You are legally responsible for maintaining, storing, and protecting your company’s records in compliance with UK law. Failing to do so can lead to fines, investigations, or even disqualification as a company director.

Company records form the backbone of your firm’s legitimacy, credibility, and operational compliance. In an age of increasing corporate fraud and digital threats, understanding your obligations isn’t just a matter of recordkeeping it’s a safeguard for your entire business identity. This article explores what those responsibilities entail, the legal frameworks behind them, and how services like Fraud Protection from Form My Company (FMC) can help keep your business secure and compliant.

Understanding the Legal Meaning of “Company Records”

Under UK law, company records encompass all statutory, financial, and operational documentation that evidences your business’s activities. This includes details about directors, shareholders, accounting data, and key decision-making resolutions.

The Companies Act 2006 requires limited companies to maintain the following categories of records:

- Statutory registers, including the register of members, directors, persons with significant control (PSC), and secretaries.

- Accounting and financial records, which must accurately reflect all income, expenses, assets, and liabilities.

- Filing and correspondence records, including minutes of meetings, votes, and official decisions affecting company policy.

- Share and ownership documents, such as share certificates and transfer records.

Each of these must be retained for a legally defined period usually between three and six years and be accessible for inspection by HMRC, Companies House, or authorised auditors.

Why Record Protection Is a Legal Duty

Maintaining records isn’t simply an administrative best practice it is a statutory obligation. The UK’s regulatory framework demands proper data protection and accuracy because these records:

- Verify the company’s legal existence and financial integrity.

- Protect shareholders and clients from fraudulent misrepresentation.

- Enable transparency and accountability in business operations.

Failure to protect or provide records upon request may result in enforcement actions under the Companies Act, potential criminal charges, and severe financial penalties. In certain cases, directors may also face temporary or permanent disqualification.

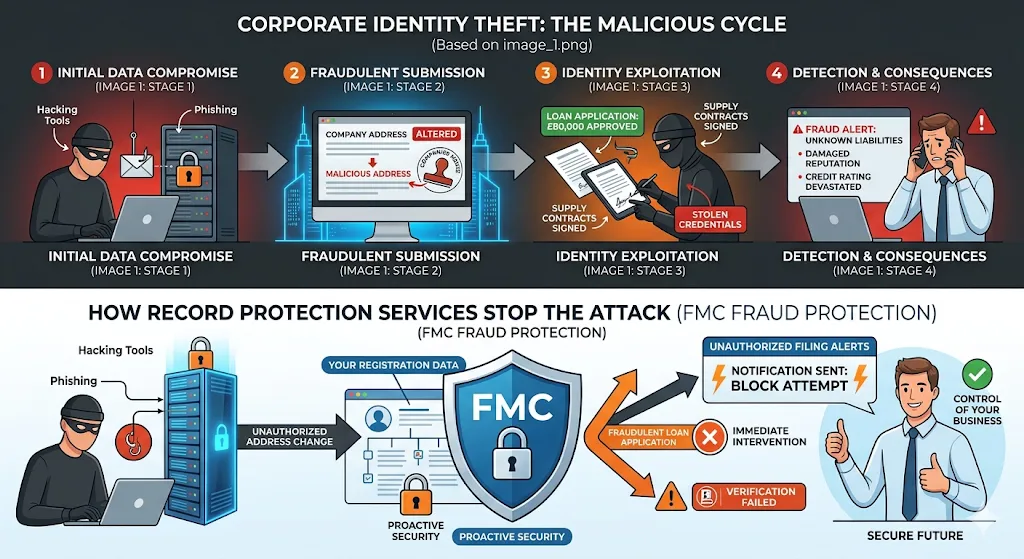

Protecting your records goes beyond compliance it defends your business identity against impersonation, unauthorised filings, and fraudulent data submissions. This is why the Fraud Protection service from FMC exists: to proactively monitor and secure your company’s online presence and registration data against these risks.

Common Misunderstandings About Record-Keeping Laws

Many directors mistakenly assume that outsourcing bookkeeping or company formation automatically covers their statutory obligations. In fact, accountability always sits with the company’s directors.

Common errors include:

- Relying solely on digital backups without secure access controls.

- Letting third-party agents manage filings without verifying updates.

- Ignoring Companies House notices or failing to update director information promptly.

UK law considers omissions as forms of non-compliance. So even if the mistake was unintentional or made by an accountant you remain legally accountable for breach of record-keeping duties.

The Connection Between Record Security and Fraud Prevention

Corporate fraud has evolved from traditional paper manipulation to digital impersonation. UK business registries have reported a rise in company identity theft, where criminals change officer details or registered addresses to access loans and contracts fraudulently.

Such cases highlight why data integrity is central to record protection. Your statutory records, if altered or accessed without authorisation, could be used to misrepresent your brand to banks, clients, or suppliers.

Services offering managed protection, like FMC’s Fraud Protection, continuously monitor your Companies House filings for unauthorised activity. They also alert you immediately if suspicious changes occur, allowing rapid preventive action. This proactive monitoring transforms compliance from a reactive requirement into a continuous layer of business security.

You can learn how this compares with self-managed methods in FMC’s related article, DIY Protection vs. Managed Fraud Services: Which is More Secure? a deeper look at the advantages of professional oversight in fraud defence.

Best Practices for Legal Record Maintenance

While many companies use accounting software or digital storage, these tools must comply with UK data-handling standards. The following best practices strengthen your legal compliance:

- Centralise Documentation – Maintain all statutory and financial records in one secure, accessible location.

- Audit Regularly – Perform periodic audits to verify data integrity and ensure filings match your internal registers.

- Implement Access Controls – Restrict edits or downloads to authorised personnel.

- Schedule Cloud Backups – Use encrypted, cloud-based solutions that comply with Data Protection Act 2018 and UK GDPR standards.

- Monitor External Changes – Use fraud monitoring tools to detect unauthorised alterations at Companies House.

These proactive measures ensure both compliance and credibility when regulators or investors review your records.

The Role of Directors and Company Secretaries

Company directors bear the ultimate legal responsibility for accurate recordkeeping. Even if you appoint a company secretary or accountant, the director must verify that statutory registers and filings remain complete and up to date.

Directors should therefore establish clear internal communication policies regarding:

- Recording board resolutions and shareholder decisions.

- Recording transactions that affect share capital or control structure.

- Reviewing confirmation statements before submission.

In many cases, directors delegate operational tasks but remain legally liable for errors. Understanding this chain of accountability helps prevent inadvertent violations and supports a culture of transparency and legal diligence.

Regulatory Bodies That Oversee Record Compliance

Several UK entities monitor company record compliance:

- Companies House: Ensures filing accuracy and transparency for all registered entities.

- HMRC: Reviews accounting records for tax compliance and auditing.

- ICO (Information Commissioner’s Office): Oversees data protection and privacy under UK GDPR.

Each body applies different standards, but all converge on one principle: directors must ensure that official data is truthful, secure, and traceable.

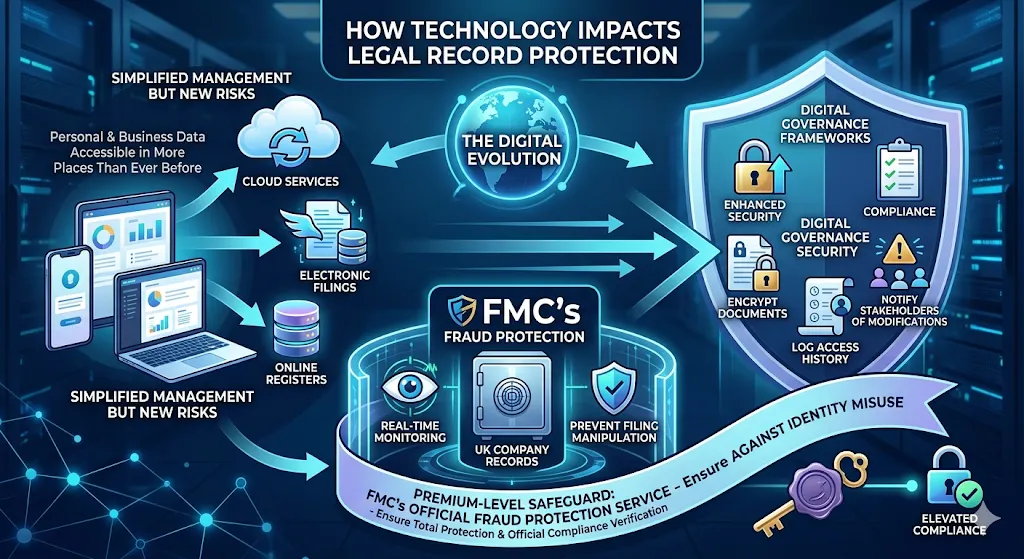

How Technology Impacts Legal Record Protection

The evolution of digital platforms has simplified company management but introduced new risks. Cloud services, electronic filings, and online registers mean personal and business data are accessible in more places than ever before.

To comply with modern regulations, firms must adopt digital governance frameworks ensuring technology enhances security rather than erodes it. Using tools that encrypt documents, log access history, and notify stakeholders of any modifications makes your company resistant to both internal and external threats.

This is where managed solutions like FMC’s Fraud Protection provide strategic value. Instead of relying solely on manual oversight, you benefit from real-time monitoring of your Companies House data, protecting against identity misuse or filing manipulation.

For companies seeking elevated compliance, you can ensure total protection and official compliance verification through FMC’s specialised service described in Ensure Full Compliance with Our Official Fraud Protection Service a premium-level safeguard for UK company records.

Consequences of Neglecting Record Responsibilities

Neglecting record maintenance is not simply poor practice it’s a legal vulnerability. Possible outcomes include:

- Financial penalties for missed filings or inaccurate data.

- Director disqualification for persistent non-compliance.

- Litigation risk, if defective records mislead shareholders or clients.

- Reputational damage, especially in regulated industries where trust and compliance are key.

The UK’s regulatory environment is strict because accuracy underpins market transparency. Whether your company is active, dormant, or newly registered, protection and compliance remain essential at all times.

Building a Compliance-First Culture

Effective record protection starts with company culture. Train employees to treat documentation and digital access responsibly. Adopt clear retention policies aligned with the UK’s statutory requirements.

Directors who demonstrate consistent attention to record security not only reduce audit risk but also reinforce investor confidence. Compliance should not be viewed as a burden it is a hallmark of professionalism and reliability.

How Form My Company Supports Record Protection

Form My Company (FMC) helps UK businesses maintain compliance through structured company services designed for transparency and security. Its Fraud Protection package provides continuous monitoring of corporate data at Companies House, automated alerts for unauthorised amendments, and hands-on guidance for restoring data integrity if compromised.

This managed protection ensures your statutory records remain accurate, legally safeguarded, and fully compliant with UK regulations. For businesses at the awareness stage (TOFU), understanding these obligations is the first step toward responsible governance before moving on to implementation through managed compliance support.

What does Fraud Protection from Form My Company include?

Fraud Protection from Form My Company monitors your company’s official records at Companies House to detect unauthorised changes in director details, addresses, or filings. The service alerts you instantly to potential identity theft or fraudulent activity, helping protect your business reputation and legal compliance.

Why is Fraud Protection important for UK-registered companies?

UK-registered companies face increasing risks of corporate identity theft, where criminals alter company information for financial gain. Fraud Protection helps prevent this by ensuring your company data remains secure, accurate, and compliant with Companies House requirements.

How does Form My Company’s Fraud Protection work?

Form My Company’s Fraud Protection uses continuous monitoring to track any updates made to your company’s official records. When suspicious changes occur, it provides immediate alerts, allowing directors to take corrective action before any damage occurs.

Can Fraud Protection help me stay compliant with Companies House?

Yes. Form My Company’s Fraud Protection service ensures all statutory records remain accurate and alerts you to any unauthorised modifications, supporting your ongoing compliance with Companies House regulations and the Companies Act 2006.

Who is responsible for protecting a company’s legal records in the UK?

In the UK, company directors have the legal duty to protect and maintain accurate records. Using oversight tools like Fraud Protection from Form My Company helps directors meet this obligation by guarding against unauthorised filings and potential data misuse.