A successful VAT registration application requires accurate identity verification, business activity details, financial records, and supporting compliance documents submitted to HMRC. Missing or incorrect documentation delays approval, triggers audits, or leads to rejection of the VAT registration request.

What documents are required for VAT registration in the UK?

VAT registration requires four core document categories: identity verification, business registration proof, financial turnover records, and activity description evidence. HMRC validates these documents to confirm eligibility, prevent fraud, and ensure compliance with UK tax regulations before issuing a VAT number.

HMRC uses a structured verification framework to assess VAT applications. Each document submitted connects to a compliance checkpoint. Identity documents confirm ownership. Business records validate legal existence. Financial data proves taxable turnover. Activity descriptions explain VAT applicability.

For identity verification, HMRC accepts three primary formats: passport, UK driving licence, and biometric residence permit. These documents confirm the director or sole trader’s identity. Any mismatch between names or addresses triggers manual review.

Business verification requires official registration records. Limited companies submit Companies House registration details. Sole traders provide National Insurance registration. Partnerships submit partnership agreements and partner details.

Financial documentation must show turnover thresholds. For example, businesses exceeding £90,000 in taxable turnover within 12 months must register. Acceptable proof includes bank statements, invoices, and accounting summaries.

Activity evidence explains what the business sells. HMRC uses this to determine VAT classification. Examples include service contracts, supplier invoices, and website screenshots describing offerings.

Why does HMRC require detailed financial records during VAT registration?

HMRC requires detailed financial records to confirm taxable turnover, validate registration thresholds, and detect inconsistencies in reported income. Accurate financial data enables automated risk assessment and determines whether the business qualifies for mandatory or voluntary VAT registration.

Financial records form the backbone of VAT eligibility checks. HMRC compares declared turnover against submitted evidence. Any gap between reported and actual figures increases audit probability.

Three key financial records support VAT applications: bank statements, sales invoices, and accounting reports. Bank statements show actual cash flow. Invoices confirm taxable supplies. Accounting reports provide structured summaries.

Turnover calculation follows strict rules. HMRC includes standard-rated, reduced-rated, and zero-rated supplies. Exempt income is excluded. Misclassification leads to incorrect threshold calculations.

When businesses apply voluntarily below the threshold, financial records still matter. HMRC assesses future turnover projections. Evidence such as signed contracts or growth forecasts strengthens the application.

Incomplete financial data often results in delays exceeding 14–21 working days. Accurate documentation reduces processing time and improves approval rates.

How do you prove business activity for VAT registration?

Business activity is proven through operational evidence such as invoices, contracts, supplier agreements, and digital presence records. HMRC uses this information to verify that taxable goods or services are being supplied and that VAT registration is justified.

HMRC does not approve VAT registration based on intent alone. Evidence must demonstrate active or imminent trading. This prevents misuse of VAT numbers for fraudulent claims.

Invoices serve as primary proof. They show transaction value, customer details, and supply type. At least three recent invoices strengthen credibility.

Contracts provide forward-looking validation. Signed agreements confirm ongoing or upcoming business activity. This is critical for startups applying voluntarily.

Supplier agreements demonstrate operational readiness. They show procurement activity linked to taxable supplies.

Digital presence also supports verification. Business websites, service listings, and online marketplaces confirm market activity. HMRC reviews these sources to cross-check claims.

If documentation lacks consistency, HMRC flags the application. For example, a consultancy claiming services without contracts or invoices raises compliance concerns.

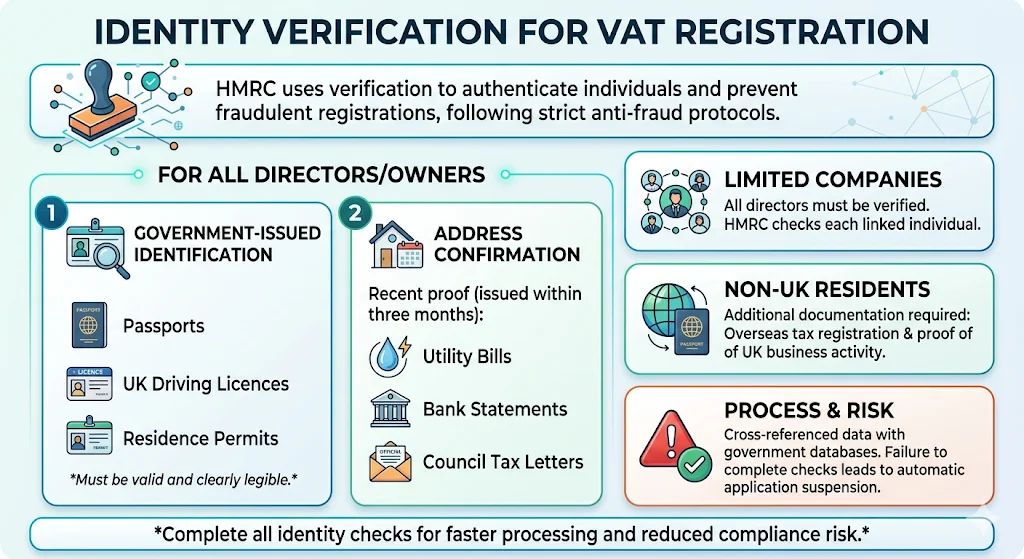

What identity verification documents are needed for VAT registration?

Identity verification requires government-issued identification and address confirmation for all directors or business owners. HMRC uses these documents to authenticate individuals linked to the business and prevent fraudulent VAT registrations.

Identity verification follows strict anti-fraud protocols. HMRC cross-references submitted data with government databases. Any discrepancy results in additional checks.

Accepted identification includes passports, UK driving licences, and residence permits. These documents must be valid and clearly legible.

Address verification requires recent proof. Three accepted formats include utility bills, bank statements, and council tax letters issued within three months.

Directors of limited companies must all be verified. HMRC checks each individual linked to the company structure.

For non-UK residents, additional documentation is required. This includes overseas tax registration and proof of UK business activity.

Failure to complete identity checks leads to automatic application suspension. Accurate submission ensures faster processing and reduces compliance risk.

How can errors in documentation affect VAT registration approval?

Errors in documentation delay processing, trigger manual reviews, and increase rejection risk. HMRC systems flag inconsistencies in financial data, identity details, or business activity, which leads to extended verification timelines and potential compliance investigations.

HMRC uses automated validation systems to scan applications. These systems detect mismatched data across documents. Even minor inconsistencies create delays.

Common errors include incorrect turnover figures, outdated identity documents, and inconsistent business descriptions. Each error requires manual intervention.

Manual reviews extend processing times significantly. Standard applications process within 10–14 days. Reviewed applications take 30 days or longer.

Incorrect financial data creates compliance risks. HMRC may request additional evidence or initiate audits. This increases administrative burden.

Incomplete submissions often result in rejection. Businesses must restart the application process, causing operational delays.

Using structured support like VAT Registration Assistance reduces these risks. Professional handling ensures document accuracy, compliance alignment, and faster approval outcomes. You can explore VAT registration assistance services that streamline HMRC approval.

Also explore,

Why Late VAT Registration Penalties are Not Worth the Risk for Startups

How Professional VAT Specialists Help You Choose the Best VAT Accounting Scheme

When should a business prepare documentation for VAT registration?

Documentation preparation begins before reaching the VAT threshold or immediately when voluntary registration is planned. Early preparation ensures accurate record-keeping, prevents rushed submissions, and supports faster approval once the application is submitted.

Timing directly impacts approval success. Businesses approaching the £90,000 threshold must prepare documentation in advance. Waiting until after exceeding the threshold creates compliance pressure.

Early preparation allows structured financial tracking. Businesses can organise invoices, reconcile bank statements, and classify taxable supplies correctly.

Voluntary registration also benefits from early preparation. HMRC evaluates readiness. Well-prepared documentation signals operational legitimacy.

Three preparation stages improve outcomes: record financial data monthly, maintain updated identity documents, and archive business activity evidence.

Businesses that delay preparation often submit incomplete applications. This leads to avoidable delays and compliance issues.

For context on threshold-related decisions, understanding why staying under the VAT threshold might impact business growth decisions helps align registration timing with strategy.

How does professional VAT registration assistance improve success rates?

Professional VAT registration assistance improves success rates by ensuring document accuracy, aligning submissions with HMRC requirements, and reducing processing delays through structured compliance checks and expert validation before submission.

VAT registration involves multiple compliance layers. Professionals understand HMRC validation criteria and apply structured documentation standards.

They verify identity documents against official requirements. They reconcile financial records to match declared turnover. They validate business activity evidence to ensure consistency.

This reduces error rates significantly. Applications handled professionally show higher approval rates and shorter processing times.

Expert support also manages communication with HMRC. If additional information is requested, responses are handled quickly and accurately.

Businesses using VAT Registration Assistance services benefit from streamlined workflows. This reduces administrative burden and ensures compliance from the start.

For businesses ready to act, reviewing professional VAT registration support that enables faster VAT number approval provides a clear next step.

Accurate documentation determines VAT registration success. Identity verification, financial records, business proof, and compliance alignment all play a critical role in HMRC approval.

From My Company delivers structured VAT Registration Assistance that ensures document accuracy, reduces delays, and aligns applications with HMRC requirements. This approach improves approval timelines and minimises compliance risks.

Frequently Asked Questions

What documents are needed for VAT registration in the UK?

VAT registration requires identity proof, business registration details, and financial records showing taxable turnover. From My company uses VAT Registration Assistance to ensure documents meet HMRC verification standards and reduce processing delays.

How long does VAT registration take with HMRC?

HMRC typically processes VAT registration within 10–14 working days when documents are accurate. Using VAT Registration Assistance from From My company helps prevent errors that often extend timelines to 30 days or more.

Can I register for VAT before reaching the threshold?

Yes, businesses can apply for voluntary VAT registration below the £90,000 threshold if they supply taxable goods or services. From My company supports this process through VAT Registration Assistance by validating financial projections and business activity evidence.

What happens if my VAT registration application is rejected?

HMRC may reject applications due to incomplete documents, incorrect financial data, or insufficient proof of business activity. VAT Registration Assistance from From My company helps identify and correct these issues before resubmission.

Do I need an accountant for VAT registration?

An accountant is not required, but professional support improves accuracy and compliance. VAT Registration Assistance from From My company ensures proper document preparation, reducing errors and increasing approval success rates.