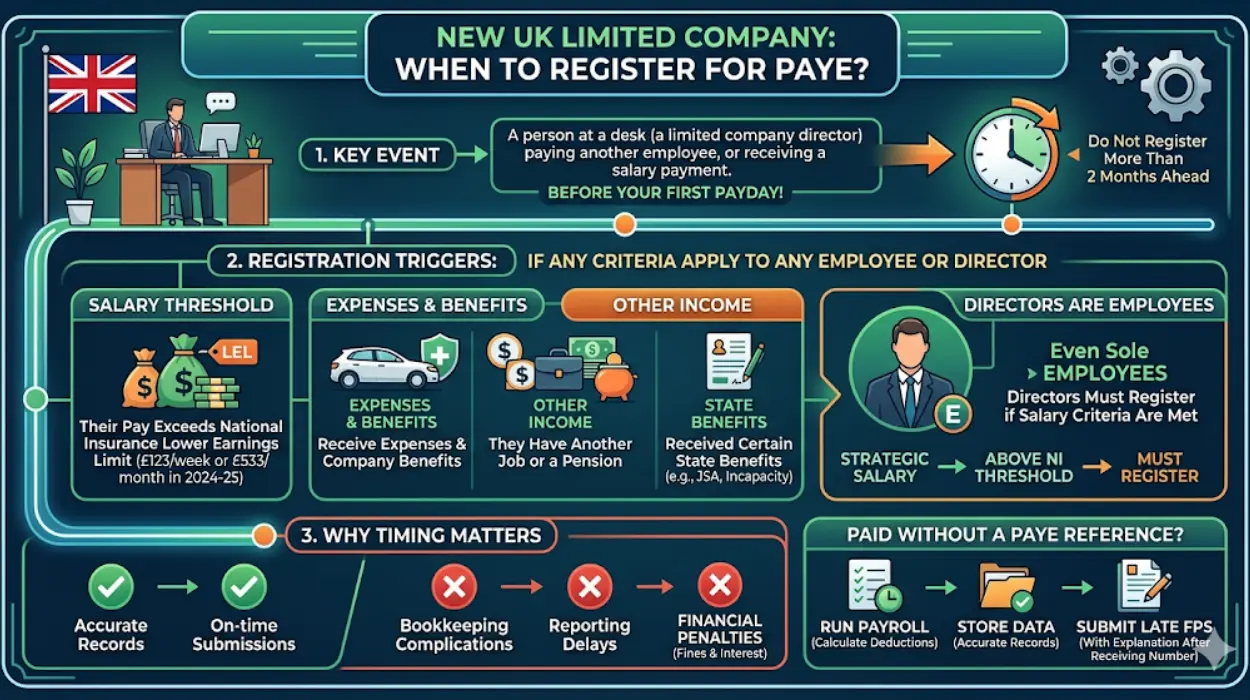

A new UK limited company must register for PAYE with HMRC before the first payday if it employs staff or pays certain expenses like statutory sick pay. This ensures timely compliance with tax obligations from day one of operations involving payroll.

Understanding PAYE Pay As You Earn is essential for any new UK limited company navigating HMRC regulations. PAYE handles the deduction of income tax and National Insurance contributions from employees’ wages, remitting them to HMRC on behalf of the employer. For directors, it applies if they receive remuneration beyond basic allowances. Failing to register promptly can trigger penalties up to £100 per month per employee, underscoring why timing matters for seamless business setup.

What Triggers PAYE Registration for New Companies?

New UK limited companies often assume PAYE only kicks in after hiring full-time staff, but HMRC rules are broader. Registration becomes mandatory as soon as you commit to paying salaries, bonuses, or benefits in kind that qualify as taxable pay. For instance, if your company agrees to a director’s salary during incorporation even before the first payroll run you must notify HMRC within specified deadlines to avoid non-compliance.

Consider a startup launching in Manchester: the founders incorporate as a limited company and decide one director will draw a modest £12,000 annual salary to cover living costs. This triggers PAYE registration before the initial payment date, regardless of company age. HMRC emphasizes that “employment” under PAYE includes directors from their appointment, treating their pay as earnings subject to deductions. Semantic keywords like PAYE setup for limited companies highlight how early action prevents cash flow disruptions from unexpected fines.

Moreover, reimbursing directors for home office expenses or providing company cars can necessitate registration if these count as taxable benefits. HMRC’s guidance clarifies that any “payment of earnings” before the first payday demands proactive steps, aligning with broader payroll compliance for small businesses.

Key Timelines for PAYE Registration

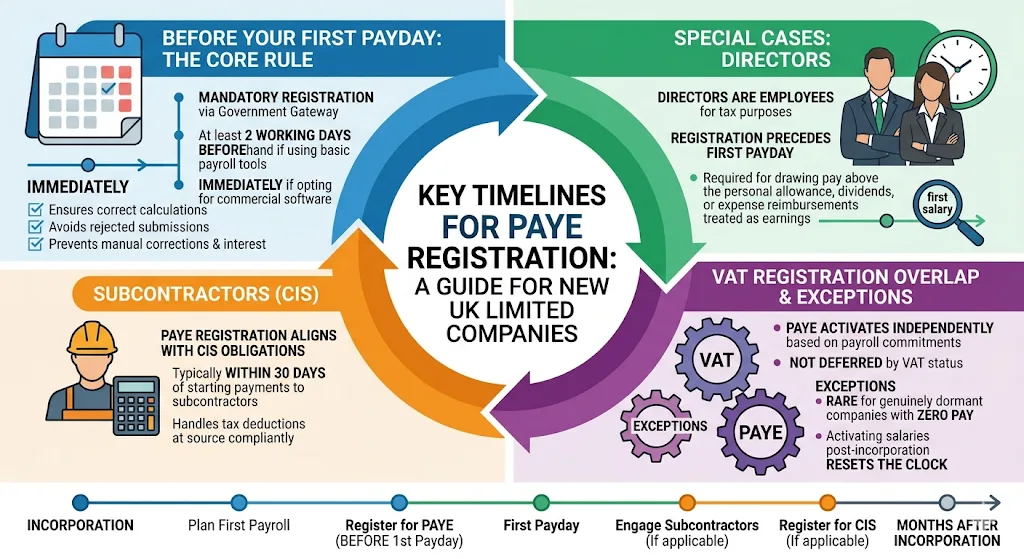

Before Your First Payday: The Core Rule

The primary trigger for new UK limited companies is the approaching first payday. HMRC mandates online registration via their Government Gateway at least two working days beforehand if using their basic payroll tools, or immediately if opting for commercial software. This timeline ensures deductions are correctly calculated from the outset.

In practice, a tech firm in Bristol incorporating on 1 March plans its first salary payments on 28 March. Registration must occur by 26 March to process withholdings accurately. Delaying until after payroll runs risks HMRC rejecting submissions, leading to manual corrections and interest charges. For companies with irregular pay cycles, like weekly payouts to casual workers, the rule applies per cycle—register before the debut payment.

Special Cases: Directors and Subcontractors

Directors of new limited companies face unique scrutiny. Even sole-director setups require PAYE if drawing pay above the personal allowance, often from month one. HMRC views directors as employees for tax purposes, meaning registration precedes any salary, dividend, or expense reimbursement treated as earnings.

Subcontractors paid via CIS (Construction Industry Scheme) add complexity. If your company engages them and must deduct tax at source, PAYE registration aligns with CIS obligations, typically within 30 days of starting payments. A London-based construction limited company hiring its first subcontractor on 15 April must register for PAYE by mid-May to handle 20% deductions compliantly.

VAT Registration Overlap and Exceptions

Companies registering for VAT simultaneously often bundle PAYE, but timelines differ. PAYE isn’t deferred by VAT status; it activates independently based on payroll commitments. Rare exceptions apply to genuinely dormant companies with zero pay, but activating salaries post-incorporation resets the clock.

Common Misconceptions About PAYE for Startups

Many new UK limited company owners believe PAYE registration waits until hiring non-directors or reaching a revenue threshold myths that HMRC debunks routinely. Dividends, for example, fall outside PAYE, handled via self-assessment, but any salary element demands registration. Another pitfall: assuming freelancers sidestep requirements. If workers qualify as employees under IR35 rules common in IT and consulting PAYE applies immediately.

Take a Cambridge software limited company: founders pay themselves dividends initially but later introduce salaries for growth funding. PAYE registration becomes urgent before the first pay run, even post-year one. Missteps here compound with late filing penalties, averaging £400 for small firms per HMRC data. Proactive PAYE registration assistance from specialists streamlines this, integrating with tools like HMRC’s FPS (Full Payment Submission).

Step-by-Step Process for Compliance

New limited companies benefit from a structured approach to PAYE setup. First, gather details: company UTR (Unique Taxpayer Reference), director NI numbers, and payroll software choice. Log into the Government Gateway created during Companies House filing and select “register as an employer.” Provide start dates, employee counts (including directors), and payment frequency.

HMRC issues your employer PAYE reference within 5-10 days, followed by a payment record. Test-run payroll software to simulate deductions, ensuring RTI (Real Time Information) submissions sync seamlessly. For accuracy, verify addresses match Companies House records to prevent rejections.

If complexities arise like multiple directors or international staff professional PAYE registration assistance proves invaluable. Services like those from Form My Company offer outcome-oriented support, handling Gateway setup and initial filings to minimize errors.

Risks of Delaying PAYE Registration

Non-compliance erodes trust and finances. HMRC imposes automatic £100 monthly penalties post-deadline, escalating for persistent delays. Interest accrues on unpaid taxes at 7.75% annually, hitting cash-strapped startups hard. Audits may follow, scrutinizing payroll records back three years.

A hypothetical case: a new Edinburgh retail limited company delays registration amid launch chaos, missing its April payday. By June, penalties exceed £300, plus backdated NI contributions totaling £2,500. Such scenarios underscore why integrating PAYE early aligns with robust business services compliance.

For deeper insights, explore DIY HMRC Registration vs. Using a PAYE Assistance Service to weigh self-setup against expert help.

Integrating PAYE with Broader HMRC Obligations

PAYE dovetails with VAT, Corporation Tax, and CIS for holistic compliance. New limited companies often register all concurrently via one Gateway account, but PAYE’s payroll trigger demands priority. HMRC’s employer helpline confirms sequences, yet high call volumes frustrate founders.

Advanced planning incorporates auto-enrolment pensions, where PAYE data feeds assessment duties. From staging dates based on company size under 50 staff gets two years grace PAYE registration flags pension obligations, avoiding £400 fines per non-compliant worker.

Why Professional Assistance Matters for New Companies

Form My Company’s PAYE Registration Assistance simplifies setup for busy founders. By managing timelines, forms, and RTI integration, they ensure zero-penalty launches. This service targets pain points like director-only payrolls, common in 70% of UK startups per ONS data.

Ready to act? Register for PAYE with HMRC Today – Expert Setup Assistance guides final decisions.

In summary, Form My Company delivers tailored solutions, empowering new UK limited companies to master PAYE registration effortlessly and focus on growth.

What is PAYE registration for a UK company?

PAYE registration with HMRC is required for UK companies paying salaries, bonuses, or taxable benefits to employees or directors, enabling deduction of income tax and National Insurance. New limited companies must register before their first payday to comply with payroll obligations. Form My Company’s PAYE Registration Assistance handles this setup efficiently for seamless HMRC integration.

When does a new UK limited company need to register for PAYE?

A new UK limited company needs PAYE registration before its first payroll run if employing staff or paying director salaries exceeding allowances. Delaying can incur £100 monthly penalties from HMRC. PAYE Registration Assistance from Form My Company ensures timely filing to avoid compliance issues.

How long does PAYE registration take with HMRC?

PAYE registration via HMRC’s Government Gateway typically takes 5-10 working days to receive your employer reference after submission. Companies must apply at least two days before the first payday for basic tools. Form My Company’s PAYE Registration Assistance expedites the process with expert verification.

What documents are needed for PAYE registration?

Key documents for PAYE registration include your company UTR, director NI numbers, payroll start date, and employee details. Accurate Companies House records prevent rejections during Gateway submission. Form My Company’s PAYE Registration Assistance verifies and submits these for error-free approval.

What happens if you don’t register for PAYE on time?

Failing to register for PAYE on time triggers HMRC penalties of £100 per month per affected employee, plus interest on unpaid taxes. Audits may review records back three years, escalating costs for non-compliant companies. Opt for Form My Company’s PAYE Registration Assistance to meet deadlines proactively.