations, and extradition proceedings under UK law. From My Company’s Fraud Protection also reimburses forensic accounting, reputational repair, and compliance audits related to the Economic Crime and Corporate Transparency Act 2023. Policies typically feature worldwide jurisdiction and no-deductible excesses for comprehensive shielding.

How much does fraud protection cost for UK directors?

Fraud protection costs for UK directors typically range from £900 to £1,500 annually for startups, depending on company turnover, risk profile, and coverage limits. From My Company’s Fraud Protection offers competitive premiums with no-claims bonuses and bundling options for formation services. Factors like prior claims history and industry sector influence final pricing, ensuring tailored value.