A significant accounting transaction for a dormant company is any financial activity that affects its accounting records, excluding specific permitted statutory fees. These include trading income, expenses, asset purchases, or liabilities, which legally disqualify dormant status under UK accounting and Companies House rules.

What qualifies as a significant accounting transaction under UK law?

A significant accounting transaction includes any entry in accounting records involving money movement, liabilities, or asset changes, except for allowed statutory payments such as Companies House filing fees, late penalties, or shares issued during incorporation.

UK law defines dormancy under the Companies Act 2006. A company is dormant when it has no significant accounting transactions during a financial year. This definition applies strictly to entries recorded in accounting systems, not just bank activity.

Three permitted exceptions exist that do not break dormancy status:

- Payment of Companies House filing fees

- Payment of penalties for late filing

- Initial share capital issued during company formation

Any other transaction triggers active status. For example, receiving £1 in revenue, paying £50 for software, or recording depreciation counts as a significant transaction. Even minimal activity requires full statutory accounts instead of dormant accounts.

Companies House and HMRC operate with aligned definitions. When a company records income or expenses, it must file active accounts and potentially submit Corporation Tax returns.

Why does the definition matter for dormant company compliance?

The definition determines whether a company qualifies to file dormant accounts or must submit full statutory financial statements, directly impacting compliance obligations, filing complexity, and regulatory exposure.

Dormant status simplifies reporting. Companies file dormant accounts instead of detailed profit and loss statements. This reduces administrative workload and limits disclosure requirements. Incorrect classification leads to compliance risks. When a company files dormant accounts despite having transactions, Companies House may issue penalties. HMRC can also enforce Corporation Tax filings if activity exists.

Two compliance outcomes depend on correct classification:

- Dormant classification: simplified accounts, no Corporation Tax filing

- Active classification: full accounts, tax obligations, detailed reporting

Regulatory systems cross-check filings. For example, HMRC flags inconsistencies when bank transactions exist but dormant accounts are submitted. This increases audit risk. Accurate classification ensures legal protection. Directors maintain fiduciary responsibility for truthful reporting. Misreporting financial activity breaches statutory duties under UK company law.

Which transactions immediately disqualify a company from being dormant?

Any financial activity beyond permitted statutory exceptions disqualifies dormancy, including income generation, expense payments, loan activity, asset purchases, and liability recognition in accounting records.

Five common disqualifying transaction types include:

- Receiving revenue from sales, services, or interest income

- Paying operational expenses such as subscriptions, rent, or utilities

- Recording director loans or repayments

- Purchasing assets such as equipment or software licenses

- Incurring liabilities, including unpaid invoices or accrued expenses

Even indirect activity counts. For example, when a company pays £120 annually for a domain name, that payment is an expense. It creates an accounting entry, breaking dormancy. Bank activity often reveals non-compliance. A single transaction on a business account, such as a £10 payment, triggers the requirement for active accounts. Accounting entries matter more than intent. Even when directors consider an activity “minor,” UK law treats all financial entries equally unless explicitly exempted.

How do accounting records determine dormancy status?

Dormancy status depends on entries recorded in accounting systems, not just cash movement, meaning accruals, adjustments, and liabilities also count as significant transactions.

Accounting records include journals, ledgers, and financial statements. These records capture all financial activity, including non-cash entries.

Three accounting elements that affect dormancy:

- Accruals: recording unpaid expenses or earned income

- Depreciation: allocating asset costs over time

- Provisions: recognising expected liabilities

For example, when a company records £300 in accrued expenses for unpaid services, it creates a transaction without cash movement. This alone disqualifies dormancy. Directors often overlook non-cash entries. However, Companies House evaluates the presence of any accounting record, not just bank statements.

Accounting software automates entries. Tools like Xero or QuickBooks generate depreciation or accrual entries automatically. These entries count as significant transactions even when directors do not manually input them.

What are the legal consequences of misclassifying a company as dormant?

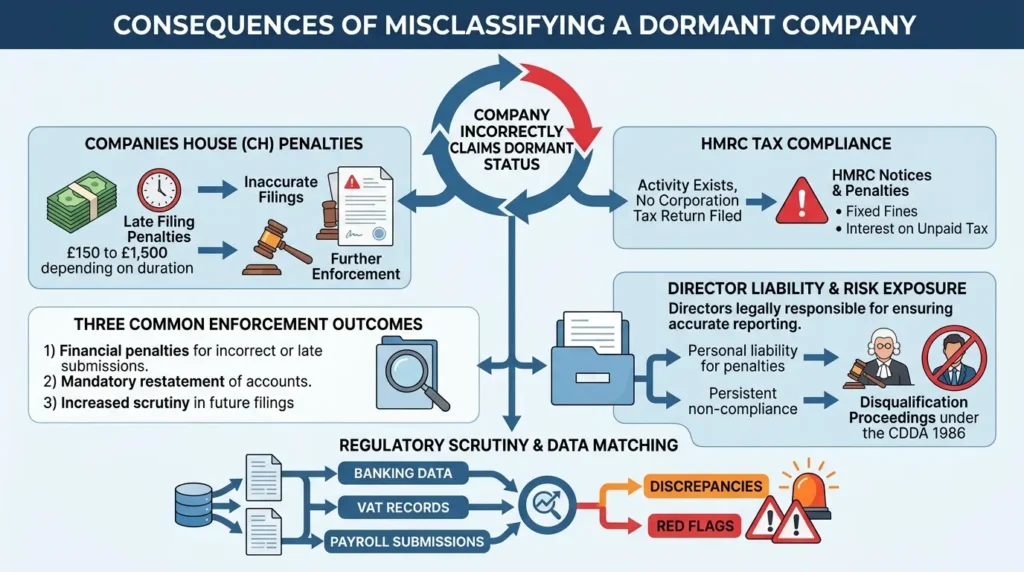

Misclassification leads to filing incorrect accounts, resulting in financial penalties, compliance investigations, and potential director liability under UK corporate governance rules.

Companies House imposes penalties for inaccurate filings. Late filing penalties range from £150 to £1,500 depending on the delay duration. Incorrect filings can trigger further enforcement. HMRC enforces tax compliance. When activity exists but no Corporation Tax return is filed, HMRC issues notices and penalties. This includes fixed fines and interest on unpaid tax.

Three enforcement outcomes commonly occur:

- Financial penalties for incorrect or late submissions

- Mandatory restatement of accounts

- Increased scrutiny in future filings

Director liability increases risk exposure. Directors are legally responsible for ensuring accurate reporting. Persistent non-compliance can result in disqualification proceedings under the Company Directors Disqualification Act 1986. Regulators rely on data matching. Banking data, VAT records, and payroll submissions provide cross-verification points. Discrepancies raise immediate red flags.

When can a company remain dormant despite limited activity?

A company remains dormant only when its financial activity is limited strictly to permitted statutory transactions, with no additional accounting entries recorded during the financial year.

Permitted activity is narrowly defined. Only three categories qualify:

- Companies House filing fees

- Late filing penalties

- Shares issued at incorporation

No operational activity is allowed. For example, registering a trademark, paying for hosting, or receiving bank interest disqualifies dormancy. Directors often assume inactivity equals dormancy. However, inactivity must align with accounting records, not just business operations.

Dormancy also applies to non-trading subsidiaries. Large corporate groups maintain dormant entities for structural purposes. These entities must strictly avoid financial transactions. Maintaining dormancy requires monitoring. Directors must review bank accounts, subscriptions, and automated payments regularly to prevent accidental activity.

Explore our ile accounts for dormant companies guides,

How to Transition Your Active Company to Dormant Status Without Legal Issues

Why Dormant Companies Must Still File a Confirmation Statement Every Single Year

How do you correctly file accounts for a dormant company?

Dormant companies file simplified accounts with Companies House, confirming no significant accounting transactions occurred, while ensuring records align with legal dormancy criteria.

The filing process includes:

- Preparing dormant accounts with a balance sheet only

- Confirming no trading or financial activity occurred

- Submitting accounts annually to Companies House

Accuracy is critical. Even a single overlooked transaction invalidates dormant status.

A structured filing approach improves compliance:

- Verify bank statements show zero operational transactions

- Validate accounting software contains no entries

- Confirm no liabilities or accruals exist

Using a specialised service reduces errors. The process to file accounts for dormant companies requires strict adherence to Companies House formatting and validation rules. Professional services ensure compliance and prevent rejection.

For a detailed breakdown of compliance risks tied to zero-balance reporting, review this guide on why accuracy is vital even when reporting zero balances to Companies House.

What is the role of professional services in maintaining dormancy compliance?

Professional filing services ensure accurate classification, validate accounting records, and submit compliant dormant accounts, reducing the risk of penalties and regulatory errors.

Dormancy compliance involves more than filing a form. It requires verification across financial systems, accounting records, and statutory requirements.

Three key service functions include:

- Validating that no disqualifying transactions exist

- Preparing compliant dormant account statements

- Submitting filings within statutory deadlines

Errors often arise from overlooked entries. For example, automated bank charges or software renewals frequently go unnoticed. Professional checks identify these risks early. The file accounts for dormant companies, and service providers perform structured validation before submission. This ensures that filings align with Companies House definitions and HMRC expectations.

For companies seeking a reliable compliance solution, the option to buy our reliable dormant filing service to keep your company records current offers a streamlined and verified approach. From My Company delivers this service with compliance-focused workflows, ensuring dormant status remains legally valid across reporting periods.

The legal definition of significant accounting transactions determines whether a company qualifies as dormant under UK law. Any financial entry beyond permitted statutory exceptions immediately changes reporting obligations and triggers full compliance requirements.

Accurate classification depends on accounting records, not assumptions about business inactivity. Even minor or non-cash entries invalidate dormancy status. This makes verification essential before filing.

From My Company ensures precise validation and compliant submission through its specialised file accounts for dormant companies service. This structured approach protects companies from penalties and maintains accurate statutory records.

Frequently Asked Questions

What are dormant company accounts in the UK?

Dormant company accounts are simplified accounts filed when a company has no significant accounting transactions during the financial year. From My Company’s File Accounts for Dormant Companies service helps ensure the filing matches UK dormant-status rules.

What counts as a significant accounting transaction for a dormant company?

A significant accounting transaction is any financial activity recorded in the company’s accounts, such as sales, expenses, loans, or asset purchases. Permitted exceptions are limited, so even small activity can remove dormant status.

Do dormant companies still have to file accounts with Companies House?

Yes, dormant companies still file annual accounts with Companies House, but the filing is shorter than full statutory accounts. The File Accounts for Dormant Companies process confirms that the company remains compliant while reporting no significant transactions.

What happens if a dormant company has a transaction?

If a dormant company records a transaction, it usually stops qualifying as dormant for that financial year. The company then files normal accounts instead of dormant accounts and may also have tax filing obligations.

Why use a dormant filing service instead of filing yourself?

A dormant filing service helps verify that no disqualifying transactions exist before submission, which reduces filing errors and compliance issues. From My Company’s File Accounts for Dormant Companies service is designed to keep records accurate and current.