The current UK VAT registration threshold is £90,000 in taxable turnover for the 12 months before registration. Businesses exceeding this must register within 30 days of awareness. This applies from April 1, 2024, unchanged into 2026.

This threshold triggers mandatory VAT registration for most small businesses. Exceeding £90,000 requires immediate compliance with HMRC rules.

What Counts as Taxable Turnover for VAT Threshold Purposes?

Taxable turnover includes all values of supplies made in the UK that HMRC taxes at standard, reduced, or zero rates. Exclude exempt supplies and disbursements. Calculate rolling 12-month totals monthly or quarterly based on payment dates.

Taxable turnover forms the core metric. HMRC defines it precisely to ensure accurate monitoring.

Businesses track sales of goods and services subject to VAT. Standard rate applies to 20% of transactions. Reduced rates cover items like energy-saving materials at 5%.

Zero-rated supplies, such as exports and certain foods, count toward the total. Exempt supplies, like financial services, do not.

Payments trigger the count. Use cash accounting if eligible. This method bases turnover on receipts, not invoices.

Monitor continuously. Exceed £90,000 anytime in 12 months? Register promptly.

Review records quarterly. Software automates calculations. Accuracy prevents penalties.

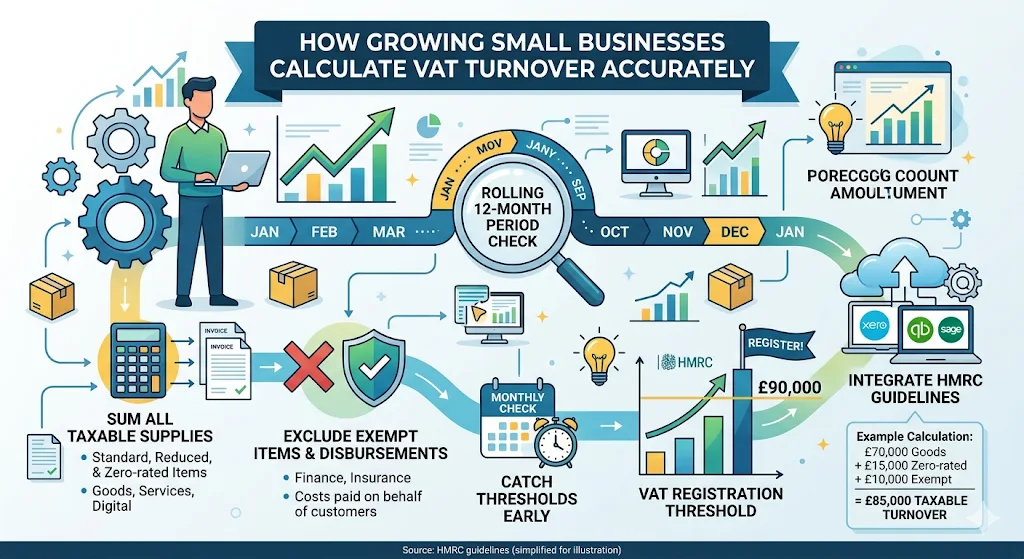

How Do Growing Small Businesses Calculate Their VAT Turnover Accurately?

Sum all taxable supplies over the past 12 months using payment dates. Subtract exempt items and disbursements. Use HMRC’s rolling period method; check monthly to catch thresholds early.

Accurate calculation demands precise records. Growing businesses scale fast. Miss a spike, face fines.

Start with the sales ledger. Identify taxable items: consultancy fees, product sales, and digital services.

Exclude VAT charged already. Focus on net values.

Apply rolling periods. January check: review February prior year to January current.

Use three methods: invoice basis for larger firms, cash for smaller, and accrual for others.

Tools like Xero or QuickBooks integrate HMRC guidelines. Export data monthly.

Example calculation: £70,000 goods (standard), £15,000 exports (zero), £10,000 finance (exempt). Total taxable: £85,000.

Adjust for partial months. Forecast growth using sales pipelines.

When Must a Small Business Register for VAT After Hitting the Threshold?

Register within 30 days of realising taxable turnover exceeds £90,000 in any rolling 12-month period. Submit online via the HMRC portal; the effective date aligns with awareness month.

Timing enforces compliance. Delay incurs penalties up to 30% of the VAT due.

Awareness triggers the clock. Review accounts monthly. Spot £90,001? Act.

HMRC accepts online applications 24/7. Processing takes 10-14 days typically.

Backdate if needed. Choose an effective date up to two years prior, but pay interest.

Voluntary registration option exists below the threshold. Benefits: reclaim input VAT.

72% of small businesses register reactively, per FSB data. Proactive monitoring cuts risks.

Prepare documents: UTR number, business details, bank info.

What Happens If Your Business Exceeds the £90,000 VAT Threshold Without Registering?

HMRC issues penalties from £100 fixed to 30% of the unpaid VAT, plus interest at 7.75% annually. Late registration triggers audits and potential director liability.

Non-compliance costs rise quickly. HMRC enforces strictly.

Fixed penalty starts at £100 for late notification. Unreasonable delay? 5-15% of VAT.

Repeated failures? 20-30% surcharges apply.

Interest accrues daily from the due date. Current base rate: 7.75%.

Audits follow. HMRC demands records back four years.

Directors face personal fines of up to £3,000 for false declarations.

Case data: 15,000+ penalties issued yearly, averaging £1,200 each, per NAO reports.

Mitigate via appeals. Show a reasonable excuse, like calculation errors.

Can Small Businesses Apply for Exceptions or Voluntary VAT Registration Below the Threshold?

Yes, register voluntarily if turnover is under £90,000 to reclaim input VAT on purchases. No exceptions to mandatory threshold; apply via HMRC Government Gateway.

Voluntary registration aids cash flow. Growing firms buy equipment and services.

Reclaim input VAT immediately. Net benefit for purchase-heavy businesses.

Apply anytime. No minimum period; deregister after 12 months if eligible.

Threshold for deregistration: £88,000 post-registration.

Consider partial exemption rules. Complex calculations apply.

FSB surveys show 22% of SMEs opt in voluntarily for growth phases.

Link to detailed processes in

How to Successfully Navigate the Complex HMRC VAT Registration Process Fast.

What Are the Main Benefits of VAT Registration for Expanding UK Small Businesses?

Registered businesses reclaim input VAT on expenses, issue compliant invoices, and access EU trade simplifications. Builds credibility with larger clients requiring VAT numbers.

Registration unlocks advantages. Expenses drop the net cost.

Reclaim 20% on office supplies, machinery, and marketing. Annual savings average £5,000-£15,000 for £200k turnover firms.

Compliant invoices attract B2B clients. 65% prefer VAT-registered suppliers, per British Chambers data.

EU sales simplify via One Stop Shop. Report quarterly.

Pricing power increases. Absorb VAT or pass to customers.

Professional image grows. Display VAT number on website, stationery.

How Does the VAT Threshold Impact Cash Flow for Growing Small Businesses?

Hitting £90,000 adds 20% VAT collection duties, straining cash until quarterly returns. Reclaims offset but requires upfront payments; plan reserves equal to two months’ output VAT.

Cash flow tightens post-registration. Collect VAT from customers. Remit to HMRC.

Quarterly payments due: 20% by month-end, 40% by month 2, 100% by month 3.

Input reclaims lag. File returns on time for refunds.

68% of SMEs report cash squeezes, per British Business Bank study.

Mitigate: stagger purchases, use VAT refund schemes.

Build reserves: estimate output VAT at 20% of sales.

Software forecasts liabilities. Adjust pricing upward by VAT.

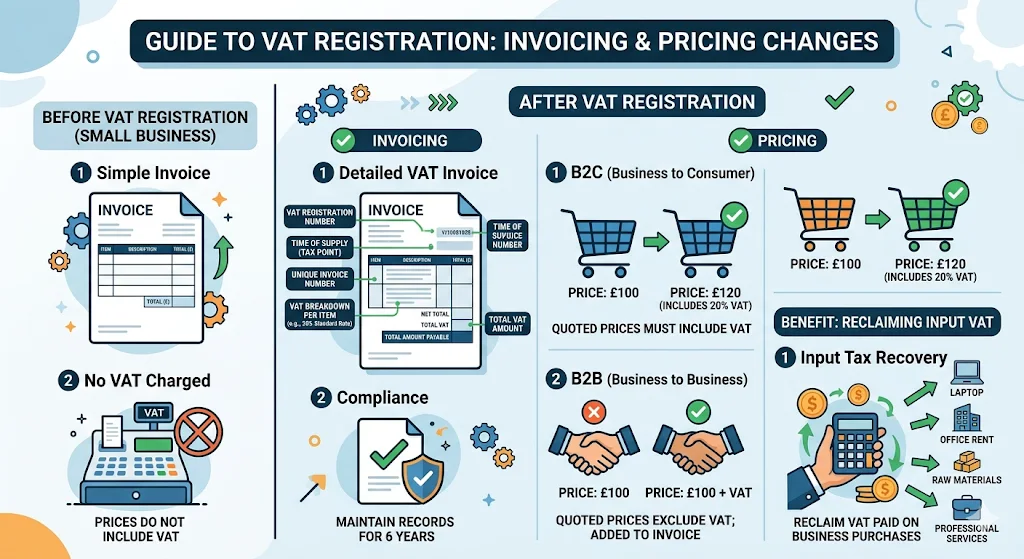

What Changes Occur to Pricing and Invoicing After VAT Registration?

Charge 20% VAT on standard supplies; update invoices with VAT number, rates, and totals. Offer VAT-inclusive pricing to customers; reclaim inputs on business costs.

Invoicing transforms. Add VAT box prominently.

Standard rate: 20% on most. Reduced: 5% on a few.

Include: unique invoice number, date, customer details, and breakdown.

Digital invoices suffice. PDF format standard.

Customer pricing: quote inclusive or exclusive. State clearly.

B2B clients reclaim; B2C absorb.

Update websites and quotes. Communicate changes via email.

Compliance audits check formats. Errors trigger corrections.

How Has the UK VAT Registration Threshold Evolved Recently for Small Businesses?

Threshold rose from £85,000 to £90,000 on April 1, 2024, frozen through 2026. Prior increases: £82k (2020), £85k (2022). Tracks inflation at 2-4% annually.

Evolution reflects policy. The government adjusts biannually.

2024 hike delayed from £90k to delay burden.

Frozen levels aid planning. No 2025/2026 rises announced.

Historical data: 2017 at £83k; steady rises since.

Impacts 15,000 new registrants yearly, HMRC stats.

Monitor Budget announcements. Autumn Statement sets the future.

Also explore,

A Complete Guide to Understanding VAT Registration for New UK Business Owners

Why Your Small Business Might Need to Register for VAT This Year

Ready to Handle VAT Registration?

VAT registration at £90,000 ensures compliance for growing small businesses. Track turnover precisely. Register on time to avoid penalties.

FormMyCompany provides VAT Registration Assistance for seamless setup. Explore VAT Registration Assistance for expert support.

Decide now with Register for VAT Today with Our Secure and Guaranteed Professional Assistance Service.

FormMyCompany delivers verified, HMRC-compliant registration using official frameworks.

Frequently Asked Questions

What is the current UK VAT registration threshold in 2026?

The UK VAT registration threshold remains £90,000 in taxable turnover for the 12 months prior to registration, unchanged since April 1, 2024. Businesses must register within 30 days of exceeding this limit. From My Company offers VAT Registration Assistance to verify calculations accurately.

How long do I have to register for VAT after hitting the threshold?

Register within 30 days of realising your taxable turnover exceeds £90,000 in any rolling 12-month period. Submit via HMRC’s online portal for fastest processing. VAT Registration Assistance from From My Company handles timely submissions to avoid penalties.

Can I register for VAT voluntarily below the £90,000 threshold?

Yes, voluntary VAT registration allows reclaiming input VAT on business purchases even under the threshold. Deregister after 12 months if turnover drops below £88,000. From My Company’s VAT Registration Assistance guides voluntary applications seamlessly.

What penalties apply for late VAT registration in the UK?

Late registration incurs fixed penalties from £100 plus up to 30% of unpaid VAT and 7.75% annual interest. HMRC audits may follow for repeated issues. Use From My Company’s VAT Registration Assistance for compliant, penalty-free registration.

What documents are needed for UK VAT registration?

Provide your UTR number, business details, bank information, and proof of turnover records. Online submission via Government Gateway processes in 10-14 days. From My Company’s VAT Registration Assistance compiles and submits all required documents accurately.