For most UK business owners earning over £40,000–£50,000 in annual profits in 2026, incorporating as a limited company (LTD) typically saves more tax than operating as a sole trader, thanks to lower corporation tax rates and flexible profit extraction via salary and dividends. Sole traders face higher income tax and National Insurance on all profits, which escalates quickly in higher bands. However, below this threshold, sole trader simplicity often wins with fewer compliance costs.

Choosing between a limited company and sole trader structure profoundly impacts your tax bill, liability, and administrative burden when starting or scaling a business in the UK. In 2026, with Making Tax Digital (MTD) fully mandatory for sole traders’ income tax self-assessment and frozen tax thresholds squeezing personal allowances, tax efficiency becomes even more critical for entrepreneurs. A limited company, registered with Companies House, offers a separate legal entity status, shielding directors’ personal assets and enabling corporation tax at 19–25% on profits up to £50,000, compared to sole traders’ progressive income tax rates of 20–45% plus Class 4 NICs.

This decision hinges on your projected profits, growth plans, and risk tolerance. For instance, a consultant earning £60,000 as a sole trader might pay around £14,000 in taxes, while the same profits in an LTD could drop to £9,500 through optimal salary/dividend splits yielding over £4,500 in savings annually. Semantic factors like VAT registration (mandatory over £90,000 turnover), PAYE for directors, and Companies House filings further differentiate structures. As experts in company formation and compliance at Form My Company, we’ve guided thousands through this choice, ensuring EEAT-aligned strategies that prioritise long-term savings and regulatory adherence. This guide breaks it down step-by-step for informed decisions.

Understanding the Structures

What is a Sole Trader?

A sole trader represents the simplest UK business structure, where you operate as a self-employed individual without forming a separate legal entity. Registration involves a quick HMRC self-assessment setup, often within weeks of trading, and requires no Companies House involvement. All profits flow directly to your personal income, taxed via Self Assessment with deadlines of 31 January and 31 July for payments on account. In 2026, MTD Phase 2 mandates quarterly updates for those above the £50,000 income threshold, increasing digital reporting demands.

Practically, this suits freelancers or micro-businesses with low overheads no need for a registered office, shareholders, or annual accounts beyond basic records. However, unlimited personal liability means business debts threaten home equity or savings. For example, a plumber with £30,000 turnover deducts £10,000 expenses (tools, van), paying tax on £20,000 profit at 20% basic rate plus 6% Class 4 NICs straightforward but inflexible. Drawbacks amplify with growth: no dividend relief, harder capital raising, and personal tax bands capping efficiency.

What is a Limited Company (LTD)?

An LTD is a distinct legal entity registered at Companies House, requiring at least one director (often the owner) and a registered office address. Formation takes 24 hours online, costing £12, with mandatory annual confirmation statements and accounts filed publicly. Profits incur corporation tax (19% up to £50,000, marginal relief to 25% beyond), leaving post-tax funds for extraction as salary (via PAYE) or dividends taxed at lower rates without NICs.

This structure demands more: appointing directors/shareholders, VAT/PAYE if applicable, and professional bookkeeping for compliance. Yet benefits shine for scaling limited liability protects personal assets to unpaid shares (often £1), credibility for B2B contracts, and tax planning like pension contributions or R&D credits. A graphic designer hitting £80,000 turnover incorporates to pay 19% corporation tax (£11,380 on £60,000 profit), then extracts £12,570 tax-free salary and £30,000 dividends at 8.75% far below sole trader equivalents. Semantic compliance like PSC registers enhances trust signals for Google rankings.

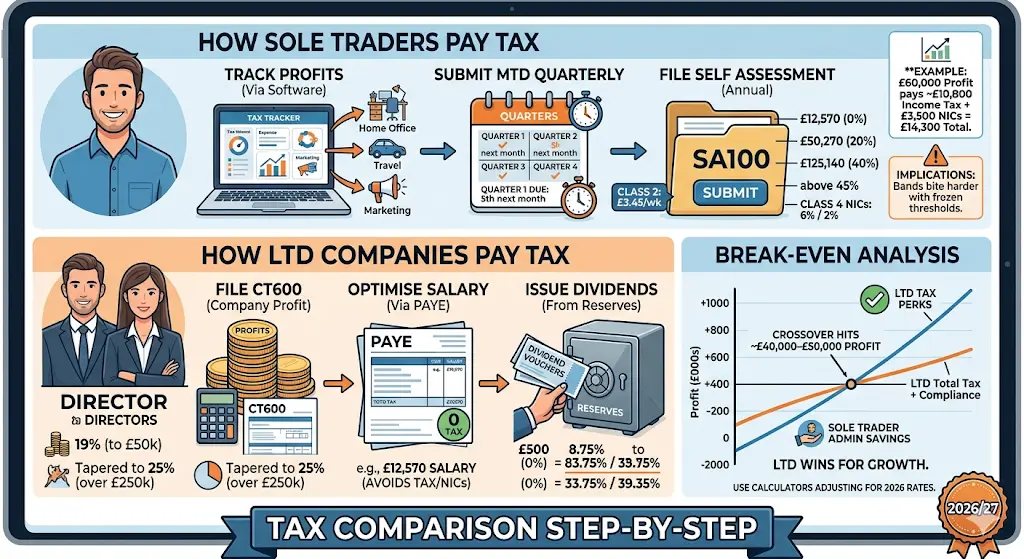

Tax Comparison Step-by-Step

How Sole Traders Pay Tax

Sole traders calculate tax on total taxable profits after allowable expenses (home office, travel, marketing). The 2026/27 personal allowance remains £12,570 tax-free, with basic rate (20%) to £50,270, higher (40%) to £125,140, and additional (45%) above. Class 4 NICs add 6% (£12,570–£50,270) and 2% thereafter; Class 2 (£3.45/week) applies over £6,725 profits. No corporation tax shield means £60,000 profit yields ~£10,800 income tax + £3,500 NICs = £14,300 total.

Step 1: Track turnover/expenses via software. Step 2: Submit MTD quarterly by 5th next month. Step 3: File annual Self Assessment. VAT kicks in over £90,000, reclaimable but adding quarterly returns. Implications: High earners lose efficiency as bands bite harder with frozen thresholds.

How LTD Companies Pay Tax

LTDs pay corporation tax on profits: 19% small profits rate to £50,000, tapered to 25% over £250,000. Directors run PAYE payroll (e.g., £12,570 salary avoids tax/NICs), then dividends from reserves (2026 allowance £500 at 0%, then 8.75%/33.75%/39.35%). Example: £60,000 profit pays £11,400 corporation tax (19%), leaving £48,600. Extract £12,570 salary (£0 tax) + £20,000 dividends (£1,750 tax) = £13,150 total tax, saving £1,150 vs sole trader.

Step 1: File CT600 annually (12 months post-period). Step 2: Optimise via low salary. Step 3: Issue dividend vouchers. VAT/PAYE integrates seamlessly for compliance.

Break-Even Analysis

Crossover hits ~£40,000–£50,000 profits; below, sole trader admin savings outweigh LTD tax perks. Use calculators adjusting for 2026 rates LTD wins for growth.

Benefits and Potential Risks

Benefits of LTD for Tax Savings

LTDs enable income splitting (salary/dividends), pension relief, and lower effective rates—ideal for directors/shareholders planning expansion. Limited liability safeguards against lawsuits, while Companies House registration boosts SEO for “trusted UK business.” Risks: Higher setup (£100–£500 accounting) and audit triggers over £10.2m turnover.

Sole Trader Advantages and Drawbacks

Simplicity no filings beyond Self Assessment suits starters, with full expense claims. Risks: Unlimited liability (e.g., client dispute claims home), tax escalation, and MTD burdens in 2026.

| Aspect | Sole Trader | LTD Company |

|---|---|---|

| Tax on £60k Profit | ~£14,300 | ~£13,150 |

| Liability | Unlimited | Limited |

| Admin Cost/Year | £200–500 | £800–1,500 |

| Growth Suitability | Low | High |

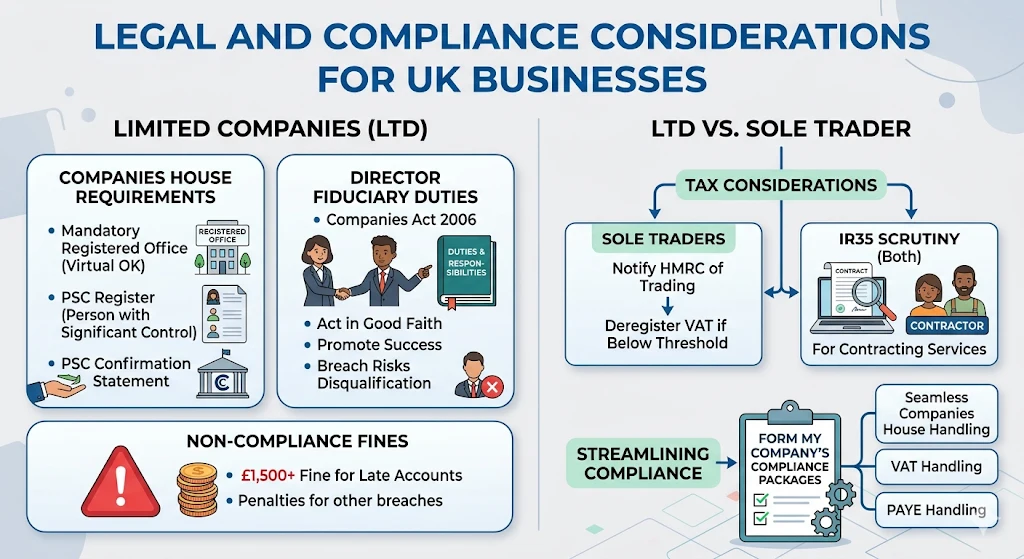

Legal and Compliance Considerations

LTDs mandate a registered office (virtual options available), PSC register, and PSC confirmation to Companies House. Directors owe fiduciary duties under Companies Act 2006; breaches risk disqualification. Sole traders notify HMRC of trading, deregister VAT if below threshold. Both face IR35 scrutiny for contractors. Non-compliance fines: £1,500+ for late accounts. Form My Company’s compliance packages ensure seamless Companies House/VAT/PAYE handling.

Common Mistakes to Avoid

Mistake 1: Sticking as sole trader past £50k overlooks LTD savings; switch via cessation/formation. Mistake 2: LTDs ignoring PAYE setup HMRC penalties up to 100% tax. Mistake 3: Mixing personal/business funds triggers audits. Mistake 4: Forgetting MTD 2026 deadlines £100+ fines. Always consult pros for tailored switches.

Practical Tips and Best Practices

Project 3-year profits; incorporate if scaling. Use accounting software (Xero/FreeAgent) for dual structures. Claim R&D for tech firms in LTDs. Time dividends pre-6 April. Maintain records 6 years. Engage accountants early for EEAT compliance.

In 2026, LTDs dominate tax savings for profitable ventures via corporation tax and extraction strategies, while sole traders excel in simplicity for low earners. Weigh liability, compliance, and growth.

If you’re ready to register your company with confidence, Form My Company provides fast, fully online company formation with expert compliance support, VAT & PAYE setup, virtual office solutions, and professional guidance. Get started today and let our specialists handle the paperwork while you focus on growing your business.

Frequently Asked Questions

When should I switch from sole trader to LTD in 2026?

Switch at £40k+ profits for tax savings, or for liability protection. Process: Inform HMRC, register LTD, transfer assets (potential CGT). Expect 2–4 weeks.

Does VAT affect the choice?

Both register over £90k; LTD reclaims input VAT easier via PAYE. No major tax swing.

Can I be a director and sole trader?

Yes, but separate activities; avoid IR35 pitfalls.

What are 2026 dividend tax rates?

£500 allowance; 8.75% basic, 33.75% higher.

How much does LTD setup cost?

£12 Companies House + £200–500 advice.