HMRC enforces tax status and filing for dormant companies, while Companies House records company existence and statutory filings; both require specific dormant accounts and confirmations to keep a company legally inactive.

Failing either triggers penalties, late filing fees, or administrative strike-off.

What is the role of HMRC for inactive business entities?

HMRC monitors tax status, requires dormant-company tax returns where relevant, and issues penalty notices for late or missing filings.

HMRC classifies a company as dormant for corporation tax when it has no income, expenses, or transactions generating tax liability. HMRC still expects companies to register and to confirm dormancy or to file a nil return when asked. HMRC may issue notices that require a company to deliver tax returns, even if nil, and can assess penalties for non-compliance. HMRC also enforces VAT deregistration rules and PAYE finalisation when payroll ceases. For statutory compliance, HMRC’s actions determine whether a company remains exempt from corporation tax liabilities.

What does Companies House do for dormant businesses?

Companies House records company formation, files dormant company accounts, updates the public register, and can strike off companies for non-filing.

Companies House requires an annual confirmation statement and dormant company accounts where applicable. Dormant accounts typically contain a balance sheet and minimal notes and must follow Companies Act accounting formats. Companies House publishes filings on the public register, which creditors and third parties use to verify company status. If a company fails to file accounts or confirmation statements, Companies House may impose penalties, place the company on the public record as non-compliant, or start strike-off procedures that remove the company from the register.

Read our articles, Why Expert Secretarial Support is Essential for Maintaining Your Inactive Company Records and Order Our Fast Track Dormant Account Service for Urgent Business Filing Requirements.

How do HMRC and Companies House’s definitions of “dormant” differ?

HMRC defines dormant for tax purposes by the absence of trading income, while Companies House defines dormant for accounting by the absence of significant accounting transactions.

A company can be dormant for HMRC but show transactions for Companies House if fees or bank charges occur. Conversely, Companies House allows certain minor transactions (e.g., share allotment fees) without losing dormancy for accounts. For tax, HMRC expects reporting if the company receives taxable income or if HMRC issues a return notice. For accounting, Companies House accepts dormant accounts prepared under small-company or micro-entity rules when transaction thresholds are not exceeded.

When must dormant companies file accounts with Companies House?

Dormant companies must file annual dormant-company accounts within nine months of the financial year end for private companies.

Private companies prepare dormant accounts that include a balance sheet signed by a director and appropriate statements. The Companies Act sets filing deadlines: accounts for private dormant companies are due nine months after the year-end. Public dormant companies require 6-month deadlines and fuller disclosures. Directors must maintain records to support dormancy status. Late filing triggers fixed penalties that scale with delay length and company size.

When must dormant companies communicate with HMRC?

Dormant companies must notify HMRC of dormancy and respond to notices to file corporation tax returns or de-register if they cease to trade.

After formation, companies should inform HMRC that they are dormant for corporation tax if there is no trading activity. If HMRC issues a notice to file a return, the company must submit a nil return or justify dormancy. Where payroll existed, directors must apply to close PAYE schemes and handle final RTI submissions. For VAT, companies must deregister once taxable turnover falls below the deregistration threshold or on full cessation. Failure to notify HMRC can cause unexpected tax liabilities and penalties.

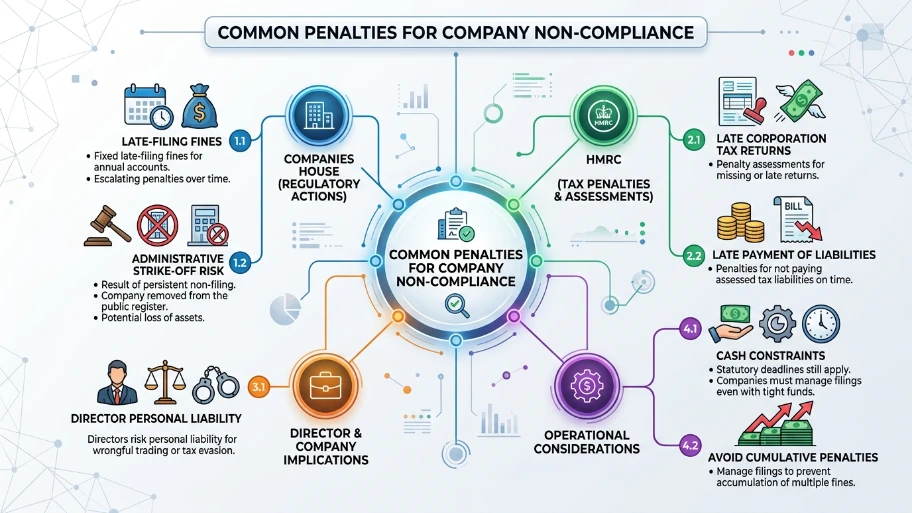

What are the common penalties for non-compliance?

Penalties include fixed late-filing fines from Companies House, HMRC penalty assessments for missing returns, and administrative strike-off risk.

Companies House fines begin with fixed penalties for late accounts and escalate over time. HMRC issues penalties for late corporation tax returns and late payment of assessed liabilities. Persistent non-filing can trigger Companies House strike-off, which removes the company from the register and may lead to loss of assets. Directors risk personal liability where wrongful trading or tax evasion occurs. Companies experiencing cash constraints still face statutory deadlines and must manage filings to avoid cumulative penalties.

How should directors maintain dormancy records?

Directors must keep clear ledgers, bank statements showing inactivity, board minutes confirming inactivity, and copies of filed dormant accounts.

Maintain a single bank account for the company and avoid third-party deposits that could imply trading. Record any nominal transactions, such as bank charges, and explain them in internal records. Hold at least annual board minutes that record the decision to remain dormant and appoint a responsible director for filings. Keep copies of all Companies House and HMRC submissions for at least six years for audit and verification purposes. These records support dormancy in audits or if HMRC or Companies House request evidence.

What steps should directors take if dormancy ends?

Directors must register trading with HMRC, prepare full statutory accounts, and update Companies House filings when the company starts trading.

On resumption of trading, register for corporation tax and, if required, register for VAT and PAYE. Update the accounting system to capture revenue, costs, and tax liabilities. Prepare full accounts in the next statutory period; Companies House will expect standard accounts rather than dormant accounts. Notify clients and suppliers of the change in status and ensure VAT invoices and payroll obligations start from the correct effective date. Failure to update registries can create retroactive liabilities.

How do professional secretarial services help maintain compliance?

Secretarial services validate filings, prepare dormant accounts, submit confirmations, and liaise with HMRC and Companies House to prevent penalties.

A specialist service assigns qualified personnel to verify company records against statutory requirements. They prepare dormant company accounts formatted to Companies House standards and file them on time. They also communicate with HMRC to confirm dormancy status and handle any notices. These services monitor filing deadlines, maintain year-end paperwork, and produce audit-ready documentation. Outsourcing reduces the director’s workload and lowers the risk of late filing penalties.

Explore our File Accounts for Dormant Companies guides,

Understanding the Role of HMRC and Companies House for Inactive Business Entities

How to Keep Your Dormant Company Ready for Potential Future Business Trading

How does the File Accounts for Dormant Companies service streamline compliance?

File Accounts for Dormant Companies prepares and files dormant accounts, ensures correct formats, and submits them to Companies House within statutory deadlines.

The service compiles balance sheets, director signatures, and supporting notes. It verifies company registration details and reconciles bank statements to confirm inactivity. The service submits accounts via Companies House filing channels and provides proof of filing. It saves directors’ time and reduces the chance of fines. Use this service when you need accurate, timely filings and structured evidence to support dormancy status.

Direct management of dormant-company compliance requires attention to both HMRC’s tax rules and Companies House’s filing regime. Directors must keep detailed records, meet specific deadlines, and respond to official notices. Professional secretarial support reduces the risk of penalties and administrative strike-off by delivering correctly formatted dormant accounts and managing HMRC communication. From My Company provides structured filing support to maintain dormancy standing efficiently and reliably.

Frequently Asked Questions

What are dormant company accounts?

Dormant company accounts are simplified statutory accounts filed when a company has had no significant accounting transactions during the financial year. For From My company, the File Accounts for Dormant Companies service helps prepare and submit these accounts in the correct Companies House format.

Do dormant companies still need to file with Companies House?

Yes. A dormant company usually still files annual dormant accounts and a confirmation statement with Companies House. Missing either filing can lead to penalties or strike-off action.

Does HMRC require a dormant company tax return?

HMRC may require a corporation tax return even when a company is dormant, depending on the company’s status and prior notices. If HMRC has opened the company for tax, the company must respond correctly and keep its dormant position updated.

How long does it take to file dormant company accounts?

Filing time depends on whether the company records are complete and whether the accounts are overdue. With the File Accounts for Dormant Companies service, the process is usually faster because the accounts are prepared in the correct format before submission.

What records are needed to file dormant accounts?

Directors usually keep bank statements, company registration details, and records showing no significant transactions. These records help verify dormancy and support accurate filing through From My company’s dormant accounts service.