Filing your confirmation statement too early can create data inaccuracies, trigger compliance mismatches, and require duplicate filings within the same review period. It can also distort your company’s official records, leading to inconsistencies with Companies House expectations and potential administrative complications.

Why does filing a confirmation statement too early cause compliance issues?

Filing too early captures outdated company data, which fails to reflect changes occurring later in the review period. This creates a mismatch between actual company status and officially registered records, increasing the likelihood of corrections, refiling, and compliance inconsistencies.

A confirmation statement verifies company information at a specific point in time. This includes registered office address, director details, People with Significant Control (PSC), and share structure. When the filing occurs early, it locks in a snapshot that may become inaccurate within days or weeks.

Companies House operates on a 12-month review cycle. Filing prematurely does not extend the next due date. It only confirms data at that moment. If changes occur after submission, they remain unreported until the next cycle unless separately updated through other filings.

This disconnect creates administrative friction. For example, if a director resigns 10 days after early filing, the confirmation statement still reflects outdated governance. This misalignment complicates record validation during audits or due diligence checks.

What specific data risks arise from early filing?

Early filing increases the risk of recording incomplete or outdated data across key company registers. This includes director appointments, PSC updates, and share allocations, which may change before the review period ends but remain unreported in the submitted confirmation statement.

The confirmation statement consolidates multiple data points into one filing. These include:

- Director and secretary records

- PSC register details

- Share capital and shareholder structure

Each of these elements can change frequently. For example, startups often issue new shares within short timeframes. Filing early before completing such actions results in a statement that fails to reflect ownership accurately.

PSC changes present another risk. If control thresholds shift due to share transfers, the early filing omits this critical update. This creates discrepancies between internal registers and Companies House records.

Accurate reporting relies on timing. Filing after all planned changes ensures that the statement reflects a complete and verified dataset.

How does early filing affect your next confirmation statement deadline?

Filing early does not reset or extend your confirmation statement deadline. The next due date remains tied to your original review period, meaning early submission can compress your compliance timeline and increase administrative workload within the same annual cycle.

The confirmation statement follows a fixed annual cycle based on the company’s incorporation date or last filing date. Filing early within this cycle does not alter the next review period end date.

For example, if a company’s review period ends on 30 September and the statement is filed on 1 July, the next deadline still falls on 30 September the following year. This effectively shortens the operational window between filings.

This compressed timeline creates pressure on compliance processes. Companies must track changes more frequently and ensure readiness for the next filing sooner than expected.

Consistent scheduling aligned with the end of the review period avoids this issue and maintains predictable compliance intervals.

Can early filing lead to duplicate submissions?

Yes, early filing can result in duplicate submissions if company details change later in the same review period. Businesses must then file additional updates or corrections, increasing administrative effort and creating multiple overlapping records within a single reporting cycle.

Duplicate filings occur when changes arise after the confirmation statement has already been submitted. These changes cannot be retroactively included in the original filing.

Instead, companies must update records through separate forms or wait until the next confirmation statement. In some cases, businesses choose to refile to maintain consistency across records.

This creates inefficiencies:

- Increased administrative workload due to repeated filings

- Higher risk of inconsistencies across multiple submissions

- Additional time spent reconciling company records

Maintaining a single, accurate submission per cycle improves clarity and reduces compliance overhead.

How does early filing impact data accuracy during audits or due diligence?

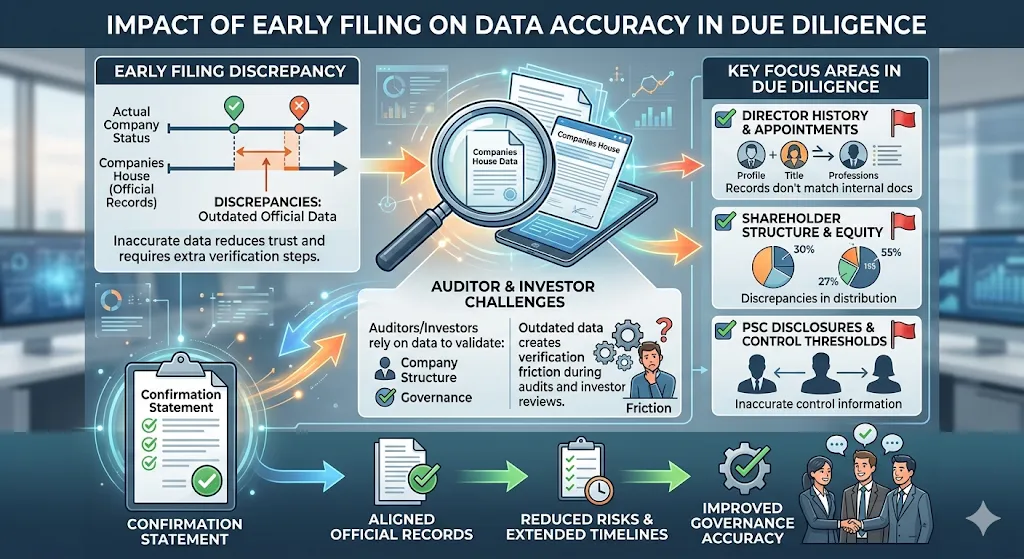

Early filing introduces discrepancies between official records and actual company status, which can complicate audits, investor reviews, and due diligence processes. Inaccurate data reduces trust in company records and may require additional verification steps.

Auditors and investors rely on Companies House data to validate company structure and governance. When this data is outdated due to early filing, it creates friction in verification.

For example, during investment due diligence, stakeholders examine:

- Director of history and appointments

- Shareholder structure and equity distribution

- PSC disclosures and control thresholds

If these records do not match internal documents, it raises concerns about governance accuracy. This often leads to additional documentation requests and extended review timelines.

Accurate confirmation statements reduce these risks by aligning official records with the actual company status at the end of the review period.

What is the correct timing strategy for filing a confirmation statement?

The optimal timing is near the end of the review period, after all significant changes have been recorded. This ensures that the confirmation statement reflects complete, verified, and up-to-date company information aligned with Companies House requirements.

A structured timing approach improves accuracy and compliance. The process involves:

- Review company records 14 days before the review period ends

- Verify all changes in directors, PSCs, and shareholding

- Update internal registers before submission

- Submit the confirmation statement within the allowed filing window

This approach captures a complete snapshot of company data. It reduces the likelihood of omissions and eliminates the need for corrective filings.

Using a professional service to file a confirmation statement accurately and on time ensures that all compliance checks are completed systematically and without oversight.

How does early filing affect companies with frequent structural changes?

Companies with frequent updates, such as startups or investment-backed firms, face higher risks when filing early because their ownership, control, and governance structures evolve rapidly within short timeframes.

High-growth companies often execute multiple structural changes within a single review period. These include:

- Issuing new shares to investors

- Appointing or removing directors

- Adjusting PSC thresholds

Filing early in such environments guarantees that at least one of these elements becomes outdated before the period ends.

For example, a company raising funding in stages may issue shares in three rounds over six months. Filing after the first round omits subsequent changes, creating incomplete ownership records.

Delaying filing until all planned changes are executed ensures that the confirmation statement reflects the full corporate structure.

To understand the broader compliance requirement, review why even inactive entities must stay updated through this guide on why dormant UK companies must still meet confirmation obligations.

When does early filing make sense, if ever?

Early filing only makes sense when no further changes are expected within the review period and all company data has been fully verified. This scenario is rare, as most companies experience at least minor updates throughout the year.

Stable companies with minimal activity may consider early filing. These typically include:

- Single-director businesses with no share changes

- Dormant companies with no operational activity

- Firms with fixed ownership and governance structures

Even in these cases, risk remains. Unexpected changes, such as director resignations or address updates, can still occur after filing.

A safer approach involves waiting until the review period nears completion. This allows time to confirm that no further updates are pending.

Accuracy takes priority over speed in regulatory filings.

How can businesses avoid the risks of early filing?

Businesses avoid early filing risks by aligning submission timing with the end of the review period, maintaining accurate internal records, and using structured compliance processes to verify all company data before submission.

Effective compliance management includes three core practices:

- Maintain real-time updates in statutory registers

- Schedule periodic compliance reviews throughout the year

- Validate all company data before filing

This structured approach ensures that the confirmation statement reflects a complete and accurate dataset.

Professional support adds a layer of verification. Services that specialise in Companies House compliance review data against official frameworks and submission standards.

For businesses seeking precision and efficiency, working with experts who handle accurate Companies House filing and compliance management ensures consistency across all filings.

From My Company provides structured compliance support that aligns filing timing with regulatory expectations while ensuring data accuracy across all submitted records.

Filing a confirmation statement too early creates avoidable risks. These include inaccurate records, duplicate filings, and compliance inconsistencies. The issue stems from timing, not complexity.

Submitting near the end of the review period ensures that all company data is complete and verified. This approach improves accuracy, reduces administrative workload, and aligns with Companies House expectations.

From My Company supports businesses by managing confirmation statement timing, verifying company data, and ensuring that each submission reflects a precise and compliant snapshot of company records.

Frequently Asked Questions

What is a confirmation statement, and why is it required in the UK?

A confirmation statement is a mandatory Companies House filing that verifies a company’s registered details, including directors, shareholders, and PSCs. To file a confirmation statement ensures that official records remain accurate and compliant with UK company law.

When should you file a confirmation statement for your company?

You must file a confirmation statement at least once every 12 months, typically near the end of your review period. Filing at the correct time ensures that all company information is complete and aligned with Companies House records.

What happens if you file a confirmation statement late or incorrectly?

Late or incorrect filing can lead to penalties, compliance warnings, or even company strike-off proceedings. Using a structured approach to file a confirmation statement helps maintain accurate records and avoids regulatory issues.

Can you update the company details when you file a confirmation statement?

Yes, you can update or confirm key company details such as registered office address, directors, and share capital during the process. Filing a confirmation statement acts as a formal validation of your company’s current structure and records.

Do dormant companies need to file a confirmation statement?

Yes, dormant companies must still file a confirmation statement annually to confirm that their details remain unchanged. From My company ensures that even inactive businesses stay compliant with Companies House filing requirements.