Registering for VAT and PAYE in the UK is mandatory when your taxable turnover exceeds £90,000 or you hire employees, respectively. The process is fully online via HMRC’s Government Gateway, typically taking 10-30 days for approval. Follow our detailed guide to complete registrations accurately while aligning with Companies House compliance for seamless company formation.

VAT and PAYE registrations form the cornerstone of tax compliance for UK limited companies, ensuring directors and shareholders meet HMRC obligations from the outset. VAT applies to most goods and services once your taxable turnover hits the £90,000 threshold, while PAYE becomes essential upon employing staff, covering income tax, National Insurance, and pension contributions. For new businesses post company formation, timely registration prevents penalties and supports cash flow through reclaimable input tax.

Entrepreneurs often overlook how these tie into broader structures: your registered office receives HMRC correspondence, directors authorise submissions, and shareholders monitor financial health. With over 1.5 million VAT-registered firms and millions more on PAYE, non-compliance risks fines up to 100% of tax due, plus reputational damage. This guide, grounded in HMRC guidelines and the Finance Acts, empowers business owners to navigate registrations confidently, integrating with Companies House filings for holistic compliance.

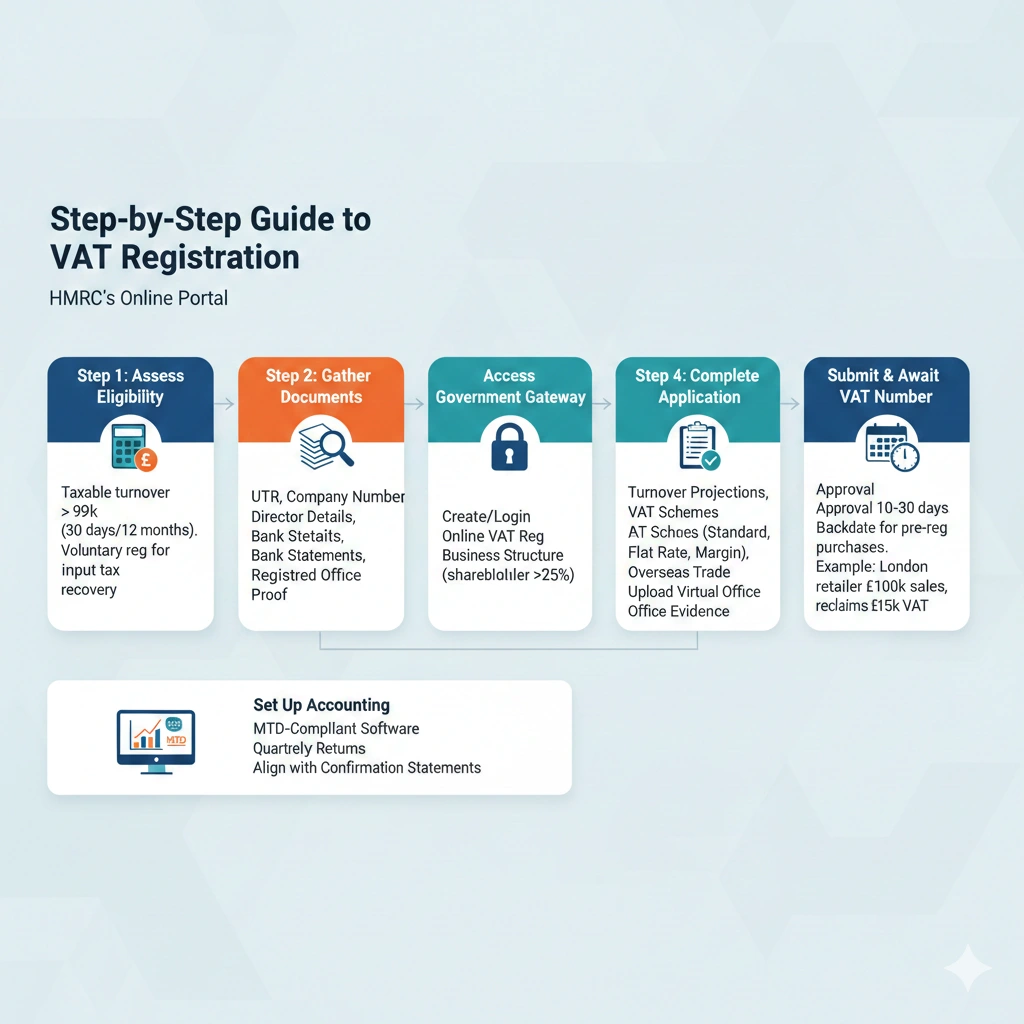

Step-by-Step Guide to VAT Registration

VAT registration follows a precise online process via HMRC’s portal, crucial for scaling businesses.

Assess eligibility. Calculate expected taxable turnover over the next 30 days alone or 12 months combined; exceeding £90,000 mandates registration within 30 days. Voluntary registration below threshold allows input tax recovery ideal for exporters or high-cost startups.

Gather documents. Prepare your Unique Taxpayer Reference (UTR) from HMRC post-self-assessment, company number from Companies House, director details, and bank statements proving registered office legitimacy. Step 3: Create or access Government Gateway. Register for VAT online, providing business structure info like shareholder percentages if over 25% control.

Complete the application. Detail turnover projections, VAT schemes (standard, flat rate, or margin), and overseas trade status. Upload evidence for virtual offices.

Submit and await VAT number. Approval arrives in 10-30 days; backdate if needed for pre-registration purchases. Example: A London retailer projecting £100,000 sales registers voluntarily to reclaim £15,000 setup VAT.

Set up accounting. Choose Making Tax Digital (MTD)-compliant software for quarterly returns. This ensures alignment with confirmation statements, reflecting accurate financials.

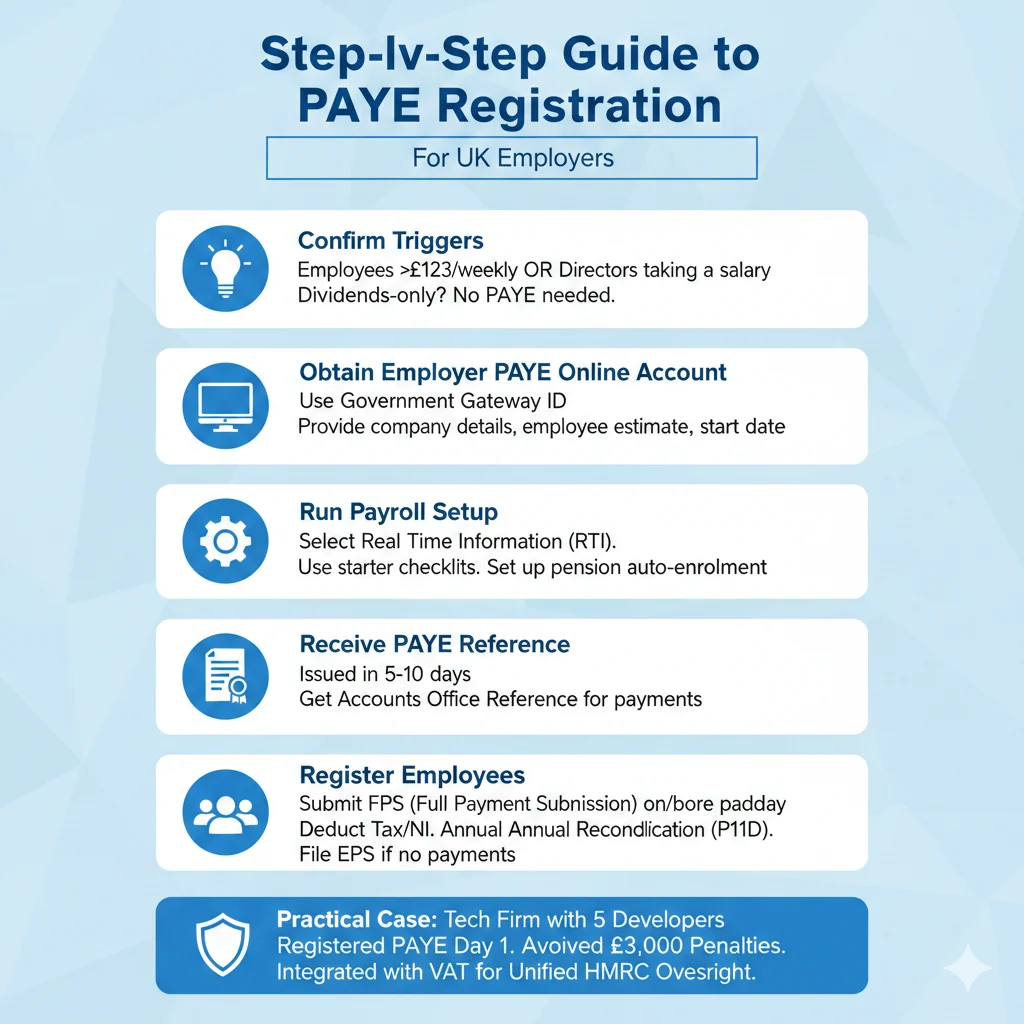

Step-by-Step Guide to PAYE Registration

PAYE registration activates when employing staff, including directors taking salaries.

Confirm triggers. Any employee earning over £123 weekly requires it; sole directors on dividends alone skip unless paying themselves salary.

Obtain Employer PAYE Online account. Use your Government Gateway ID, entering company details, estimated employee numbers, and start date. Step 3: Run payroll setup. Select Real Time Information (RTI) submissions, starter checklists for new hires, and pension auto-enrolment compliance.

Receive PAYE reference. Issued within 5-10 days, alongside accounts office reference for payments. Step 5: Register employees. Submit FPS (Full Payment Submission) on or before payday via RTI, deducting tax/NI. Reconcile annually. File EPS if no payments due, syncing with P11D for benefits.

Practical case: A tech firm with five developers registers PAYE day one, avoiding £3,000 penalties by RTI compliance. Integrate with VAT systems for unified HMRC oversight.

Benefits and Potential Risks

VAT and PAYE registrations unlock key advantages while demanding vigilance. Benefits: VAT registration enables 20% input reclaim on purchases, boosting cash flow e.g., a construction firm reclaims £50,000 yearly. PAYE formalises payroll, attracting talent and enabling R&D tax credits. Compliance enhances credibility with banks reviewing Companies House data for loans.

Integrated registrations streamline audits, as HMRC shares info with Companies House on director changes. Growing firms gain scalability, with flat-rate VAT simplifying admin for turnovers under £150,000.

Risks: Late VAT registration triggers retrospective liability, plus 2-15% penalties; voluntary deregistration below £88,000 is possible but forfeits reclaims. PAYE errors like under-deducted NI incur employer liability, with fines up to £3,000 per employee. Deregistration mishaps disrupt refunds, while HMRC enquiries tie up resources. Proactive management mitigates these, preserving shareholder value.

Legal and Compliance Considerations

Governed by the VAT Act 1994 and Income Tax (Earnings and Pensions) Act 2003, registrations impose director duties under Companies Act 2006 for accurate records. HMRC’s MTD for VAT mandates digital quarterly submissions from 2022, with fines for non-compliance. PAYE’s RTI requires payday reporting, with automatic £100-£400 penalties per late FPS.

Linkages abound: Update registered office changes via Companies House AR01 to avoid missed HMRC notices; PSC registers influence control disclosures in applications. Finance Act 2024 hikes late payment interest to 7.75%. Directors face personal liability for evasion, up to 100% tax-geared penalties or imprisonment.

For complex structures like holding companies, group VAT registration consolidates filings. Virtual offices must forward mail promptly per HMRC rules. Compliance extends to apprenticeships levy for payrolls over £3m, ensuring holistic adherence.

Common Mistakes to Avoid

Navigating registrations trips up many; sidestep these with insight. Delaying post-threshold: Assuming grace periods register within 30 days or face backdated charges plus penalties, as one cafe owed £20,000 unexpectedly.

Incomplete applications: Omitting bank validation or shareholder details halts processing; double-check UTR and SIC codes. Wrong scheme choice: Flat-rate suits small service firms but traps retailers with high inputs model scenarios first.

PAYE payroll gaps: Forgetting RTI for casual workers triggers £100 fines; use checklists. Ignoring updates: Director resignations require new authorisations, or submissions fail. A logistics company refiled thrice due to outdated registered office data, costing weeks.

Deregistration oversights: Dropping below thresholds without notifying blocks refunds. Vigilance prevents escalation to HMRC compliance checks.

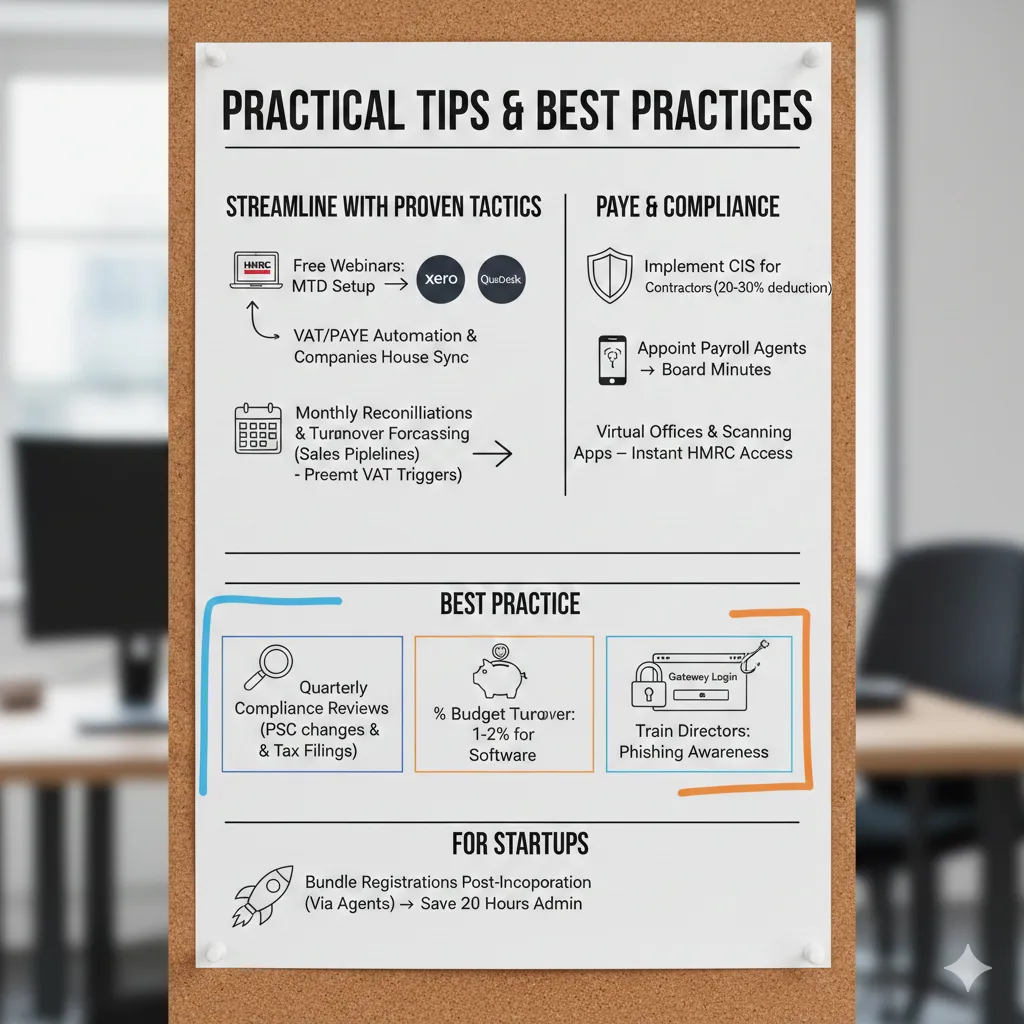

Practical Tips and Best Practices

Streamline with proven tactics. Use HMRC’s free webinars for MTD setup, integrating Xero or QuickBooks for VAT/PAYE automation syncing Companies House data. Schedule monthly reconciliations, forecasting turnover via sales pipelines to preempt VAT triggers.

For PAYE, implement CIS for contractors, deducting 20-30% at source. Appoint payroll agents for accuracy, documenting approvals in board minutes. Leverage virtual offices with scanning apps for instant HMRC access.

Best practice: Quarterly compliance reviews aligning PSC changes with tax filings; budget 1-2% turnover for software. Train directors on phishing targeting Gateway logins. For startups, bundle registrations post-incorporation via agents, saving 20 hours admin.

Mastering VAT and PAYE registrations fortifies your UK company’s compliance foundation, from company formation to ongoing operations. Timely, accurate handling protects directors, optimises cash, and scales with growth.

If you’re ready to register your company with confidence, Form My Company provides fast, fully online company formation with expert compliance support, including VAT & PAYE registrations, virtual office solutions, and professional guidance. Get started today and let our specialists handle the paperwork while you focus on growing your business.

Frequently Asked Questions

When must I register for VAT if voluntary?

Anytime below £90,000 for input recovery; ideal for capital-intensive firms. Deregister below £88,000 if ineligible, but notify HMRC 30 days prior.

Can directors avoid PAYE on salaries?

No, salaries trigger PAYE; dividends don’t, but combine strategically for tax efficiency post-NIC thresholds.

How long until I get my VAT number?

10 working days typically; expedited queries via helpline if urgent for trading.

What if turnover dips post-registration?

Apply to deregister; retain records five years. Group options consolidate for stability.

Does PAYE apply to family businesses?

Yes, if paying salaries; spouse thresholds still deduct NI/tax via RTI.