Company formation with VAT registration in the UK involves incorporating via Companies House first, then voluntarily or mandatorily registering for VAT with HMRC if your taxable turnover hits £90,000 in a 12-month period. Form My Company streamlines both, offering seamless incorporation alongside VAT setup for immediate compliance. This dual process ensures your new limited company trades legally from day one, avoiding penalties.

Launching a business through company formation marks the gateway to limited liability protection, tax optimisation, and scalability for UK entrepreneurs. Integrating VAT registration at this stage—whether mandatory due to the £90,000 threshold or voluntary for reclaiming input tax—amplifies efficiency, especially for trading firms in e-commerce, services, or retail. Governed by Companies House for formation and HMRC for VAT, the process demands coordination: post-incorporation, your unique VAT number enables cross-border sales, cashflow boosts via refunds, and professional credibility with B2B clients. With over 1.5 million VAT-registered entities, non-compliance risks 30-day late penalties up to £400 per return, escalating to enforcement.

Directors and shareholders benefit from aligned setups—private limited companies (Ltds) dominate, appointing persons with significant control (PSCs) while linking VAT to PAYE for payroll. Recent Economic Crime and Corporate Transparency Act tweaks heighten scrutiny on accurate filings, underscoring expert guidance. Virtual offices for registered addresses complement remote operations, shielding home details publicly. This guide unpacks formation intertwined with VAT, empowering sole traders transitioning to Ltds or scaling SMEs with actionable steps rooted in GOV.UK protocols and HMRC manuals. Master these for frictionless launches amid rising digital trade demands.

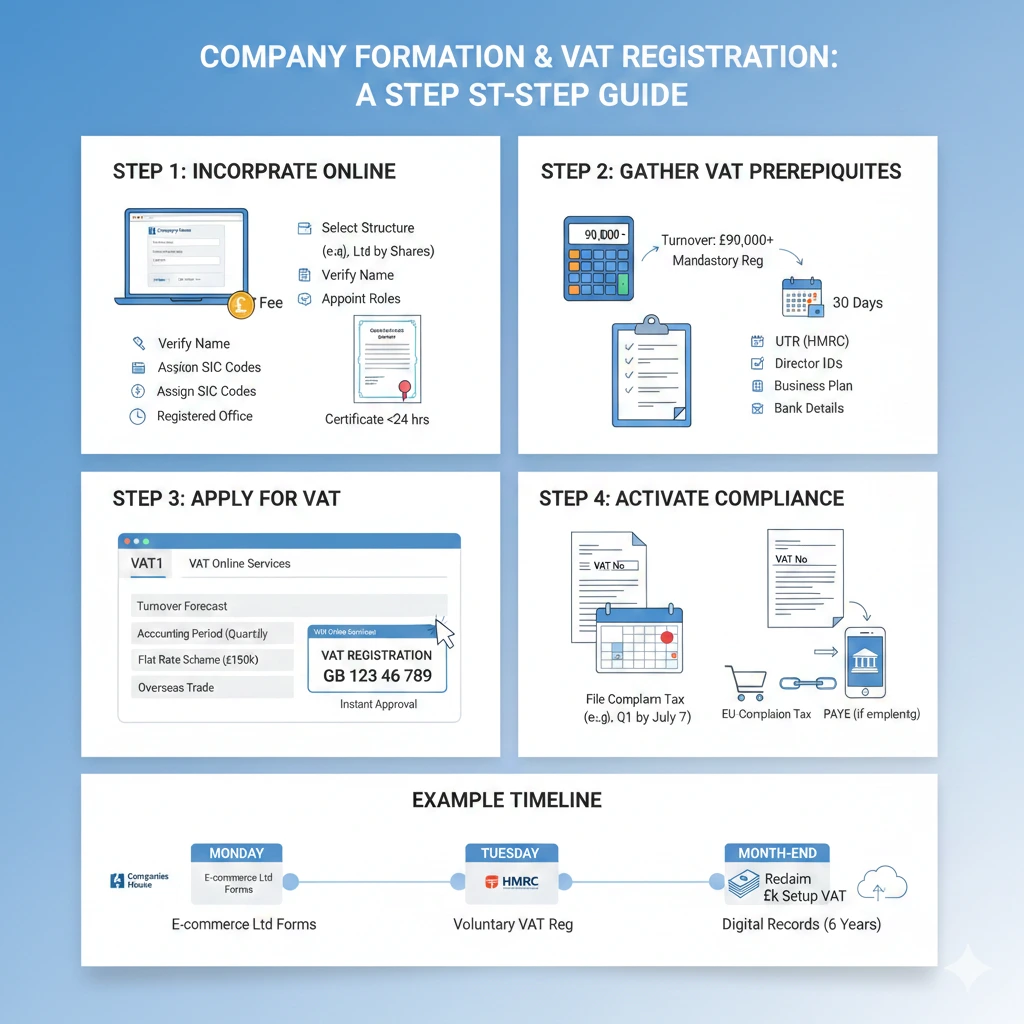

Step-by-Step Guide to Company Formation with VAT Registration

Company formation precedes VAT but integrates smoothly. Step 1: Incorporate online at Companies House (£12 fee). Select structure (Ltd by shares standard), verify name availability, appoint director(s)/shareholder(s)/PSCs, assign SIC codes, and provide registered office address. Receive certificate within 24 hours, birthing your legal entity.

Step 2: Gather VAT prerequisites. Calculate projected turnover; exceed £90,000 mandates registration within 30 days. Voluntary earlier if reclaiming VAT on purchases. Prepare Unique Taxpayer Reference (UTR) from HMRC auto-notification post-formation, director IDs, business plans, and bank details.

Step 3: Apply via VAT1 form online (VAT Online Services) or post. Detail turnover forecasts, accounting periods (quarterly standard), schemes like Flat Rate (for <£150k turnover), and overseas trade status. Approval yields VAT number instantly online, backdated if needed.

Step 4: Activate compliance. Issue VAT-compliant invoices (with registration number), file first return by period end (e.g., Q1 by July 7), pay via Faster Payments. Link to Corporation Tax, PAYE if employing. Example: E-commerce Ltd forms Monday, registers VAT voluntarily Tuesday, reclaims £5k setup VAT by month-end, trading EU-compliant immediately. Post-setup, maintain records 6 years digitally.

Benefits and Potential Risks of VAT Registration During Formation

VAT registration turbocharges new companies. Reclaim input VAT on assets (e.g., £20k office fit-out yields £4k refund), improving cashflow—critical for startups pre-revenue. Voluntary registration accesses Flat Rate Scheme (FRS): charge 20% output but pay reduced % (e.g., 14.5% services), pocketing difference legally. B2B prestige: VAT invoices demanded by corporates; retail schemes like Margin allow antique sales tax-free on margin.

Exports zero-rate, boosting competitiveness; group registration consolidates multi-entity filers. Compliance signals HMRC trust, easing loans/bank accounts. Digital VAT for distance sales post-Brexit suits online firms.

Risks counterbalance: Mandatory threshold traps unwary—miss 30-day window, retrospective liability plus interest. Increased admin burdens quarterly returns, software costs (£10-50/month). Cashflow traps: output VAT collected pre-supplier payments. FRS disqualifies post-£150k, clawback risks. Penalties: late returns £100-£400, inaccuracies 30-100% tax geared. Example: Cafe Ltd registers voluntarily, reclaims £2k but misfiles Q1, pays £200 + 5% interest—salvageable with agents. Irreversible voluntary cancellation below threshold for 2 years. Professional bundling mitigates, reclaiming 80% common errors.

Legal and Compliance Considerations

HMRC’s VAT Act 1994 mandates registration if taxable supplies hit £90,000 rolling 12 months (or £88k last quarter projected). Voluntary anytime, but exceptions: no reclaim if non-business (>90% exempt). Companies House requires formation first; VAT follows via UTR.

Post-ECCTA 2023, digital gatekeeping verifies directors—false formation blocks VAT. Invoices mandatory: name, address, VAT number, rates, reverse charge for EU. Quarterly returns electronic (MTD-VAT compliant software mandatory). Partial exemption prorates input reclaim; tour operators use special schemes.

PAYE/VAT/PAYE nexus: Employing? Register simultaneously. GDPR aligns records; Making Tax Digital end-2026 mandates all VAT digital. Penalties: Behaviour £3k+, serious issue surcharges 15%. Auditors probe VAT in CT returns. Example: Property Ltd claims full input wrongly (exempt sales), HMRC denies £10k, fines 30%. Non-residents appoint fiscal reps. LLPs/partnerships mirror Ltds. Always segregate records for inspections (unannounced possible). Solicitors advise complex structures like holding companies.

Common Mistakes to Avoid

Overlooking threshold: Traders monitor monthly; ignorance invites retrospective VAT + penalties. Example: Consultancy hits £95k unaware, pays £19k backdated + £400 fine. Voluntary without need: Locked 2 years, admin overloads micro-firms.

Incorrect schemes: FRS ineligible (foreign sales >£0), or Margin misused. Invoice errors: Missing VAT number voids reclaim, client disputes. Late deregistration post-threshold drop—HMRC rejects if careless.

Bundling oversights: Formation address mismatches VAT principal place; HMRC queries. Software non-MTD: Fines from April 2026. Neglecting partial exemption: Overclaims trigger assessments. Example: Retailer forgets overseas zero-rating, overpays £3k quarterly—annual £12k loss. Director liability unlimited if evasion. PO Box addresses fail post-2024. Verify forecasts conservatively; test VAT1 thoroughly.

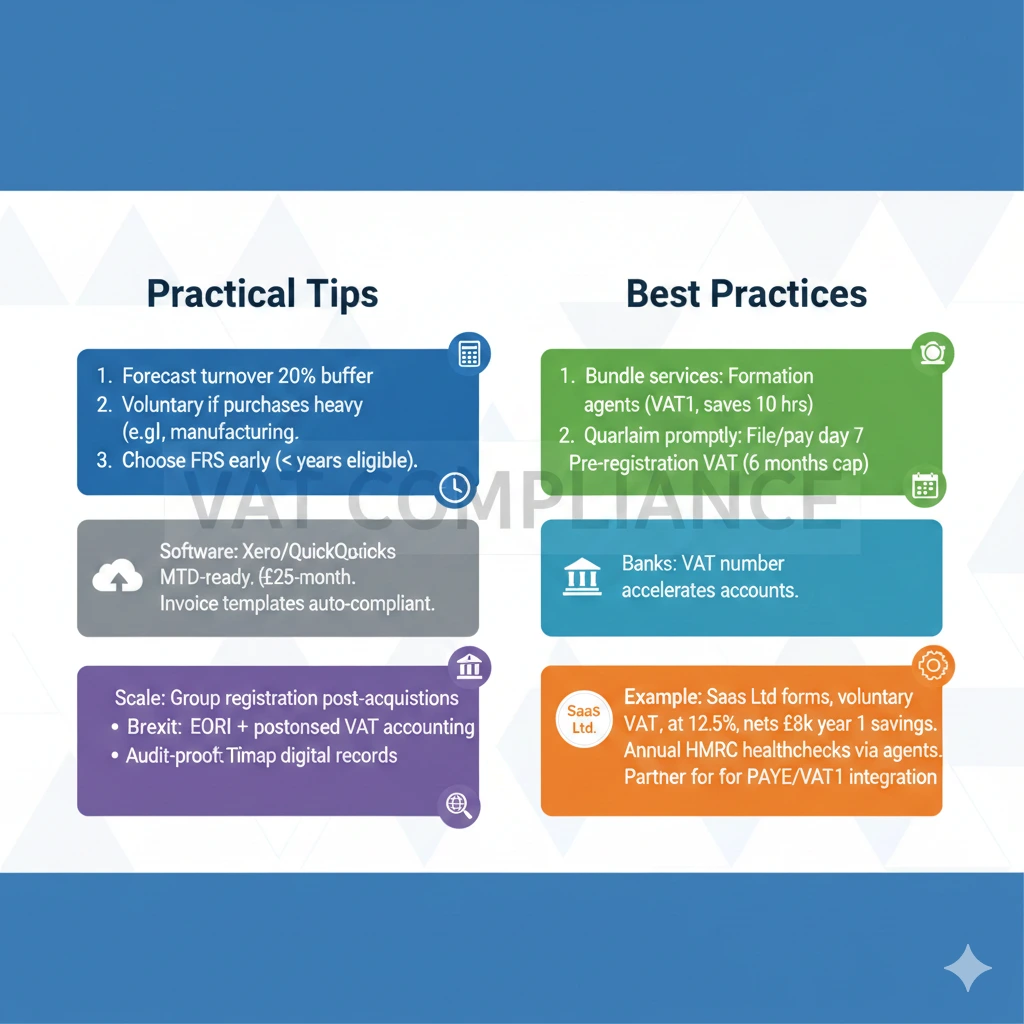

Practical Tips and Best Practices

Forecast turnover 20% buffer; voluntary if purchases heavy (e.g., manufacturing). Choose FRS early (<2 years eligible). Software: Xero/QuickBooks MTD-ready (£25/month). Invoice templates auto-compliant.

Bundle services: Formation agents handle VAT1, saving 10 hours. Quarterly diaries: File/pay day 7 post-period. Reclaim promptly: First return claims pre-registration VAT (6 months cap). Banks: VAT number accelerates accounts.

Scale: Group registration post-acquisitions. Brexit: EORI + postponed VAT accounting. Audit-proof: Timestamp digital records. Example: SaaS Ltd forms, voluntary VAT, FRS at 12.5%, nets £8k year 1 savings. Annual HMRC healthchecks via agents. Partner for PAYE/VAT1 integration.

Frequently Asked Questions

When must I register for VAT after company formation?

Mandatory within 30 days if turnover reaches £90,000 rolling 12 months. Voluntary immediately post-incorporation for reclaims. HMRC assesses projections; backdate up to 4 years 4 months if overpaid.

Can I use Flat Rate Scheme with new company formation?

Yes, if turnover <£150k. Apply on VAT1; effective from registration. Pays fixed % on VAT-inclusive turnover (e.g., 14.5% professional services). Limited cost business allowance £2k/year reclaim. Disqualifies if capital goods >£2k.

What if I miss the VAT registration deadline?

HMRC charges output tax from threshold day + late penalties (£100 min), interest 2.75%+. Retrospective up to 4 years. Mitigate via voluntary disclosure.

Does VAT registration affect Companies House filings?

Indirectly: Update PSC/service addresses if changed. CT returns include VAT summary. No direct link, but MTD integrates.

Can non-UK residents form and VAT register?

Yes, via UK registered office. Fiscal rep needed if no establishment. EORI for customs. Agents essential.

Integrating company formation with VAT registration fortifies UK ventures against compliance pitfalls, maximising reclaims and growth. Precision in thresholds, schemes, and filings underpins enduring success.

If you’re ready to register your company with confidence, Form My Company provides fast, fully online company formation with expert compliance support, including VAT & PAYE registration, virtual office addresses, and ongoing professional guidance. Get started today and let our specialists handle the paperwork while you focus on growing your business.