VAT registration directly affects pricing by requiring businesses to add VAT to taxable sales, which can increase customer-facing prices or reduce margins if absorbed. It also enables VAT recovery on expenses, improving net profitability when managed strategically.

How does VAT registration change your pricing structure?

VAT registration alters pricing by adding a standard 20% VAT to most goods and services in the UK, requiring businesses to either increase prices or absorb the tax within existing margins, directly influencing competitiveness and perceived value.

VAT creates a visible price difference between registered and non-registered businesses. When a business crosses the VAT threshold of £90,000 (as of 2024), it must apply VAT to taxable sales. This forces a pricing decision.

Businesses typically adopt one of two pricing approaches:

- Increase prices by 20% to pass VAT to customers

- Maintain prices and absorb VAT, reducing profit per sale

Each approach produces different outcomes. Passing VAT increases the total cost to consumers. Absorbing VAT protects price competitiveness but compresses margins.

Pricing strategy depends on customer type. B2B clients reclaim VAT, so price increases rarely affect demand. B2C customers cannot reclaim VAT, so price sensitivity increases immediately.

How does VAT registration affect profit margins?

VAT registration impacts profit margins by reducing net revenue when VAT is absorbed, but it can improve margins through input VAT recovery on business expenses, creating a balance between tax liability and reclaim opportunities.

Profit margins shift based on how VAT is handled in pricing. When VAT is added on top of prices, margins remain stable, but demand may drop. When VAT is included within existing prices, margins decline instantly.

For example, a £100 service becomes £83.33 net revenue after VAT. This results in a 16.67% reduction in gross income per transaction.

However, VAT registration introduces a key financial advantage: input VAT recovery. Businesses reclaim VAT paid on:

- Office rent and utilities

- Software subscriptions and tools

- Professional services such as legal or accounting

If a company incurs £10,000 in VAT-paid expenses annually, reclaiming this amount offsets output VAT liability and improves net profitability.

The net margin effect depends on the expense structure. Businesses with high VATable costs benefit more than low-expense service providers.

When should a business adjust pricing after VAT registration?

A business must adjust pricing immediately after VAT registration becomes effective, ensuring compliance with HMRC rules while maintaining margin control and market positioning based on customer type and competitive benchmarks.

VAT becomes chargeable from the effective date of registration. This requires immediate pricing updates across all systems, including invoices, websites, and contracts.

Delaying pricing updates creates compliance risks and accounting discrepancies. HMRC requires accurate VAT reporting from the first taxable transaction after registration.

Pricing adjustments depend on three conditions:

- Customer base composition (B2B vs B2C)

- Competitive landscape within the industry

- Cost structure and margin flexibility

For example, a consultancy serving VAT-registered businesses can increase prices without losing demand. A retail business selling to consumers faces immediate price resistance and may need gradual adjustments.

Transparent communication also matters. Businesses that clearly explain VAT inclusion maintain customer trust and reduce confusion at checkout.

How does VAT registration influence competitive positioning?

VAT registration influences competitive positioning by increasing visible prices compared to non-registered competitors, but it also enhances credibility, enabling businesses to compete for larger contracts and partnerships that require VAT compliance.

Unregistered businesses can offer lower prices because they do not charge VAT. This creates a short-term pricing advantage in consumer markets.

However, VAT registration signals legitimacy. Larger organisations prefer working with VAT-registered suppliers due to compliance and audit requirements. This opens access to higher-value contracts.

Competitive positioning shifts in two ways:

- Price-sensitive markets favour non-registered businesses

- Corporate and B2B markets favour VAT-registered entities

Businesses often reposition their offerings after registration. Instead of competing on price, they emphasise value, service quality, or expertise.

VAT registration also aligns businesses with formal financial systems, improving access to funding, partnerships, and international trade opportunities.

What pricing strategies work best after VAT registration?

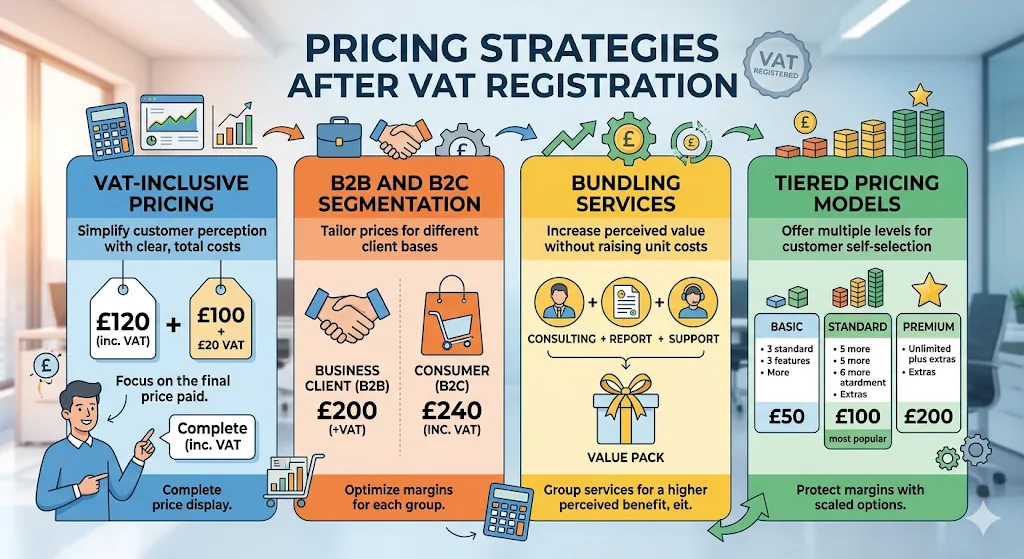

Effective pricing strategies after VAT registration include value-based pricing, VAT-inclusive pricing for transparency, and tiered pricing models that protect margins while maintaining customer appeal across different segments.

Businesses adapt pricing models to reduce the perceived impact of VAT.

Common strategies include:

- Implement VAT-inclusive pricing to simplify customer perception

- Segment pricing for B2B and B2C customers

- Bundle services to increase perceived value without raising unit prices

Value-based pricing becomes critical. Instead of focusing on cost-plus pricing, businesses align pricing with outcomes delivered.

For example, a digital agency charging £1,200 instead of £1,000 shifts focus from price to results. VAT becomes less noticeable when the value proposition is strong.

Tiered pricing also helps maintain margins. Offering three pricing levels—basic, standard, premium—allows customers to self-select based on budget and perceived value.

How does VAT recovery improve financial efficiency?

VAT recovery improves financial efficiency by allowing businesses to reclaim input VAT on operational costs, reducing overall tax burden and increasing effective cash flow when expenses are consistently VAT-inclusive.

Input VAT recovery acts as a cost-reduction mechanism. Every eligible expense reduces the total VAT payable to HMRC.

Businesses optimise recovery by:

- Tracking VAT on all eligible purchases

- Using compliant invoicing systems

- Maintaining accurate financial records

For example, if a company collects £20,000 in VAT from customers and pays £8,000 in VAT on expenses, the net VAT payable is £12,000. This reduces the effective tax burden.

Efficient VAT management improves cash flow predictability. Businesses that integrate VAT tracking into accounting systems avoid underpayment or overpayment issues.

Using professional support, such as VAT Registration Assistance, ensures the correct classification of expenses and maximises reclaim opportunities. Learn more about VAT Registration Assistance.

What mistakes reduce profit margins after VAT registration?

Common mistakes include absorbing VAT without adjusting pricing, failing to reclaim input VAT, misclassifying taxable items, and poor financial tracking, all of which reduce margins and create compliance risks.

Margin erosion often results from avoidable errors.

Key mistakes include:

- Absorb VAT without recalculating margins

- Ignore reclaimable VAT on business expenses

- Misclassify zero-rated or exempt supplies

- Delay VAT filings, leading to penalties

Each mistake has a measurable financial impact. For example, failing to reclaim £5,000 in input VAT directly reduces annual profit by the same amount.

Accurate classification also matters. Some goods and services qualify for reduced or zero VAT rates. Misclassification leads to overpayment or compliance issues.

Businesses that implement structured VAT processes maintain stable margins and avoid unnecessary financial leakage.

Also explore,

The Essential Checklist for UK Businesses Approaching the Compulsory VAT Limit

Why Staying Under the VAT Threshold Might Be Limiting Your Business Growth

How does VAT registration affect long-term growth strategy?

VAT registration supports long-term growth by enabling scalable pricing models, improving financial transparency, and aligning businesses with regulatory frameworks required for expansion into larger markets and international trade.

VAT registration acts as a growth milestone. It signals that a business has reached a scale requiring formal tax compliance.

Growth benefits include:

- Access to larger clients requiring VAT invoices

- Improved financial reporting for investors and lenders

- Alignment with international trade requirements

VAT also standardises pricing across markets. Businesses entering the EU or global markets operate within established VAT frameworks, reducing friction.

Companies planning cross-border operations benefit from expert guidance. This is explained in detail in Why expert VAT advice is crucial for businesses with international trading links.

VAT registration also prepares businesses for advanced tax structures such as VAT schemes, including the Flat Rate Scheme or Margin Scheme, which further optimise profitability.

How can expert VAT support improve pricing and margins?

Expert VAT support improves pricing and margins by ensuring accurate registration, optimal pricing strategies, full VAT recovery, and compliance with HMRC rules, reducing financial risk while enhancing operational efficiency.

Professional VAT services provide structured support across the entire lifecycle of VAT management.

Key benefits include:

- Accurate VAT registration aligned with business model

- Strategic pricing recommendations based on market positioning

- Identification of reclaim opportunities across all expenses

- Ongoing compliance and reporting support

From My Company delivers specialised VAT Registration Assistance designed to help businesses implement efficient pricing structures and maximise profitability from day one.

Expert guidance reduces costly errors and ensures businesses operate within HMRC regulations while maintaining competitive pricing.

Businesses ready to optimise their VAT strategy can explore expert-led solutions here: Book your consultation for fast VAT registration assistance with our expert team.

VAT registration directly reshapes pricing and profit margins by introducing tax obligations and recovery opportunities. Businesses that adjust pricing strategically, track VAT accurately, and optimise recovery maintain strong margins and competitive positioning.

From My Company provides structured VAT Registration Assistance that supports accurate implementation, efficient pricing strategies, and long-term financial performance.

Frequently Asked Questions

What is VAT registration, and when is it required in the UK?

VAT registration is the process of enrolling a business with HMRC to charge VAT on taxable goods or services. It becomes mandatory when taxable turnover exceeds £90,000 in 12 months. From My Company provides VAT Registration Assistance to ensure accurate and timely compliance.

How long does VAT registration take in the UK?

VAT registration typically takes 10 to 30 working days, depending on HMRC processing times and application accuracy. Delays often occur due to incomplete information or verification checks. Using VAT Registration Assistance from From My Company helps streamline the process and reduce errors.

Can I register for VAT voluntarily before reaching the threshold?

Yes, businesses can voluntarily register for VAT even if turnover is below £90,000. This allows input VAT recovery on expenses and improves business credibility with VAT-registered clients. From My Company supports voluntary registration through its VAT Registration Assistance service.

What documents are required for VAT registration?

HMRC requires business details such as company registration number, turnover records, bank details, and a description of activities. Additional verification may include identity checks and proof of trading. VAT Registration Assistance from From My Company ensures all required documents are correctly prepared and submitted.

How does VAT registration affect pricing for customers?

VAT registration requires businesses to add VAT, usually 20%, to taxable sales, which increases final prices for non-VAT-registered customers. Businesses must decide whether to pass on the cost or absorb it within margins. From My Company helps structure pricing strategies through VAT Registration Assistance.