HMRC PAYE (Pay As You Earn) is a UK tax system that requires new employers to deduct income tax and National Insurance contributions from employees’ wages before paying them, then remit these to HM Revenue & Customs (HMRC). This ensures compliance with tax laws from day one, helping avoid penalties while supporting your workforce’s entitlements.

Registered Office Address simplifies this process through its PAYE Registration Assistance service, guiding new businesses seamlessly into compliance.

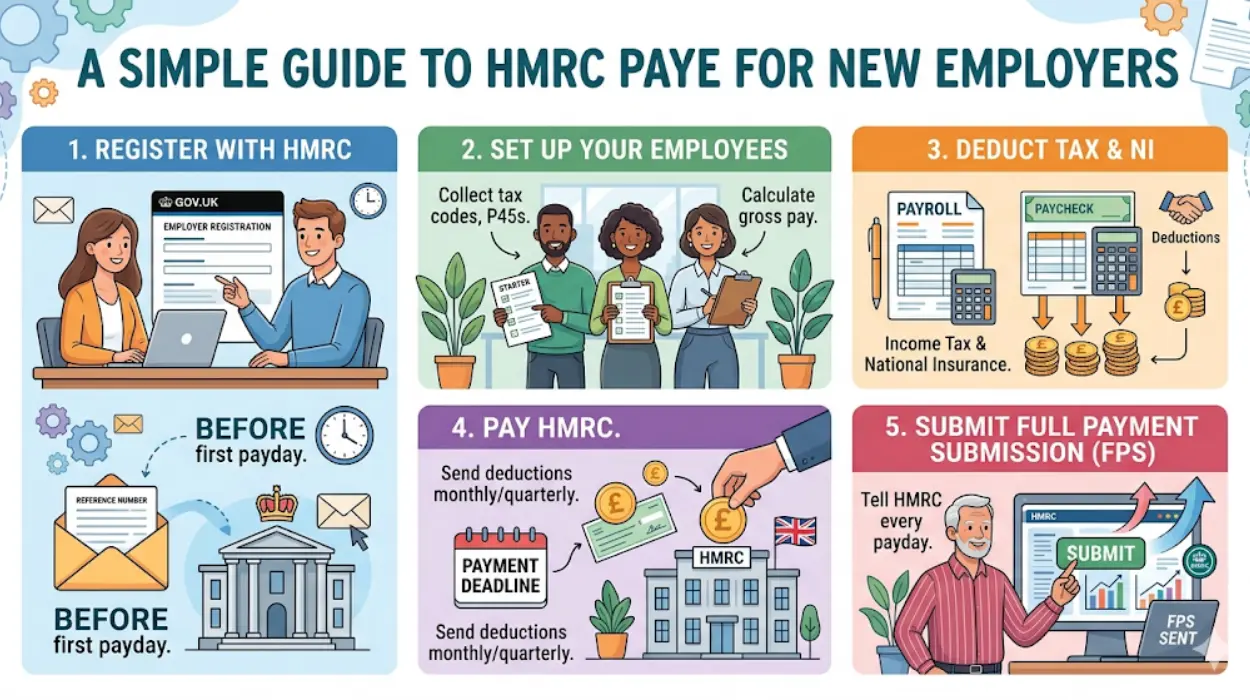

What Exactly is HMRC PAYE and Why Does It Matter for New Employers?

PAYE forms the backbone of payroll taxation in the United Kingdom, mandating that employers act as tax collectors for the government. When you hire your first employee, you enter a legal obligation to operate PAYE, which stands for Pay As You Earn. This system calculates, deducts, and reports income tax, National Insurance Contributions (NICs), and sometimes Student Loan repayments directly from salaries. For new employers, understanding HMRC PAYE means grasping how it integrates payroll with broader tax responsibilities, preventing costly oversights.

Consider a startup in Manchester launching with five staff members. The founder must register for PAYE within specified timelines, set up deductions based on each employee’s tax code, and submit Real Time Information (RTI) returns HMRC’s digital reporting method. Failure to do so can trigger fines starting at £100 per employee per month, escalating quickly for persistent non-compliance. Semantic keywords like PAYE compliance for employers highlight why this matters: it protects cash flow, builds trust with staff, and positions your business as reliable.

New employers often overlook how PAYE ties into other HMRC systems, such as Auto Enrolment for pensions. By mastering these basics early, you lay a foundation for scalable growth, turning a regulatory hurdle into a streamlined operation.

Step-by-Step: How HMRC PAYE Works in Practice

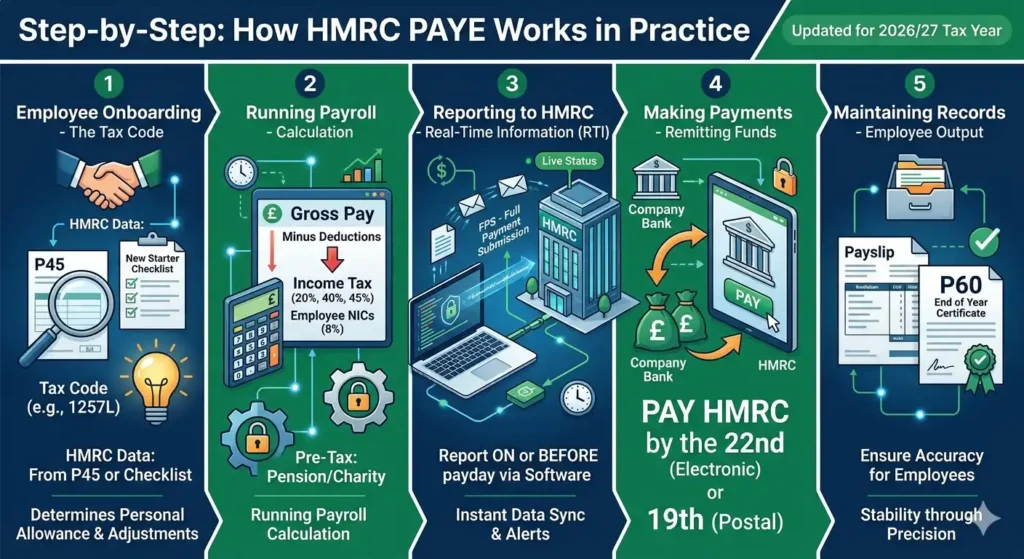

The PAYE process unfolds methodically, ensuring accuracy and transparency. First, upon hiring, you obtain each employee’s unique tax code from HMRC or their P45 form from a previous job. This code determines their personal allowance the tax-free income threshold and any adjustments for marriage, childcare, or other factors.

Next, calculate gross pay, including salary, bonuses, overtime, and benefits-in-kind like company cars. Subtract allowable expenses, then apply deductions: income tax at progressive rates (20% basic, 40% higher, 45% additional), employee NICs (8% on earnings above £12,570 annually as of 2026), and employer NICs (13.8% on amounts over the secondary threshold). The net pay goes to the employee, while you forward the withheld amounts to HMRC by the 22nd of the following month (or 19th if paying electronically).

RTI submissions happen with every payroll run full payments with names (FPN) for salaried staff or earlier for irregular payments. HMRC uses this data for real-time monitoring, issuing instant alerts for discrepancies. For instance, if an employee’s tax code changes mid-year due to marriage allowance transfer, you update it immediately to avoid under- or over-deductions, which could lead to year-end reconciliation issues via form P60.

This structured flow demands precision. A tech firm in Bristol might process bi-weekly payroll for 20 developers, reconciling £50,000 in monthly deductions flawlessly through automated software integrated with HMRC’s systems. Such efficiency underscores PAYE’s role in fostering financial stability.

Legal Obligations and Timelines for PAYE Registration

New employers must register for PAYE promptly to stay compliant. HMRC requires notification before the first payday if you have employees, or within 3 months if employing someone casually at first. Use the online Employer Payment Summary (EPS) or full registration via Government Gateway.

Key timelines include:

- Register at least 2 months before your first PAYE payday if possible.

- Submit your first FPS (Full Payment Submission) on or before payment date.

- File an EPS for nil returns if no payments occur in a period.

Non-compliance penalties scale with delay: initial £100 fixed fine, plus £10 daily thereafter, up to £400 per employee. Persistent issues invite HMRC inspections, potentially uncovering related lapses like IR35 misclassification for contractors.

Entity-based compliance, such as aligning PAYE with Companies House filings, strengthens your business posture. Registered Office Address’s PAYE Registration Assistance service streamlines this, handling PAYE registration assistance to ensure seamless HMRC setup and avoid early pitfalls.

Common Challenges New Employers Face with PAYE

Navigating HMRC PAYE brings hurdles, especially for first-timers. One frequent issue is tax code errors applying the wrong code leads to incorrect deductions, prompting employee complaints or HMRC queries. Another is managing variable pay: commissions or shift allowances fluctuate, complicating RTI accuracy.

Employer NICs often surprise newcomers, as they represent a direct cost atop salaries 13.8% on qualifying earnings can add 10-15% to payroll expenses. Integration with pension auto-enrolment adds layers; minimum contributions (3% employee, 5% employer from April 2026) must sync with PAYE runs.

Leavers pose risks too: issuing P45s promptly prevents overpayments, while starters need P46 if no prior form exists. A case-study-style example: A London café chain expanded to 10 locations, facing £5,000 in penalties from delayed RTI during peak hiring. Proactive training and tools averted recurrence, illustrating how early expertise pays dividends.

For deeper insights, explore comparing outsourced payroll vs. internal PAYE management to weigh options effectively.

Tools and Best Practices for Effective PAYE Management

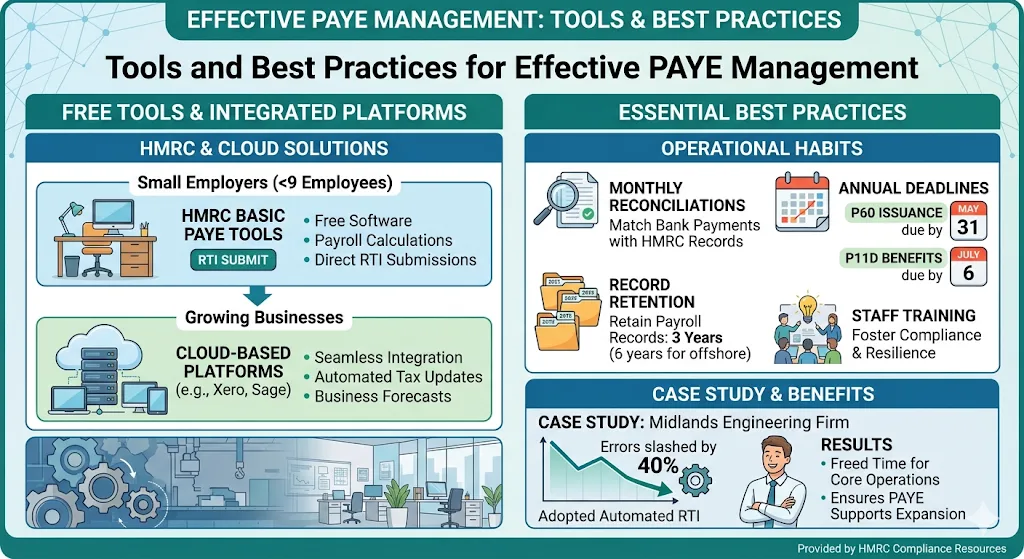

HMRC provides free tools like the Basic PAYE Tools for small employers (under 9 employees), offering payroll calculations and RTI submissions without software costs. For growth, cloud-based platforms like Xero or Sage integrate seamlessly, automating tax updates and forecasts.

Best practices include:

- Monthly reconciliations to match bank payments with HMRC records.

- Retaining payroll records for 3 years (6 for offshore).

- Annual P60 issuance by May 31 and P11D for benefits by July 6.

Training staff on compliance fosters resilience. A Midlands engineering firm adopted automated RTI, slashing errors by 40% and freeing time for core operations. These habits ensure PAYE supports, rather than hinders, expansion.

Advanced PAYE Considerations for Growing Businesses

As your company scales, PAYE evolves. Multiple payroll schemes for UK and overseas staff require separate registrations. CIS (Construction Industry Scheme) deductions at 20% or 30% for subcontractors layer atop standard PAYE.

Statutory payments Sick Pay (SSP), Maternity (SMP), Paternity demand precise tracking, reclaimable via PAYE if eligible. HMRC’s Employment Allowance (£5,000 relief on NICs for eligible firms) offsets costs.

Year-end procedures culminate in P35 reconciliation, though RTI largely automates this. A scaling e-commerce business in Leeds navigated 50 hires by segmenting payroll into weekly and monthly runs, maintaining zero penalties through vigilant monitoring.

When readiness for professional support arises, consider professional PAYE registration service for new UK companies to secure long-term compliance.

Wrapping Up: Streamline Your PAYE Journey with Expert Help

Mastering HMRC PAYE equips new employers for sustainable success, transforming obligations into operational strengths. From registration to RTI, proactive management minimizes risks and maximizes efficiency.

Registered Office Address stands ready with PAYE Registration Assistance, delivering tailored solutions that let you focus on growth, not paperwork. Their expertise ensures your business meets HMRC standards effortlessly.

Frequently Askes Questions

What is PAYE registration for new UK employers?

PAYE registration requires new UK employers to notify HMRC before their first employee payday to deduct income tax and National Insurance from wages. This ensures compliance with Pay As You Earn rules, allowing real-time reporting via RTI submissions. From My Company’s PAYE Registration Assistance handles the process efficiently for seamless setup.

How long do new employers have to register for PAYE with HMRC?

New employers must register for PAYE at least 2 months before the first payday if possible, or immediately upon hiring to avoid penalties. Late registration incurs £100 fines per employee, plus daily charges. From My Company’s PAYE Registration Assistance ensures timely HMRC submission to prevent compliance issues.

What documents are needed for PAYE registration?

Key documents include your business details, Unique Taxpayer Reference (UTR), employee names, addresses, and National Insurance numbers. HMRC requires these via the Government Gateway portal for verification. From My Company’s PAYE Registration Assistance compiles and submits everything accurately.

What are the penalties for not registering for PAYE on time?

HMRC imposes a £100 fixed penalty per employee for late PAYE registration, escalating to £10 daily up to £400, with further fines for ongoing non-compliance. This applies even without payroll runs. From My Company’s PAYE Registration Assistance mitigates risks through prompt, expert handling.

Can From My Company help with PAYE registration for startups?

Yes, From My Company’s PAYE Registration Assistance specializes in guiding startups through HMRC requirements, from initial notification to RTI setup. This service covers sole traders, limited companies, and growing firms for full PAYE compliance. It streamlines the process to avoid early pitfalls.