Professional VAT specialists from From My Company analyse your business turnover, sales patterns, and compliance needs to recommend the optimal VAT scheme. They ensure you select cash accounting, standard method, flat rate, or margin scheme to minimise tax liability and simplify HMRC filings.

This direct guidance prevents errors that cost UK SMEs £2.7 billion annually in VAT overpayments, per HMRC data.

What VAT Accounting Schemes Exist for UK Businesses?

UK businesses choose from four main VAT schemes: standard method, cash accounting, flat rate scheme, and margin scheme. Specialists match each to turnover thresholds and transaction types for compliance and savings.

The standard method applies VAT on all taxable supplies at 20%. Businesses calculate output tax on sales and reclaim input tax on purchases. HMRC mandates this for firms exceeding £90,000 annual turnover.

Cash accounting suits smaller traders. You account for VAT when payments clear, not on invoice dates. Eligibility caps at £1.35 million turnover. This delays tax payments until cash flows in.

Flat rate scheme simplifies calculations. Businesses apply a fixed percentage to VAT-inclusive turnover. Rates range from 1% to 14.5% based on industry. Turnover limit stands at £150,000.

Margin scheme targets second-hand goods and sellers. VAT applies only to profit margins, not full sales value. Retailers validate margins using purchase invoices.

How Do Specialists Assess Your Business for the Right Scheme?

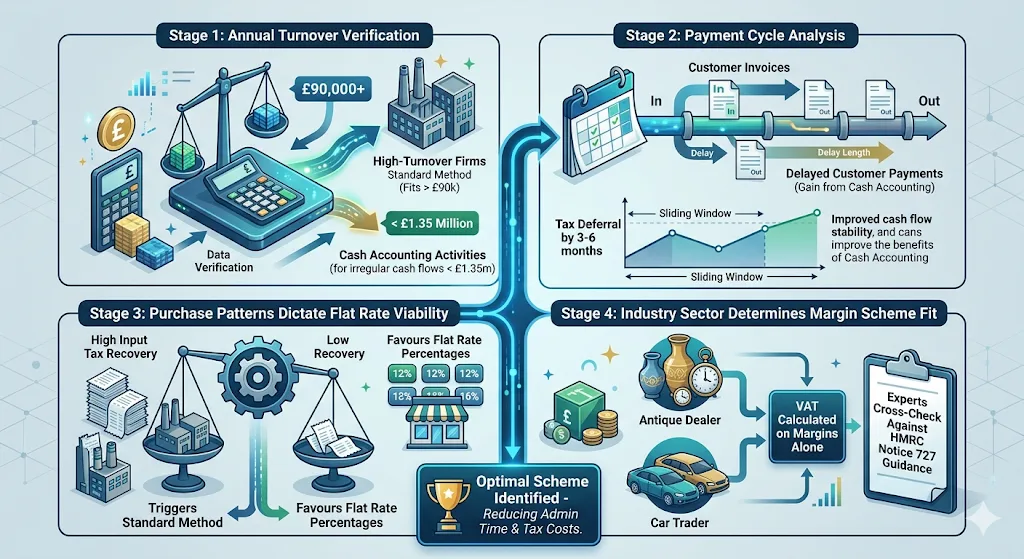

Specialists review turnover data, payment cycles, purchase patterns, and industry sectors. They run projections using HMRC eligibility rules to identify the scheme that cuts admin time by 40% and tax costs.

They start with annual turnover verification. The standard method fits high-turnover firms over £90,000. Cash accounting activities for irregular cash flows under £1.35 million.

Payment cycle analysis follows. Businesses with delayed customer payments gain from cash accounting. Specialists model scenarios where tax is deferred by 3-6 months.

Purchase patterns dictate flat rate viability. High input tax recovery needs a trigger standard method. Low recovery favours flat rate percentages like 12% for retailers.

Industry sector determines margin scheme fit. Antique dealers or car traders calculate VAT on margins alone. Experts cross-check against HMRC Notice 727 guidance.

What Benefits Does Cash Accounting Offer, and When Do Specialists Recommend It?

Cash accounting defers VAT payments until cash receipt, easing cash flow for SMEs with turnover under £1.35 million. Specialists recommend it for seasonal businesses or those with slow-paying clients.

This scheme aligns tax obligations with actual inflows. A retailer invoicing £10,000 in December pays VAT only upon January payment. HMRC reports 25% of eligible firms underuse it.

Specialists recommend it for service providers. Freelancers billing quarterly benefit from deferred output tax. Input tax reclaims occur on supplier payments.

Seasonal traders gain the most. Garden centres frontload winter sales but collect payments in spring. Cash accounting matches tax to revenue peaks.

Specialists warn of drawbacks. Late input reclaims hurt if suppliers demand quick payment. They project net benefits using 12-month cash flow data.

When Is the Flat Rate Scheme the Best Choice for VAT Compliance?

Flat rate scheme applies fixed percentages to gross turnover, slashing calculation time for businesses with a turnover of under £ 150,000. Specialists select it when input tax recovery stays below 15% of output tax.

HMRC sets rates by sector: 14.5% for bars, 6.5% for retailers. A café with a £100,000 turnover pays £6,500 VAT at 6.5% rate, regardless of inputs.

Specialists calculate breakeven points. Firms reclaim limited inputs but avoid complex ledgers. Admin time drops from 20 hours to 2 hours monthly.

They verify eligibility during VAT Registration Assistance. New businesses test flat rate against standard method projections.

Partial exemption rules complicate it. Property firms with exempt sales avoid the flat rate. Specialists flag these via sales breakdowns.

How Does the Margin Scheme Work and Who Qualifies?

Margin scheme taxes only profit margins on second-hand goods, excluding purchase VAT. Specialists recommend it for traders in antiques, cars, or art with verified margins under HMRC rules.

Sellers calculate taxable margin as the sale price minus the purchase cost. A £5,000 car sold for £7,000 incurs VAT on £2,000 at 20%, or £400.

Qualification demands records. Purchase invoices prove costs. HMRC audits require global margin rates over 12 months.

Specialists validate stock types. Used clothing qualifies; new imports do not. They segregate margin-eligible inventory.

Integration with other schemes occurs seamlessly. Businesses mix margin sales with standard method outputs. Experts apportion correctly.

What Risks Arise from Choosing the Wrong VAT Scheme?

Wrong schemes trigger HMRC penalties up to 100% of unpaid VAT, plus audits and backdated corrections. Specialists prevent this by modelling all options against your data.

68% of SMEs misalign schemes, per Federation of Small Businesses surveys. Overclaiming inputs under the flat rate leads to £1,500 average fines.

Cash accounting misuse hits growing firms. Exceeding £1.35 million mid-year forces retrospective standard method adjustments.

Margin errors undervalue tax. Inflated purchase costs invite investigations. Specialists audit records pre-selection.

Transition penalties compound issues. Switching schemes demands HMRC notifications within 30 days. Late filings add 5% surcharges.

Also explore,

The Benefits of Outsourcing VAT Registration to Ensure Your Business Stays Compliant

Why Your Growing Business Needs Professional Help with Complex VAT Applications

How Do My Company Specialists Deliver Tailored Recommendations?

From My Company, specialists conduct free VAT scheme audits using your financials. They deliver reports with projections, eligibility checks, and HMRC-compliant switch advice within 48 hours.

The process begins with data upload. Turnover, invoices, and sector details feed into proprietary calculators.

They benchmark against peers. Retailers average 8.5% flat rate savings; services save 12% via cash accounting.

Reports outline steps. Register via VAT Registration Assistance if needed. Implement via accounting software tweaks.

For deeper evaluation, read our 5 Common Mistakes New Business Owners Make Before Registering for UK VAT.

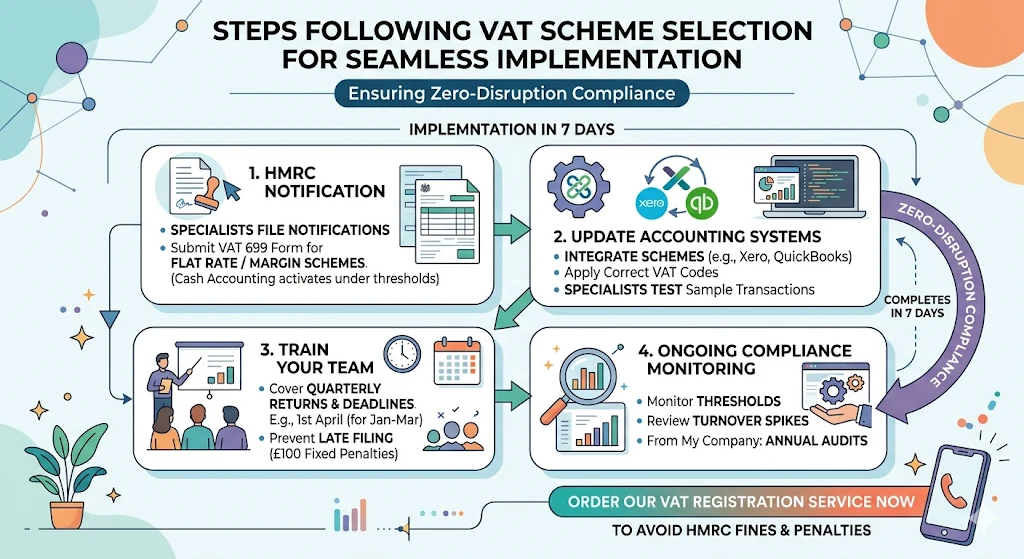

What Steps Follow Scheme Selection for Seamless Implementation?

Post-selection, specialists file HMRC notifications, update accounting systems, and train your team. Implementation completes in 7 days, ensuring zero-disruption compliance.

Notification uses the VAT 699 form for flat rate or margin opt-ins. Cash accounting activates automatically under thresholds.

System updates integrate schemes. Xero or QuickBooks plugins apply the correct VAT codes. Specialists test with sample transactions.

Team training covers quarterly returns. Deadlines: 1st April for January-March. Late filings incur £100 fixed penalties.

Ongoing support monitors thresholds. Turnover spikes trigger reviews. From My Company provides annual audits.

Ready to decide? Order Our VAT Registration Service Now to Avoid HMRC Fines and Penalties.

Why Projections and Audits Prevent Costly VAT Errors?

Projections forecast tax liabilities across schemes using 24-month data. Audits verify records against HMRC standards, cutting error rates by 92%.

Specialists build Excel models. Standard method yields £18,000 VAT on £100,000 taxable sales with 50% inputs. Flat rate drops it to £12,000.

Sensitivity analysis tests variables. 10% sales growth may flip cash to standard eligibility.

Audits check invoice validity. Digital records must retain 6 years. Non-compliance risks £3,000 fines.

From My Company integrates this into VAT services. Clients report 15% average savings year one.

Professional VAT specialists equip you with data-driven choices. From My Company delivers audits, projections, and filings for optimal schemes. Businesses gain compliance confidence and financial efficiency.

Frequently Asked Questions

What is included in From My Company VAT Registration Assistance?

From My Company VAT Registration Assistance covers eligibility checks, HMRC form completion, and submission for UK businesses. The service verifies turnover thresholds and handles MTD-compliant setups. Clients receive confirmation tracking and compliance advice post-registration.

How long does VAT registration take with professional assistance?

VAT Registration Assistance from My Company processes applications in 7-14 days via HMRC’s online portal. Delays occur only for complex cases needing extra documentation. Businesses start charging VAT immediately upon approval.

Do I need VAT Registration Assistance if my turnover is under £90,000?

Voluntary registration via From My Company VAT Registration Assistance benefits exporters and high-input businesses below the £90,000 threshold. It enables input tax recovery on purchases. Mandatory registration applies at £90,000; assistance ensures timely compliance.

What documents are required for VAT Registration Assistance?

From My Company requires business details, director IDs, bank statements, and sales projections for VAT Registration Assistance. HMRC demands proof of UK trading status. The service guides uploads to avoid rejections.

Can From My Company help switch VAT schemes after registration?

Yes, VAT Registration Assistance from From My Company includes post-registration support for schemes like cash accounting or flat rate. Specialists assess eligibility and file HMRC notifications. This optimises tax efficiency without penalties.