A UK limited company offers superior limited liability protection, tax flexibility through salary/dividend combinations, and enhanced credibility for growth, while a sole trader provides simpler setup with fewer compliance demands but full personal liability for debts. Limited companies suit businesses expecting profits over £50,000 annually, whereas sole traders fit freelancers or micro-ventures under that threshold. Choose based on your risk exposure, revenue projections and administrative tolerance.

Deciding between a UK limited company and sole trader structure shapes your business’s legal, tax and operational future, with each offering distinct advantages under current 2026 regulations. A limited company, registered via Companies House, creates a separate legal entity where directors and shareholders enjoy limited liability—protecting personal assets like homes from business debts beyond invested capital. In contrast, a sole trader merges you personally with the business, simplifying self-employment but exposing all assets to creditors.

Semantic factors like “UK limited company vs sole trader tax,” “sole trader advantages disadvantages,” and “Companies House registration requirements” drive searches as entrepreneurs weigh scalability against ease. Limited companies appeal to expanding operations needing investor funding or VAT reclaims, paying corporation tax (19–25%) on profits before dividends. Sole traders face income tax (20–45%) plus National Insurance on all earnings via Self Assessment. With Making Tax Digital for Income Tax Self-Assessment (MTDITSA) phasing in for sole traders from April 2026, administrative gaps narrow. This guide, grounded in Companies Act 2006 and HMRC rules, compares setups, taxes, risks and transitions for informed scaling.

Step-by-Step Comparison: Setting Up Each Structure

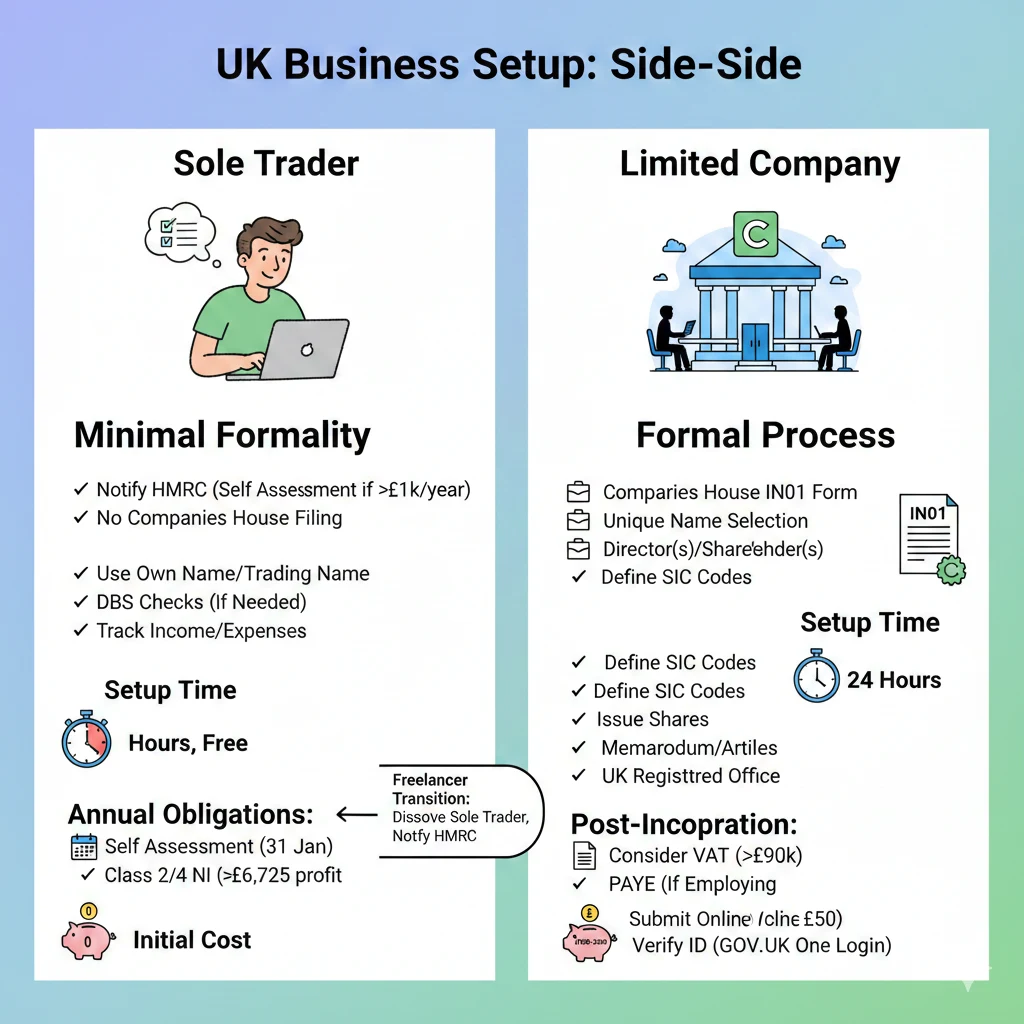

Registering as a sole trader demands minimal formality: notify HMRC via Self Assessment if earnings exceed £1,000/year—no Companies House filing, no registered office. Use your name or a trading name (register as “business name” if not personal), obtain DBS checks if needed, and track income/expenses for tax. Setup completes in hours, free, with UTR issued promptly. Annual obligations: Self Assessment by 31 January, Class 2/4 NI if profits >£6,725.

Forming a limited company requires Companies House IN01: select unique name, appoint director(s)/shareholder(s), define SIC codes, issue shares (e.g., 100x £1), draft memorandum/articles (model standard), nominate UK registered office. Submit online (£50 from Feb 2026), verify ID via GOV.UK One Login, receive Certificate in 24 hours. Post-incorporation: HMRC Corporation Tax (3 months trading), consider VAT (£90k threshold), PAYE if employing. A freelancer transitions by dissolving sole trader status, notifying HMRC—carry forward losses if qualifying. Limited setup costs £100–£300 initially, versus sole trader’s zero.

Core Benefits and Risks of Limited Company vs Sole Trader

Limited companies excel in liability protection: creditors pursue company assets only, vital for contracts risking disputes. Tax efficiency shines above £50k profits—19% corporation tax on retained earnings, dividends at 8.75–39.35% (no NI), versus sole trader’s 40%+ income tax/NI. Credibility attracts banks (easier loans sans personal guarantees), investors (SEIS/EIS reliefs), and clients perceiving professionalism. Scalability supports shareholders, pensions via company contributions.

Sole traders win simplicity: no annual accounts/confirmation statements, full profit retention post-tax, easier expense claims (e.g., home office). Risks? Unlimited liability endangers homes/savings; harder finance (personal guarantees standard); tax bands erode savings at scale (£720+ advantage to Ltd at £70k per Hoxton Mix models).

Limited risks include admin burden (Companies House filings), director duties (personal liability for wrongful trading). Sole trader risks: debt exposure, growth limits. Switch at £30–40k profits for optimal tax.

Legal and Compliance: Key Differences Explained

Sole traders report via HMRC Self Assessment: income tax (20–45%), Class 4 NI (6–9% profits), Class 2 (£3.45/week). No public register; privacy intact but MTDITSA mandates quarterly digital updates from 2026, fines £100+ for non-compliance. No VAT until £90k (voluntary reclaims inputs).

Limited companies file confirmation statements (£34), accounts (micro-entity <£632k turnover), CT600 (19–25% profits). PSC register publicises >25% owners. VAT/PAYE if thresholds met. Directors owe fiduciary duties (Companies Act 2006): diligence, conflicts avoidance—disqualification possible. 2026 changes: £50 incorporation, mandatory ID verification. Sole traders dodge corporate veil but lack separation.

Both access R&D credits, but Ltd extracts via corporation tax reliefs. Annual sole trader costs near-zero; Ltd £300–£800 accounting.

Common Mistakes When Choosing Between Structures

Many sole traders delay incorporation past £50k profits, forfeiting tax savings (£720 at £70k). Limited directors underpay salary (losing NI credits/pension relief) or over-dividend into higher bands. Sole traders claim excessive expenses (HMRC audits disallow motoring without logs). Ltd founders skip registered office (dissolution risk) or mismatch SIC codes (HMRC mismatches).

Assuming Ltd auto-saves tax ignores NI hikes; sole traders overlook MTDITSA prep. A £60k earner stays sole trader, paying £11k tax vs Ltd’s £9k. Pre-assess with calculators; consult on transitions (notify HMRC, file final Self Assessment).

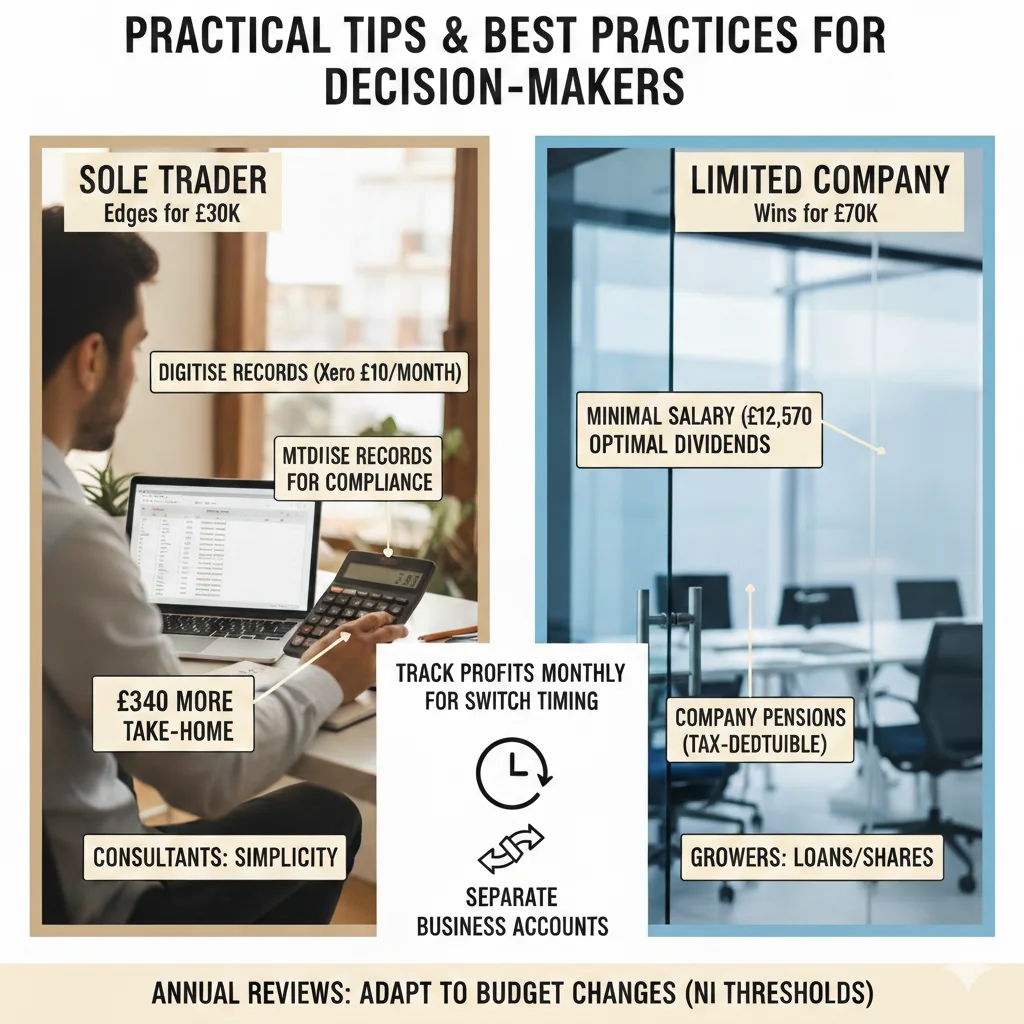

Practical Tips and Best Practices for Decision-Makers

Calculate take-home pay: £30k sole trader edges (£340 more); £70k Ltd wins. Track profits monthly for switch timing. Sole traders: digitise records for MTDITSA (Xero £10/month). Ltd: minimal salary (£12,570 allowance), optimal dividends, company pensions (tax-deductible). Both: separate business accounts. Growers favour Ltd for loans/shares; consultants sole for simplicity. Annual reviews adapt to Budget changes (NI thresholds).

FAQs: Limited Company vs Sole Trader

When should you switch from sole trader to limited company?

Typically at £50–70k profits: Ltd saves via corporation tax/dividends. Notify HMRC; file final Self Assessment.

Do limited companies pay less tax than sole traders?

Yes above £50k—19% CT + lower dividend rates vs 40% income tax/NI. Model your figures.

Is there unlimited liability as sole trader?

Yes—personal assets at risk for debts unlike Ltd’s corporate shield.

What are setup costs?

Sole trader: free. Ltd: £50 Companies House + £100–300 agent/office.

Can sole traders have employees?

Yes, but run PAYE like Ltd; no liability protection.

Limited company scales with protection/tax perks; sole trader starts simple. Align with goals.

If you’re ready to register your company with confidence, Form My Company provides fast, fully online company formation with expert compliance support. Get started today and let our specialists handle the paperwork while you focus on growing your business.