Your UK limited company qualifies as dormant if it conducts no significant accounting transactions during the financial year, such as issuing shares, paying interest, or receiving dividends. Companies House defines this under Section 1169 of the Companies Act 2006. File dormant accounts to confirm status.

This status exempts companies from full audits and detailed financial statements. Directors maintain compliance by filing simplified forms annually.

What Defines a Dormant Company Under UK Law?

A dormant company performs no significant transactions, per Companies House criteria: no share allotments, no interest payments or receipts, no debt-related payments, and no significant sums credited to accounts.

Section 1169 of the Companies Act 2006 sets this standard. Companies House uses it to classify inactivity.

Dormant status applies to limited companies registered in England, Wales, Scotland, or Northern Ireland. It covers private limited companies (Ltd) and public limited companies (PLC).

Transaction types exclude trivial administrative activities. For example, bank fees under £100 do not trigger activity. Review annual accounts to identify these.

Directors verify status before filing. Use Companies House guidance for precise checks.

Which Transactions Prevent Dormant Classification?

Transactions disqualifying dormancy include allotting shares, paying or receiving interest, settling debts or claims, and crediting significant sums to ledgers. Even one such event activates the company.

The Companies Act 2006 lists these explicitly. Banks report interest automatically.

Share allotments count regardless of value. Directors record them in statutory registers.

Interest payments arise from loans or overdrafts. Receipts from investments also qualify.

Debt settlements cover supplier invoices or loans. Claims include legal settlements.

Significant sums mean amounts over nominal fees. HMRC provides thresholds in guidance.

What Counts as Non-Significant Activity?

Bank charges, filing fees to Companies House, and minor stationery costs under £100 remain non-significant. These preserve dormancy if no other transactions occur.

Companies House exempts routine administrative costs. Verify against annual bank statements.

Bank charges accrue monthly. They total under 1% of turnover for dormant firms.

Filing fees pay for confirmation statements. Submit the WebFiling CH1 form annually.

Stationery purchases support compliance. Limit to essential items like paper.

Cross-check the ledgers quarterly. This prevents accidental activation.

How Do You Check Your Company’s Transaction History?

Examine bank statements, ledgers, and registers for the financial year. Confirm absence of disqualifying transactions using Companies House checklists.

Access online banking portals first. Download 12-month statements.

Review purchase ledgers for payments. Scan sales ledgers for receipts.

Inspect share registers for allotments. Check director loan accounts.

Use accounting software exports. Filter by date range.

Companies House dormant checklist lists 12 criteria. Match records against it.

What Documents Prove Dormant Status?

Prepare bank statements, cash book extracts, and director minutes confirming no transactions. Attach to dormant accounts filing (AA02 form).

Bank statements show inflows and outflows. Redact personal details.

Cash books record all entries. Zero balances indicate dormancy.

The director’s minutes document decisions. Note: no trading resolutions passed.

HMRC tax returns confirm nil activity. File CT600 if required.

Retain records for 6 years. Companies House audits randomly.

When Does the Financial Year Trigger a Dormancy Review?

Review status at financial year-end, typically 12 months from incorporation or last accounts date. File within 9 months of the year-end.

Accounting Reference Date (ARD) sets the period. Check Companies House profile.

New companies review after the first ARD. Dormancy applies from day one if inactive.

Extended periods require pro-rata checks. Divide transactions by months.

Deadlines enforce compliance. Late filings incur £150–£1,500 penalties.

Set calendar reminders. Automate via compliance software.

How Does Dormancy Differ from Strike-Off?

Dormancy maintains active registration with simplified filings. Strike-off dissolves the company permanently after 3 months’ notice.

Dormant companies file annually. They remain on the register.

Strike-off uses DS01 form. Directors declare no activity for 3 months prior.

Creditors object within 2 months. Process halts if challenged.

Dormancy suits temporary inactivity. Strike-off ends operations.

Choose based on plans. Reactivate dormant companies easily.

What Are the Filing Requirements for Dormant Companies?

File AA02 dormant accounts and CS01 confirmation statement annually with Companies House. No audit or director’s report needed.

The AA02 form lists a balance sheet with nil figures. Submit online via WebFiling.

CS01 confirms officer details and PSC register. Due within 14 days of the review period.

Fees total £13 for a confirmation statement. Account filing remains free.

Directors sign AA02 digitally. Upload within 9 months of the year-end.

Non-filing triggers compulsory strike-off. Penalties start at £500.

Also explore,

A Simple Guide to Understanding Dormant Company Status and Filing Requirements

Why Your Dormant Company Still Needs to File Accounts with Companies House

What Happens if Your Company Becomes Active Mid-Year?

File full accounts from the activation date. Recalculate year-end to split dormant and active periods if under 12 months.

Notify Companies House of the change. Use the NT01 form for notifications.

Prepare abbreviated accounts for partial periods. Include transaction details.

HMRC requires CT600 adjustments. Pay corporation tax on profits.

Update registers immediately. Record new transactions.

Seek professional help for transitions. Accountants handle splits accurately.

For seamless handling, explore our File Accounts for Dormant Companies service.

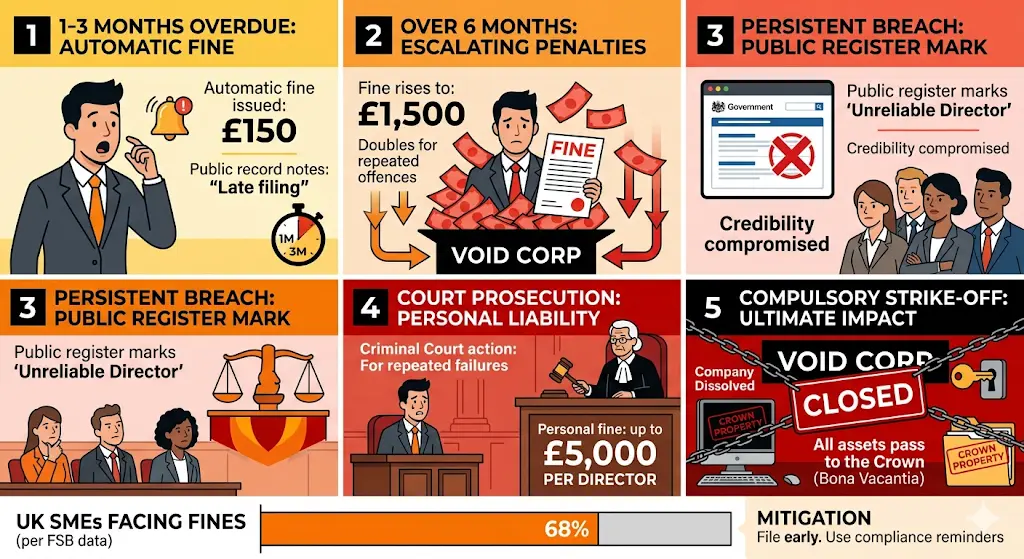

How Do Penalties Affect Non-Compliant Dormant Companies?

Late dormant filings incur £150 for 1–3 months overdue, rising to £1,500 over 6 months. Persistent delays lead to strike-off.

Companies House scales fines by the length of the delay. First offence often warns.

Public register notes penalties. This impacts the director’s credibility.

Court prosecution follows repeated breaches. Fines reach £5,000 per director.

Mitigate by filing early. Use reminders from compliance tools.

68% of UK SMEs face fines yearly for filings, per FSB data.

What Steps Confirm Legal Dormancy Before Filing?

Match transactions against 12 Companies House criteria. Zero disqualifiers confirm status. Submit AA02 within the deadline.

Download the checklist from GOV.UK. Print and annotate.

The director meeting approves the review. Minutes record consensus.

Accountant validates independently. They spot overlooked entries.

File test submission if unsure. WebFiling previews forms.

Maintain audit trail. This supports HMRC enquiries.

Dive deeper into affordable options in our guide: How to Find Affordable Accountants for Your Inactive Company Annual Filing Requirements.

Why Maintain Accurate Dormant Status Records?

Accurate records prevent fines, enable reactivation, and support director duties under the Companies Act 2006. They prove compliance.

Section 386 mandates record-keeping. Dormant firms store minimally.

Reactivation requires back-filings. Gaps delay processes.

Creditors check status publicly. Clean records build trust.

Annual reviews spot trends. Early action avoids activation.

From My Company streamlines this. Our File Accounts for Dormant Companies ensures precision.

Form My Company delivers compliant filings for dormant limited companies. Access expert File Accounts for Dormant Companies to meet deadlines without penalties.

Ready for hands-off management? Read Let Our Experts Manage Your Dormant Company Accounts and Annual Confirmation Statements.

Frequently Asked Questions

What qualifies a UK limited company as dormant for filing accounts?

A UK limited company qualifies as dormant if it conducts no significant accounting transactions, such as share allotments, interest payments, or debt settlements, per Section 1169 of the Companies Act 2006. Companies House requires filing AA02 dormant accounts to confirm this status. From My Company handles File Accounts for Dormant Companies to ensure compliance.

How do I file dormant company accounts with Companies House?

File the AA02 form online via WebFiling within 9 months of your financial year-end, showing nil balances and no transactions. Include a confirmation statement (CS01) annually. From My Company’s File Accounts for Dormant Companies service submits these accurately to avoid penalties.

What are the penalties for late dormant company accounts filing?

Late filings incur £150 for 1-3 months overdue, escalating to £1,500 beyond 6 months, plus potential strike-off. Persistent delays risk director fines up to £5,000. Use File Accounts for Dormant Companies from From My Company for timely submissions.

Can a dormant company still trade or receive payments?

No, dormant companies cannot trade, issue invoices, or handle significant transactions without losing status and requiring full accounts. Minor fees like bank charges under £100 are exempt. From My Company verifies eligibility before File Accounts for Dormant Companies.

Do dormant companies need to file confirmation statements?

Yes, dormant companies file CS01 confirmation statements annually within 14 days of the review period, confirming officers and PSC details. This costs £13 and pairs with AA02 accounts. From My Company’s File Accounts for Dormant Companies bundles both for full compliance.