The UK VAT registration threshold is £90,000 in taxable turnover, measured over any rolling 12‑month period, not the tax year. Once cumulative revenue exceeds this limit, businesses must notify HMRC within 30 days and register for VAT.

HMRC evaluates taxable turnover continuously. Each month, businesses add the latest month’s taxable sales and drop the same month from the previous year. This rolling calculation prevents timing manipulation and ensures timely compliance.

Taxable turnover includes standard-rated, reduced-rated, and zero-rated supplies. It excludes exempt supplies such as certain financial services. Accurate categorisation matters because misclassification leads to incorrect threshold tracking.

Businesses must also monitor expected turnover. If projected taxable sales exceed £90,000 in the next 30 days alone, registration is required immediately. This “forward look” rule captures sudden growth events such as large contracts or seasonal spikes.

What records must be maintained before reaching the VAT threshold?

Maintain complete sales and purchase records, VAT classifications, invoices, receipts, and digital accounting logs. Businesses must evidence taxable turnover calculations, verify supply types, and retain documentation for at least six years to support HMRC reviews and accurate VAT registration.

Robust records start with invoice discipline. Each sale must show date, value, VAT rate, and customer details. Consistent invoice numbering enables traceability during audits.

Purchase records must separate recoverable and non-recoverable VAT. This distinction becomes critical once registered because input tax recovery depends on valid VAT invoices and correct categorisation.

Digital record-keeping aligns with Making Tax Digital (MTD) requirements. Systems must store and transmit data via compatible software. Manual spreadsheets without digital links increase compliance risk.

Retention periods matter. HMRC requires records for six years, including credit notes, import documents, and evidence of zero-rating. Clear audit trails reduce disputes and speed up registration checks.

When must a business register for VAT with HMRC?

Register within 30 days after the end of the month in which taxable turnover exceeds £90,000, or immediately when expected turnover exceeds the threshold in the next 30 days. The effective registration date determines when VAT must be charged and reported.

The notification deadline is strict. Missing the 30-day window triggers penalties and potential interest on underpaid VAT. The effective date is usually the first day of the second month after exceeding the threshold.

Forward-looking registration has a different effective date. When a contract guarantees that the next 30 days will exceed £90,000, the effective date is the date you realised this expectation.

Early voluntary registration remains an option. Businesses with significant input VAT, such as equipment purchases, often register before hitting the threshold to reclaim costs and signal credibility to B2B clients.

How does approaching the threshold affect pricing and cash flow?

Crossing the threshold requires adding VAT (typically 20%) to prices or absorbing it within margins. This shifts customer demand, impacts competitiveness, and changes cash flow because VAT collected must be remitted to HMRC on scheduled returns.

Pricing decisions depend on the customer base. B2B clients often recover VAT, so price sensitivity is lower. B2C customers cannot reclaim VAT, which makes gross price increases more visible and potentially reduces demand.

Margin management becomes central. Businesses choose between passing on the full 20% VAT, partially absorbing it, or restructuring offerings. Each choice affects profitability and positioning.

Cash flow timing changes with VAT returns. Output VAT collected from customers is not income; it is a liability. Input VAT on purchases offsets this liability, but timing differences can create short-term cash pressure.

Scheme selection can stabilise cash flow. The Flat Rate Scheme, Cash Accounting Scheme, and Annual Accounting Scheme each alter payment timing and calculations. Selection must align with transaction patterns and sector rates.

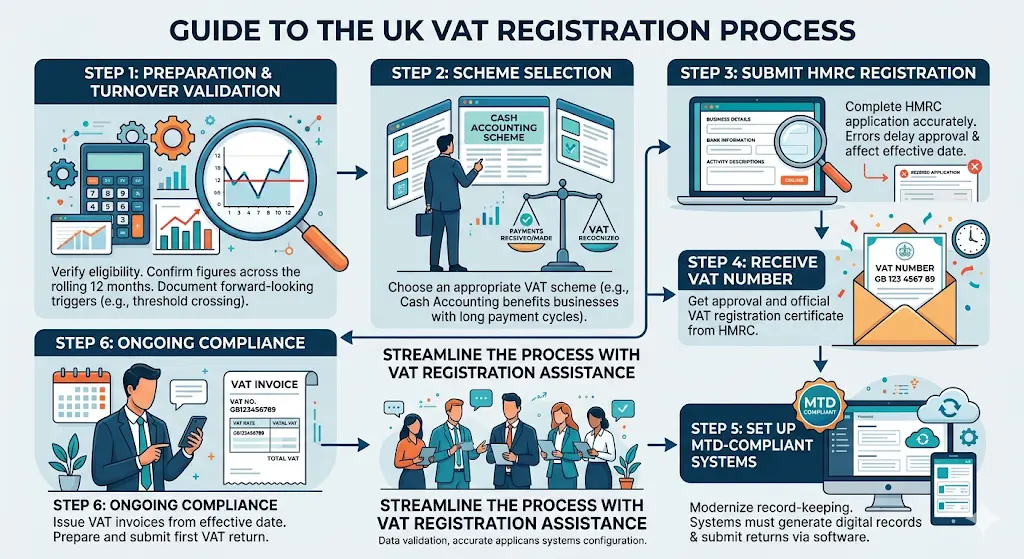

What steps are involved in the VAT registration process?

The process includes verifying eligibility, calculating taxable turnover, choosing a VAT scheme, submitting HMRC registration, receiving a VAT number, setting up MTD-compliant systems, and issuing VAT invoices from the effective date while preparing the first return.

Preparation starts with accurate turnover validation. Businesses must confirm figures across the rolling 12 months and document any forward-looking triggers.

Scheme selection affects ongoing obligations. For example, the Cash Accounting Scheme recognises VAT when payments are received or made, which benefits businesses with long payment cycles.

The HMRC application requires business details, bank information, and activity descriptions. Errors delay approval and can misalign the effective date.

After approval, businesses must update invoices to include the VAT number, rate, and amounts. Systems must generate digital records and submit returns through MTD-compatible software.

To streamline these steps, many firms use VAT Registration Assistance services that validate data, submit accurate applications, and configure compliant systems from day one. Explore outcome-focused support through this VAT Registration Assistance page.

How can businesses prepare operationally before hitting the threshold?

Prepare by updating accounting systems, training staff on VAT rules, revising contracts and pricing, segmenting customers by VAT sensitivity, and establishing controls for invoicing and reporting to ensure compliance from the first VAT-effective transaction.

System readiness prevents errors on day one. Accounting platforms must apply correct VAT rates, generate compliant invoices, and maintain digital links for MTD submissions.

Staff training reduces misclassification. Teams must distinguish between standard-rated, reduced-rated, zero-rated, and exempt supplies. Clear internal guides and approval workflows limit mistakes.

Contract terms often require updates. Pricing clauses, payment terms, and VAT treatment must be explicit. This avoids disputes when VAT is introduced to existing agreements.

Customer segmentation informs pricing strategy. Businesses serving 70% B2B clients may pass on VAT with minimal impact, while B2C-heavy firms may redesign bundles or introduce tiered pricing to protect demand.

What penalties apply if you fail to register on time?

Late registration triggers penalties based on VAT owed and delay length, plus interest on unpaid amounts. HMRC can backdate the effective registration date, requiring businesses to account for VAT on past sales without having charged customers.

Penalty calculations consider behaviour and duration. Careless errors incur lower rates than deliberate non-compliance, but both increase with longer delays.

Backdating creates immediate liabilities. If HMRC sets an earlier effective date, businesses owe output VAT for that period. Recovering VAT from customers after the fact is often impractical.

Interest accrues on unpaid VAT. This adds to the financial burden and can strain cash flow, especially for businesses with thin margins or slow receivables.

Proactive monitoring and timely registration eliminate these risks. Consistent monthly checks of rolling turnover provide early warning signals.

How can VAT schemes influence compliance and cost management?

Choosing the right scheme—Flat Rate, Cash Accounting, or Annual Accounting—changes how VAT is calculated and paid, affecting administrative effort, cash flow timing, and effective tax cost depending on sector percentages and transaction patterns.

The Flat Rate Scheme applies a fixed percentage to gross turnover. It simplifies calculations but limits input VAT recovery, which may increase the effective cost for purchase-heavy businesses.

Cash Accounting aligns VAT payments with actual cash movement. This reduces pressure when customers pay late and is beneficial for businesses with extended credit terms.

Annual Accounting reduces filing frequency to one return per year with advance payments. It smooths administration but requires disciplined budgeting to meet scheduled payments.

Selecting a scheme requires data analysis. Businesses must compare input VAT levels, payment cycles, and sector rates to determine the most efficient option.

Also explore,

Why Staying Under the VAT Threshold Might Be Limiting Your Business Growth

Understanding Different VAT Schemes Available for Small Businesses and Sole Traders

How can VAT Registration Assistance reduce errors and speed compliance?

VAT Registration Assistance validates turnover calculations, selects appropriate schemes, prepares HMRC submissions, configures MTD systems, and establishes compliant invoicing processes, reducing delays, preventing penalties, and ensuring accurate VAT treatment from the effective date.

Professional assistance standardises data validation. Experts reconcile sales records, verify VAT classifications, and document threshold calculations to support HMRC scrutiny.

Application accuracy improves approval timelines. Correct business activity codes, bank details, and scheme choices reduce back-and-forth with HMRC.

System configuration ensures compliance. MTD-compatible software, digital links, and invoice templates are set up correctly, which prevents reporting errors in the first return.

Businesses also gain guidance on reclaiming pre-registration VAT where eligible. For a deeper explanation, see How VAT registration assistance helps reclaim pre-registration costs.

When ready to proceed, decision-focused guidance on Purchase VAT registration support for accurate filings and expert tax advice is available here.

From My Company delivers structured onboarding, verified submissions, and compliant system setup, ensuring a clean start under VAT.

Approaching the £90,000 VAT threshold requires precise turnover tracking, disciplined record-keeping, and timely HMRC registration. Clear pricing strategy, scheme selection, and MTD-ready systems prevent disruption. From My Company supports accurate registration and compliant operations through VAT Registration Assistance, reducing risk and ensuring correct filings from day one.

Frequently Asked Questions

What is VAT Registration Assistance and who needs it?

VAT Registration Assistance supports UK businesses in registering for VAT with HMRC by validating turnover, preparing applications, and ensuring compliance. From My company provides VAT Registration Assistance for businesses approaching or exceeding the £90,000 threshold or planning voluntary registration.

How long does the VAT registration process take in the UK?

HMRC typically processes VAT registrations within 10 to 30 working days, depending on application accuracy and verification checks. VAT Registration Assistance from From My company helps reduce delays by submitting complete and validated information.

Can I register for VAT before reaching the £90,000 threshold?

Yes, businesses can voluntarily register for VAT before hitting the compulsory threshold to reclaim input VAT and enhance credibility. From My company offers VAT Registration Assistance to assess eligibility and manage early registration correctly.

What documents are required for VAT registration?

Required documents include business details, turnover records, bank information, and a description of activities. VAT Registration Assistance ensures these documents are accurate and aligned with HMRC requirements for smooth approval.

What happens if I register late for VAT?

Late VAT registration can result in penalties, interest, and backdated VAT liabilities based on when the threshold was exceeded. VAT Registration Assistance from From My company helps identify deadlines and submit timely applications to avoid compliance risks.