To transition an active company to dormant status without legal issues, cease all trading activity, settle financial obligations, notify HMRC of inactivity, and file dormant accounts with Companies House. Maintain compliance by submitting annual confirmation statements and accurate records to avoid penalties.

What does it mean for a company to become dormant?

A company becomes dormant when it has no significant accounting transactions during a financial year, excluding specific statutory payments such as Companies House filing fees, penalties, or shares issued during formation. HMRC and Companies House both define dormancy with strict compliance criteria.

Dormant status applies when a company stops trading completely. This includes halting sales, purchases, payroll, and investments. Even one unauthorised transaction, such as bank interest or subscription fees, invalidates dormant classification.

Companies House and HMRC operate separate definitions. Companies House focuses on accounting transactions. HMRC focuses on trading activity. A company must meet both definitions to remain compliant.

Dormant companies still exist legally. They must maintain statutory records and file annual documents. This includes confirmation statements and dormant accounts.

Why do companies transition to dormant status?

Companies transition to dormant status to pause operations while maintaining legal registration, reduce administrative costs, protect a business name, or prepare for future restructuring, acquisitions, or relaunch strategies without dissolving the entity.

Business owners use dormancy during strategic pauses. For example, directors halt trading while exploring new markets or awaiting funding approval.

Dormant status avoids full compliance burdens. Active companies file full accounts and tax returns. Dormant companies file simplified accounts, reducing accounting costs by up to 60% based on UK SME averages.

Some directors retain dormant companies to secure branding rights. Others use them for intellectual property holding structures or to delay operational launch.

What steps are required to transition to dormant status legally?

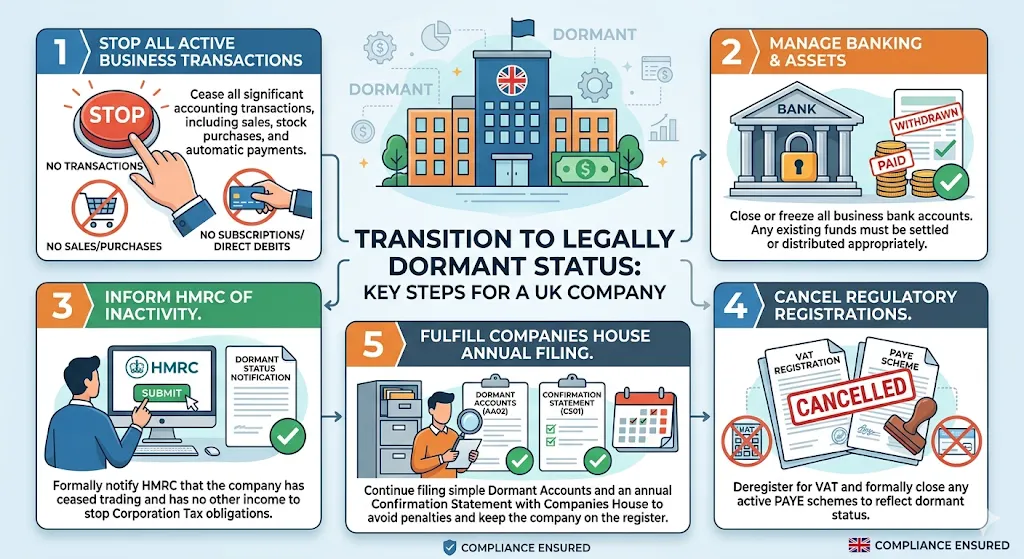

To legally transition, stop all transactions, close or freeze business bank accounts, notify HMRC of inactivity, cancel VAT and PAYE registrations, and prepare dormant accounts. Each step ensures compliance with UK regulatory frameworks and avoids financial or legal penalties.

Stopping transactions is the first requirement. This includes direct debits, loan repayments, and subscription services. Even small automated payments invalidate dormancy.

Directors must inform HMRC that the company has stopped trading. This action prevents Corporation Tax obligations. HMRC then updates the company’s status internally.

VAT and PAYE schemes must be cancelled if registered. Active tax schemes indicate operational status. Removing them aligns with dormancy classification.

Companies House requires the submission of dormant accounts annually. Directors can use the File Accounts for Dormant Companies service to ensure correct formatting and compliance with filing standards.

How do you ensure compliance during the dormant period?

Compliance during dormancy requires filing annual confirmation statements, submitting dormant accounts on time, maintaining statutory registers, and avoiding any financial transactions that breach dormancy conditions under Companies House and HMRC rules.

Dormant companies must still file a confirmation statement every 12 months. This verifies company details such as directors, shareholders, and registered address.

Dormant accounts must be submitted annually. These accounts contain a balance sheet and limited notes. Missing deadlines results in penalties starting at £150 and increasing up to £1,500.

Directors must maintain statutory records. This includes registers of members and persons with significant control (PSC). These records must remain accurate and accessible.

No financial activity is allowed. This includes receiving income or paying expenses. Even a single transaction, such as £1 bank interest, breaches compliance.

Using the File Accounts for Dormant Companies service ensures correct submission formats and reduces rejection risk by Companies House.

What common mistakes cause legal issues when transitioning to dormancy?

Legal issues arise when companies continue minor transactions, fail to notify HMRC, submit incorrect accounts, or misunderstand dormancy definitions. These errors trigger penalties, compliance investigations, or forced reclassification as an active company.

One common mistake involves leaving bank accounts active. Automated charges, such as software subscriptions or bank fees, count as transactions.

Another issue involves failing to inform HMRC. If HMRC expects a Corporation Tax return, missing it leads to penalties starting at £100 and increasing with delays.

Incorrect account filing also creates problems. Dormant accounts must follow specific templates. Submitting micro-entity or full accounts instead results in rejection.

Some directors misunderstand allowed transactions. Only three categories are permitted: Companies House fees, penalties, and shares issued during incorporation.

Learning how professionals handle compliance improves accuracy. This guide on how accountants streamline dormant company reporting explains structured processes used by experts.

How long can a company remain dormant?

A company can remain dormant indefinitely as long as it meets all compliance requirements, files annual documents, and avoids any disqualifying transactions. There is no statutory time limit imposed by Companies House or HMRC for dormancy duration.

Many companies stay dormant for several years. This is common in holding structures or inactive subsidiaries within corporate groups.

Companies House does not impose a dormancy limit. However, failure to file the required documents leads to strike-off proceedings. This removes the company from the register.

Directors must assess whether dormancy still serves a business purpose. Maintaining a dormant entity incurs administrative obligations, even if reduced.

If a company resumes activity, it must inform HMRC immediately. Trading restarts Corporation Tax obligations and changes filing requirements.

Also explore,

Why Dormant Companies Must Still File a Confirmation Statement Every Single Year

The Essential Checklist for Maintaining a Dormant Limited Company in the UK

When should you consider professional support for dormant company filings?

Professional support becomes essential when directors lack compliance knowledge, manage multiple entities, or want to avoid filing errors. Accountants ensure accurate submissions, reduce rejection rates, and maintain regulatory alignment with UK corporate laws.

Dormant filings appear simple but contain technical requirements. Errors in balance sheet formatting or missing notes cause rejection.

Professional services streamline the process. Accountants validate data, prepare compliant documents, and submit filings within deadlines.

Directors managing multiple companies benefit significantly. Handling five or more entities increases administrative complexity and error risk.

For decision-ready support, explore dormant company account submission services designed for accuracy and speed.

From My Company provides structured compliance services tailored to UK regulatory requirements. Their File Accounts for Dormant Companies service ensures submissions meet Companies House standards while reducing administrative burden.

Transitioning an active company to dormant status requires precise actions: stop transactions, notify HMRC, cancel tax registrations, and file compliant dormant accounts. Errors in any step trigger penalties or reclassification.

Dormancy offers operational flexibility and cost reduction when managed correctly. It preserves company registration while eliminating active reporting obligations.

From My Company delivers compliance-focused solutions through its File Accounts for Dormant Companies service. This ensures accurate submissions, regulatory alignment, and reduced administrative risk for directors managing dormant entities.

Frequently Asked Questions

What are dormant company accounts and when must they be filed?

Dormant company accounts are simplified financial statements submitted to Companies House when a business has no significant transactions. Using a service like File Accounts for Dormant Companies ensures these are filed annually and on time to maintain compliance.

Do dormant companies still need to file accounts every year?

Yes, dormant companies must file accounts every year even if there is no trading activity. File Accounts for Dormant Companies helps ensure submissions meet Companies House requirements and avoid late filing penalties.

What qualifies a company as dormant in the UK?

A company is considered dormant if it has no significant accounting transactions during a financial year, except for specific allowed entries. From My company supports directors in verifying eligibility before using the File Accounts for Dormant Companies service.

What happens if dormant accounts are filed late?

Late filing results in automatic penalties starting from £150 and increasing based on the length of the delay. Using File Accounts for Dormant Companies reduces the risk of missed deadlines and ensures accurate submission.

Can I file dormant company accounts myself or do I need a service?

Directors can file dormant accounts themselves, but errors in formatting or missing details often lead to rejection. From My company provides File Accounts for Dormant Companies to ensure compliance, accuracy, and faster processing.