UK limited company directors pay themselves a salary through PAYE by registering with HMRC, setting up a payroll scheme, deducting tax and NI contributions, and reporting via Real Time Information (RTI). This complies with tax rules and builds state pension entitlement. From My Company streamlines registration.

What Legal Requirements Apply to Director Salaries?

Directors register for PAYE within three months of starting payroll. HMRC mandates RTI submissions on or before each payday. Salaries count as allowable business expenses, reducing corporation tax liability.

Directors follow Companies House and HMRC rules. Register the company first if new. PAYE applies once you pay a salary.

PAYE covers income tax and National Insurance. Directors pay Class 1 NI contributions like employees. Use official rates from HMRC.

68% of UK SMEs use director salaries below the £12,570 tax-free threshold annually. This avoids income tax. Higher salaries trigger deductions.

HMRC audits non-compliant payroll. Penalties reach £3,000 per month for late RTI. Register early to comply.

Directors verify identity during PAYE setup. Submit the director’s details via HMRC online services. Approval takes up to five working days.

Why Register for PAYE Before Paying Salary?

PAYE registration creates your payroll scheme with HMRC. It enables legal salary payments and RTI reporting. Without it, HMRC fines apply, and salaries become undeclared dividends.

Start payroll only after scheme approval. HMRC assigns a unique payroll reference.

Registration prevents tax evasion claims. Courts rule irregular payments as loans if unregistered. Repay with interest.

PAYE builds NI credits. Directors qualify for a state pension after 35 years. Salaries count toward this record.

97% of compliant directors avoid HMRC investigations. Use the government gateway for secure access.

Link salary to employment contract. Draft a simple agreement stating the role and pay. Sign before the first payment.

How Do You Register Your Company for PAYE?

Register online via HMRC’s government gateway. Provide the company UTR, the director’s details, and the start date. Receive payroll reference instantly or within days. From My Company offers PAYE Registration Assistance to handle submissions.

Access gov.uk/paye-registration. Create or log in to the government gateway account.

Enter company details: CRN, UTR, and address. List paying directors and employees.

Select start reason: new payroll or threshold reached. £123 weekly PAYE liability triggers mandatory registration.

HMRC reviews submission. Activate the scheme for payments. Download payslips and reports.

Three common errors delay approval: mismatched UTR, missing NI numbers, and incomplete director verification. Double-check forms.

What Salary Amount Maximises Tax Efficiency?

The optimal salary sits at £12,570 personal allowance for 2026/27. Pay via PAYE to claim expenses and NI credits. Combine with dividends for total remuneration up to the £50,270 basic rate band.

Calculate based on tax bands. £12,570 incurs zero income tax. NI starts at £242 weekly.

Directors save 19% corporation tax on salary costs. Example: £12,570 salary is deducted fully from profits.

Compare options: pure salary, salary plus dividends, or dividends only. Salary plus dividends minimises overall tax for most.

HMRC data shows 72% of directors choose £8,000-£12,570 salary. Adjust yearly with Budget changes.

Run calculations using the HMRC tax calculator. Factor in the child benefit charge if income exceeds £60,000.

How Do You Set Up Payroll for Director’s Salary?

Install HMRC-approved payroll software or use bureau services. Calculate gross pay, tax, NI each period. Submit Full Payment Submission (FPS) via RTI before or on payday.

Choose software like HMRC’s Basic PAYE Tools (free for under 10 employees). Input salary details.

Directors process monthly or bi-weekly. Run payroll on fixed dates.

Deduct 20% income tax on amounts over allowance. Employee NI at 8%, employer at 13.8%.

Issue payslip showing breakdowns: gross £1,047 monthly equals £12,570 yearly. Retain records six years.

Bank transfer net pay. Reconcile employer NI quarterly via EPS if nil.

What Steps Follow Monthly Salary Payments?

Submit RTI FPS each payday with payment details. Pay HMRC deductions by 22nd next month (electronic) or 19th (post). Reconcile year-end with P60 and P11D forms.

FPS reports earnings, deductions, hours. Use software auto-submission.

Three payment methods: Bacs, Cheque, Cash (rare). HMRC prefers Faster Payments.

Track via HMRC online account. View payment history and forecasts.

Year-end tasks: issue P60 by 31 May. File final FPS by 19 April post-year-end.

Audit trail prevents disputes. Store payslips digitally with timestamps.

How Do You Handle Tax and NI Deductions Correctly?

Withhold income tax at source using a cumulative basis. Deduct employee NI Class 1 from £12,570 threshold. Pay employer NI on full salary above the secondary threshold of £175 weekly.

Use PAYE tables or software for precision. Monthly tax code 1257L standard.

Example: £1,047 monthly salary. Zero tax, £58 employee NI, £123 employer NI.

Reclaim overpayments via adjustment. HMRC refunds within 30 days.

Directors report benefits-in-kind on P11D. Cars, phones add to taxable pay.

Comply with auto-enrolment pensions. Deduct 5% minimum from salary.

What Records Must You Maintain for Compliance?

Keep payroll records for six years: payslips, FPS submissions, payment proofs. Include contracts, NI numbers, tax codes. HMRC inspects on request.

Digital storage suffices. Use a secure cloud compliant with GDPR.

List key documents: starter checklist, leaver forms, MTD evidence.

72% of fines stem from poor records. Scan and index files.

Annual review checks accuracy. Update for rate changes.

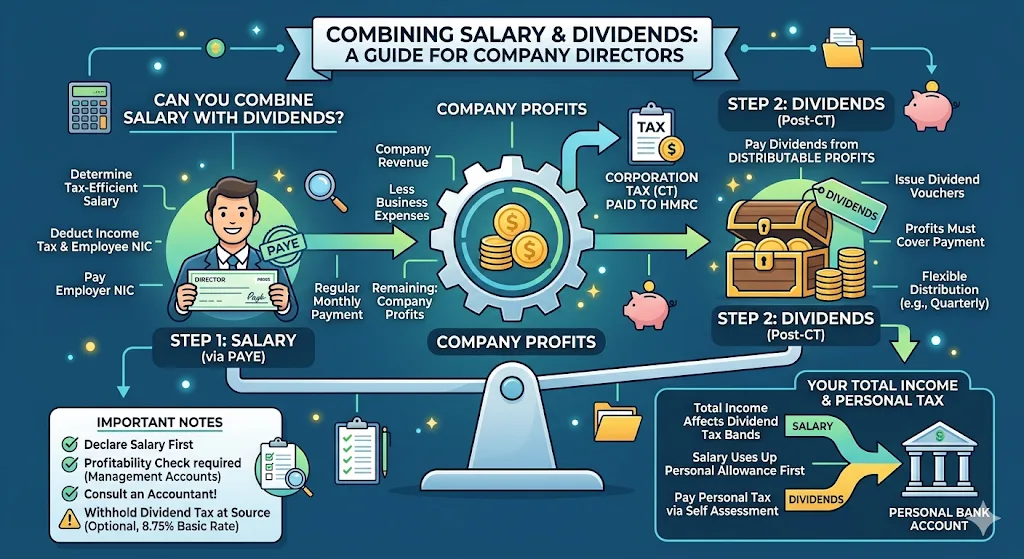

Can You Combine Salary with Dividends?

Yes, pay a tax-efficient salary, then dividends from profits. Salary via PAYE; dividends post-CT with voucher. Total income affects dividend tax bands.

Declare salary first. Profits after salary qualify for dividends.

Distribute quarterly. Withhold 8.75% basic rate tax at source, optional.

Caps apply: profits cover dividends. Track via management accounts.

What Are Common Pitfalls to Avoid?

Avoid irregular payments without RTI. Skip the bureau if a simple setup. Missed deadlines trigger £100-£400 fines per month.

Three pitfalls: unregistered payroll, wrong tax codes, and late payments.

Verify NI numbers before starting. Update addresses promptly.

How Does Professional Help Simplify This?

Outsource PAYE registration and setup to experts. They submit forms, provide software guidance, and ensure RTI compliance. Saves 10-15 hours monthly.

Professionals handle HMRC liaison. Access templates and audits.

Read more on time savings in How Our PAYE Assistance Saves You Hours of Admin with HMRC.

Decide with Get Your UK Business PAYE Ready – Professional Registration.

My Company delivers PAYE Registration Assistance with verified compliance.

Frequently Asked Questions

How do I register for PAYE as a UK limited company director?

Register for PAYE online via HMRC’s Government Gateway using your company’s UTR and director details. Submit within three months of starting payroll to receive a unique payroll reference. From My Company provides PAYE Registration Assistance to ensure accurate submission and quick HMRC approval.

What is PAYE registration and why do companies need it?

PAYE registration sets up a payroll scheme with HMRC for deducting income tax and National Insurance from salaries. UK limited companies require it before paying directors or employees to comply with RTI reporting rules. It prevents fines up to £3,000 for non-compliance.

What documents are needed for PAYE registration assistance?

Provide company CRN, UTR, director NI numbers, and proof of identity for PAYE registration. HMRC requires accurate details to activate the payroll scheme. Services like From My Company’s PAYE Registration Assistance guide document preparation.

Can From My Company help with PAYE setup after registration?

Yes, from My Company’s PAYE Registration Assistance extends to payroll software setup and initial RTI submissions. This ensures seamless compliance with HMRC rules for director salaries. It covers ongoing admin for UK limited companies.

How long does PAYE registration take with HMRC?

HMRC processes PAYE registrations in up to five working days after online submission. Instant references appear for simple cases via the Government Gateway. From My Company’s PAYE Registration Assistance handles verification to speed up approval.