To register a charity company in the UK, you first determine your charitable purpose, choose an appropriate legal structure—typically a company limited by guarantee—then register with Companies House and the Charity Commission. The process involves defining your objects, preparing governing documents, and ensuring trustees meet eligibility criteria. With careful preparation and compliance, your charity gains legal protections, tax reliefs, and credibility vital for securing funding and delivering public benefit.

Registering a charity company in the UK opens the door to formal recognition, tax exemptions, and public trust. Beyond heartfelt missions, incorporation transforms charitable projects into enduring institutions accountable to strict legal standards. For founders—whether social entrepreneurs, trustees, or community leaders—understanding each step ensures smooth navigation of Companies House and Charity Commission processes.

A charity company is usually a company limited by guarantee where members agree to contribute a nominal amount, such as £1, in the event of insolvency. Unlike private limited companies with shareholders, it has no share capital, preventing profit distribution. Instead, all income supports charitable aims defined in the governing documents. This model suits charities promoting education, poverty relief, community development, health, or arts.

At Form My Company, we help clients move from concept to compliance seamlessly—drafting articles of association, registering with authorities, setting up PAYE and VAT where needed, and maintaining registered offices. This guide outlines every stage in detail, ensuring your new charity launches fully compliant and ready to make an impact.

Step-by-Step Explanation: How to Register a Charity Company in the UK

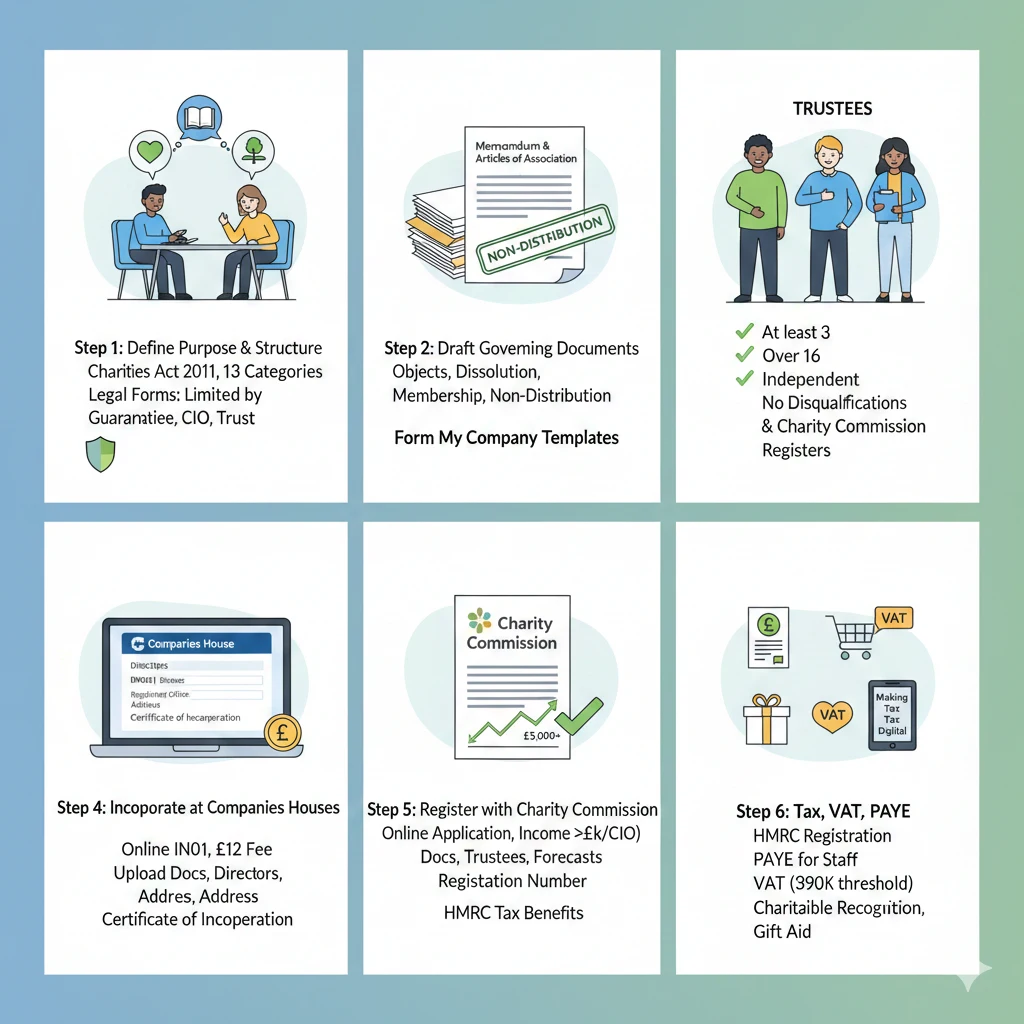

Step 1: Define your charitable purpose and structure

Under the Charities Act 2011, only organisations with exclusively charitable purposes—like promoting health, education, or environmental protection—qualify for registration. Founders should articulate objectives within these 13 recognised categories. Next, choose a legal form: most opt for a charitable company limited by guarantee, though alternatives include Charitable Incorporated Organisations (CIOs) or trusts.

If you expect significant assets or employees, incorporation protects trustees with limited liability, separating personal and organisational finances. Drafting a clear charitable purpose early avoids rejection by the Charity Commission.

Step 2: Draft your governing documents

Prepare your memorandum and articles of association. These documents state your charity’s objects, dissolution process, and membership rules. They must include a “non-distribution clause,” confirming profits serve the charity, not individuals. Form My Company provides compliant templates tailored to Commission standards to prevent costly revisions.

Step 3: Select trustees and officers

You’ll need at least three independent trustees, all over 16 years old for companies. They ensure compliance with charity law and financial prudence. Confirm no one is disqualified—such as undischarged bankrupts or individuals with unspent convictions under the Charities Act. All trustees’ details appear in both Companies House and Charity Commission registers.

Step 4: Incorporate at Companies House

Register your charity company online via the IN01 form, paying the £12 fee. Upload digital copies of your articles of association, list directors, and select a registered office address (virtual addresses offered by Form My Company meet this requirement). Upon approval, you’ll receive a Certificate of Incorporation and a unique company number.

Step 5: Register with the Charity Commission

Apply online if your annual income will exceed £5,000 or you’re a CIO. Provide evidence of charitable purpose, your governing document, trustee details, and financial forecasts. The Commission may request revisions before approval. Once registered, your charity receives a registration number, unlocking tax benefits via HMRC’s Charities Online service.

Step 6: Register for tax, VAT, and PAYE if applicable

If employing staff, register with HMRC for PAYE. For trading activities reaching the £90,000 threshold, register for VAT and maintain digital records under Making Tax Digital (MTD). Apply for Charitable Recognition with HMRC to claim Gift Aid and Corporation Tax reliefs.

This process blends legal compliance with strategic foresight. Professional support from Form My Company ensures filings meet Companies Act and Charity Commission criteria on the first submission, saving months of revisions.

Benefits and Potential Risks of Registering a Charity Company

Benefits

A registered charity company enjoys limited liability: trustees and members aren’t personally liable for debts, a critical safeguard during grant-funded projects. It also gains strong credibility—funders, corporates, and government bodies prefer registered charities due to transparency via public registers. Tax reliefs under HMRC rules include exemption from Corporation Tax on charitable trading and eligibility for Gift Aid, which increases donation value by 25%.

Additionally, incorporation provides continuity beyond individual founders, with assets owned by the company rather than trustees. Legal personhood allows property ownership, contracts, and employment without personal exposure.

Risks

Registration incurs higher ongoing regulation. Annual filings must meet both Companies House and Charity Commission standards, doubling administrative load. Trustees face legal duties under the Companies Act 2006—reporting, conflict of interest, and duty of care—or risk disqualification. Non-compliance can trigger warnings, fines, or removal from the register.

A further challenge lies in VAT. While most core charitable activities are exempt, partial exemption rules complicate reclaiming input tax for trading operations or charity shops. Strategic planning mitigates such risks, making professional formation essential from the outset.

Legal and Compliance Considerations

A charity company operates within dual frameworks: company law and charity law. It must file annual accounts, directors’ reports, and confirmation statements to Companies House within prescribed deadlines. For the Charity Commission, trustees file an annual return, trustee report, and independently examined accounts if income exceeds thresholds (e.g., £25,000).

Directors (who also act as trustees) must maintain proper governance, ensuring compliance with UK GDPR for donor records and safeguarding laws for working with vulnerable beneficiaries. Charity property management falls under the Charities Act 2022, requiring valuation for disposals.

Financial transparency is paramount: maintain distinct charity bank accounts and bookkeeping through compliant software. PAYE registration is compulsory for paid staff, and Real Time Information (RTI) must be submitted monthly. Late HMRC or Companies House filings incur penalties from £150–£1,500.

Further, your registered office address must be publicly accessible for official correspondence, although virtual office services shield personal addresses. Regular trustee training strengthens internal controls—Form My Company provides compliance dashboards helping track annual obligations automatically.

Common Mistakes to Avoid When Registering a Charity Company

The most common error is drafting vague objects in governing documents. The Charity Commission rejects submissions lacking clarity on public benefit, delaying registration. Another mistake is forming as a profit-limited company by shares instead of a guarantee company—this prevents charitable recognition altogether.

Other pitfalls include:

- Appointing trustees without eligibility checks, disqualifying your application.

- Listing a personal residence as a registered office, risking privacy and mail loss.

- Failing to distinguish charity and trading activities, leading to VAT or HMRC confusion.

- Submitting inconsistent financial forecasts, which undermines public benefit claims.

A real-life example: a community arts group applied with ambiguous objectives (“supporting culture”). The Commission requested revision three times, delaying funding by six months. Precision and expert documentation ensure faster approvals. At Form My Company, our incorporation specialists pre-screen all documents to eliminate such errors and future-proof compliance.

Practical Tips and Best Practices

Start with strategic clarity—define charitable goals in measurable terms, such as “advancing arts education for youth in Cambridge.” Draft articles using standard Charity Commission models but customise rules for quorum or trustee rotation.

Appoint a qualified treasurer early to manage budgeting and forecasts. Set up a dual-approval banking system for transparency. Use cloud accounting tools for VAT MTD and streamline RTI submissions for PAYE. Schedule AGMs annually and document minutes digitally, maintaining version control on shareable cloud drives.

Apply early for HMRC Gift Aid recognition; delays can forfeit months of reclaimable donations. Maintain insurance coverage—public liability, trustee indemnity, and event policies. For growth, consider forming a subsidiary limited company for commercial trading under charity ownership. This blend balances compliance with income diversification.

For credibility, maintain a virtual registered office and professional correspondence through Form My Company, ensuring all regulatory notices reach you securely.

FAQs

Who can register a charity company in the UK?

Anyone over 16 can start a charitable company, provided it meets public benefit criteria under the Charities Act 2011 and employs at least three independent trustees who manage its operations responsibly.

How much does it cost to register?

The Companies House fee is £12 for online submission. Professional legal drafting and compliance services, such as Form My Company’s packages, typically range from £150–£400, covering articles and filing.

Do charities pay tax in the UK?

No, registered charities are exempt from Corporation Tax on charitable income. They may still need VAT or PAYE registration for staff and trading.

Can a charity trade?

Yes, but trading must further charitable objectives or occur through a taxable subsidiary. Clear separation prevents breaching charitable status.

What’s the main difference between a CIO and a charity company?

A CIO (Charitable Incorporated Organisation) registers only with the Charity Commission, reducing paperwork but limiting flexibility. A charity company registers with both Companies House and the Charity Commission, offering stronger recognition with wider funding options.

Registering a charity company in the UK requires careful planning, from selecting charitable objects to fulfilling dual compliance with Companies House and the Charity Commission. The process rewards diligence with credibility, limited liability, and access to tax-efficient funding—all reinforcing public trust.

If you’re ready to register your company with confidence, Form My Company provides fast, fully online company formation with expert compliance support, VAT & PAYE setup, virtual office solutions, and professional guidance. Get started today and let our specialists handle the paperwork while you focus on growing your business.