HMRC and Companies House manage different compliance duties for inactive companies. Companies House requires annual confirmation and dormant accounts filing, while HMRC focuses on corporation tax status and may require notification of dormancy. Both must be updated accurately to avoid penalties and maintain legal company status.

What is the role of Companies House for inactive business entities?

Companies House maintains the legal record of all UK companies, including dormant entities. It requires the submission of annual confirmation statements and dormant accounts to confirm that no significant financial activity has taken place during the financial year.

Companies House acts as the official registrar of UK companies. It ensures that every registered entity maintains an accurate public record. Even when a company is inactive, it remains on the register and must comply with statutory filing obligations.

Dormant companies must file two key documents annually. These include a confirmation statement and dormant accounts. The confirmation statement verifies company details such as directors, shareholders, and registered office. Dormant accounts confirm that no accounting transactions occurred.

Failure to submit these documents results in automatic penalties. Late filing penalties start at £150 and can reach £1,500 depending on delay length. Continued non-compliance can lead to the company being struck off. Companies House does not assess tax obligations. Its function remains strictly administrative and record-based. However, its data feeds into other regulatory systems, making accuracy critical.

How does HMRC regulate inactive companies?

HMRC oversees the tax status of dormant companies and determines whether corporation tax filings are required. A company must notify HMRC when it becomes dormant, after which HMRC typically suspends the requirement to file corporation tax returns unless activity resumes.

HMRC defines dormancy differently from Companies House. A company is dormant for corporation tax purposes when it has no taxable income or activity. This includes trading, investments, or significant financial transactions.

Directors must inform HMRC when a company becomes inactive. This is usually done through the company’s corporation tax account or by written notification. Once accepted, HMRC may mark the company as dormant.

HMRC stops issuing notices to deliver corporation tax returns after dormancy confirmation. However, if any transaction occurs, such as bank interest exceeding thresholds or trading income, the company becomes active again.

In some cases, HMRC still requests returns even for dormant companies. This happens when records are incomplete or activity is suspected. Directors must respond promptly to avoid compliance issues.

Why must dormant companies comply with both authorities?

Dormant companies must comply with both HMRC and Companies House because each authority governs separate legal and financial obligations. Companies House ensures accurate corporate records, while HMRC manages tax classification and compliance, requiring dual reporting even without business activity.

These two authorities operate independently. Companies House focuses on transparency and public records. HMRC focuses on taxation and financial compliance. A company can be dormant with Companies House but still active with HMRC. This occurs when minor transactions trigger tax obligations. For example, receiving £200 in bank interest may not affect Companies House status but can impact HMRC classification.

Compliance failures with either authority lead to different consequences. Companies House enforces financial penalties and strike-off procedures. HMRC imposes fines, interest, and investigations. Directors must manage both obligations simultaneously. This includes tracking financial inactivity thresholds and ensuring timely submissions to both bodies.

What qualifies a company as dormant in the UK?

A UK company is considered dormant when it has no significant accounting transactions during a financial year. This excludes specific allowable transactions such as filing fees, penalties, and initial share capital payments that do not affect its dormant classification.

Dormancy depends on transaction activity. Companies House defines significant accounting transactions as those that must be entered into accounting records. If none occur, the company qualifies as dormant.

Examples of permitted transactions include:

- Payment of Companies House filing fees

- Civil penalties for late filing

- Initial share subscription during incorporation

Any other financial movement, such as trading income, employee salaries, or asset purchases, breaks dormancy. HMRC uses a stricter definition. It evaluates whether taxable income exists. Even small financial gains can trigger an active status for tax purposes. Directors must maintain clear records. This ensures accurate classification across both regulatory bodies.

What filings are required for dormant companies?

Dormant companies must file annual dormant accounts with Companies House and submit a confirmation statement to verify company details. They must also notify HMRC of dormancy and only submit corporation tax returns if specifically requested.

The filing process involves multiple steps across different systems. Each requirement has specific deadlines and formats.

Key filings include:

- Submit dormant accounts within 9 months of the financial year-end

- File a confirmation statement at least once every 12 months

- Notify HMRC when the company becomes dormant

- Respond to HMRC notices if issued

Dormant accounts are simpler than active company accounts. They typically include a balance sheet and minimal notes. The confirmation statement ensures that company data remains accurate. This includes director details, PSC (Person with Significant Control), and registered address.

Businesses often use professional services to manage these filings. A structured approach reduces the risk of missed deadlines and penalties. For accurate and compliant submissions, many directors choose to file accounts for dormant companies efficiently using specialist support that aligns with UK filing frameworks.

What happens if a dormant company fails to comply?

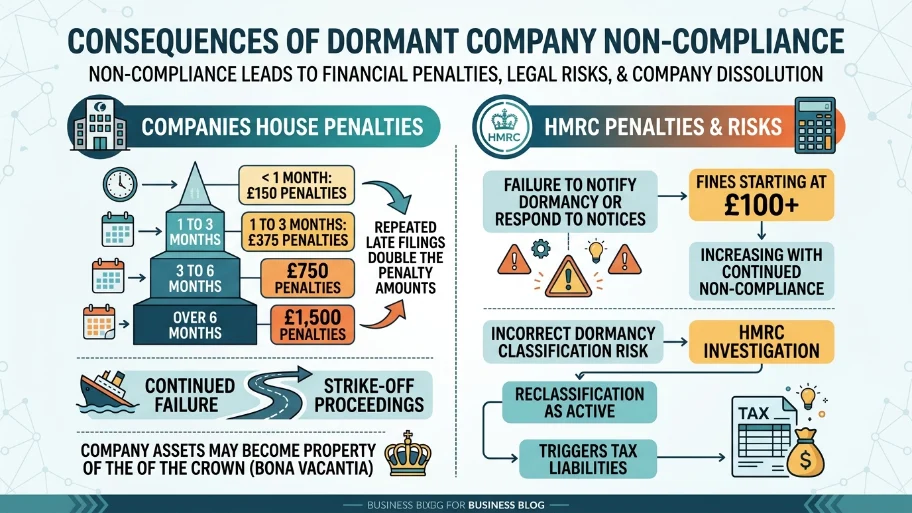

Non-compliance leads to financial penalties, legal risks, and possible company dissolution. Companies House imposes late filing fines, while HMRC may issue tax penalties or reopen tax obligations if dormancy status is unclear or incorrectly reported.

Companies House applies a tiered penalty system. Filing delays of:

- Up to 1 month results in £150 penalties

- 1 to 3 months result in £375 penalties

- 3 to 6 months result in £750 penalties

- Over 6 months results in £1,500 penalties

Repeated late filings double the penalty amounts. Continued failure leads to strike-off proceedings. Once struck off, company assets may become property of the Crown.

HMRC penalties vary based on the issue. Failure to notify dormancy or respond to notices can result in fines starting at £100 and increasing with continued non-compliance. Incorrect dormancy classification also creates risks. HMRC may investigate and reclassify the company as active, triggering tax liabilities.

How do Companies House and HMRC definitions differ?

Companies House defines dormancy based on accounting transactions, while HMRC defines it based on taxable activity. A company may meet one definition but not the other, requiring careful monitoring of both financial and tax-related activities.

The distinction creates compliance complexity. Directors often assume that dormancy applies universally, which is incorrect. Companies House focuses on accounting entries. If no significant entries exist, the company qualifies as dormant.

HMRC evaluates income and tax exposure. Even minimal financial activity can trigger an active status.

For example, three common scenarios highlight the difference:

- Receiving bank interest affects HMRC but not Companies House

- Holding investments affects HMRC classification

- Paying only filing fees maintains dormancy for both

Understanding these differences ensures accurate reporting and prevents regulatory conflicts.

Explore our file accounts for dormant companies guides,

How to Keep Your Dormant Company Ready for Potential Future Business Trading

Why Late Filing Penalties Apply Even if Your Company Has Never Traded

How can dormant companies maintain compliance efficiently?

Dormant companies maintain compliance by tracking deadlines, submitting accurate filings, and aligning reporting across both authorities. Using structured processes or professional services reduces errors and ensures consistent compliance with UK regulatory requirements.

Efficiency depends on process control. Directors must maintain a compliance calendar that includes all deadlines.

Key actions include:

- Track filing deadlines for accounts and confirmation statements

- Maintain zero-transaction financial records

- Monitor HMRC communication regularly

- Validate company details before submission

Automation tools and professional services improve accuracy. They reduce manual errors and ensure timely submissions.

Many businesses rely on structured solutions to file accounts for dormant companies with precision and regulatory alignment. These services handle documentation, submission, and compliance tracking.

For a deeper understanding of maintaining records, see this guide on why expert secretarial support improves dormant company compliance. When urgent filings arise, businesses often evaluate options like fast-track dormant account filing services for immediate compliance needs.

HMRC and Companies House serve distinct but equally critical roles in managing inactive business entities. Companies House ensures accurate public records through confirmation statements and dormant accounts, while HMRC governs tax classification and reporting obligations. Misalignment between these authorities creates compliance risks, including penalties and legal exposure.

Dormant companies must actively manage their status despite having no trading activity. Accurate filings, timely submissions, and clear financial records remain essential. From My Company delivers structured solutions that simplify dormant company compliance, ensuring alignment with both Companies House and HMRC requirements.

Frequently Asked Questions

What are dormant company accounts?

Dormant company accounts are simplified annual accounts filed when a company has had no significant accounting transactions during the financial year. From My company prepares and submits the File Accounts for Dormant Companies to keep this filing accurate and compliant.

Do dormant companies still file with Companies House?

Yes. Dormant companies still file dormant accounts and an annual confirmation statement with Companies House. These filings confirm that the company remains registered and that its details are current.

Does HMRC still deal with dormant companies?

Yes. HMRC still tracks dormant companies for corporation tax purposes. A company must tell HMRC when it becomes dormant, and HMRC may stop issuing tax return notices if no taxable activity exists.

What counts as a dormant company in the UK?

A company is dormant when it has no significant accounting transactions in a financial year. Small permitted items, such as filing fees or incorporation share capital, do not usually stop dormancy.

What happens if dormant company accounts are filed late?

Late filing can trigger penalties from Companies House and create compliance issues with HMRC. From My company helps businesses file Accounts for Dormant Companies on time to reduce the risk of fines and strike-off action.