UK small businesses and sole traders choose from four main VAT schemes: the standard VAT scheme, the Flat Rate Scheme (FRS), the Cash Accounting Scheme, and the Margin Scheme. Each targets specific turnover levels and business types to simplify compliance and reduce costs.

From My Company guides businesses through these options during VAT Registration Assistance.

What Is the Standard VAT Scheme?

The standard VAT scheme requires businesses to charge 20% VAT on sales, reclaim VAT on purchases, and file returns quarterly if turnover exceeds £90,000 annually.

Businesses register for VAT under this scheme when taxable turnover hits £90,000 in 12 months. They add VAT to sales invoices. Customers pay this VAT. Firms reclaim input VAT from suppliers.

HMRC mandates quarterly returns. Submit by the end of the month following each quarter. Pay VAT owed within 30 days of errors or adjustments.

This scheme suits businesses with high reclaimable expenses. Retailers and manufacturers reclaim VAT on stock and equipment. Turnover limits apply strictly.

Who Qualifies for the Flat Rate Scheme?

Sole traders and small businesses with VAT-taxable turnover under £150,000 qualify for the Flat Rate Scheme. They apply a fixed percentage to VAT-inclusive turnover and pay HMRC without reclaiming input VAT.

HMRC approves FRS for eligible firms. Turnover is calculated over four quarters. Exclude VAT-exempt supplies.

Firms pick rates from 1% to 14.5%. Retailers use 7.5%. Consultants apply 14.5%. Limited-cost traders select 16.5%.

Pay flat rate VAT monthly or quarterly. No input VAT claims simplify records. Save time on bookkeeping.

New businesses test FRS for the first year. Switch if unsuitable later. Deregister if turnover drops below £150,000.

How Does the Cash Accounting Scheme Work?

Businesses with turnover below £1.35 million use the Cash Accounting Scheme. They account for VAT when payments are received or made, not when invoices are issued.

Apply via VAT return. HMRC grants permission automatically for qualifying firms.

Record output VAT on customer payments. Claim input VAT on supplier payments. Matches cash flow directly.

Suits service providers with delayed payments. Freelancers and contractors benefit most.

File returns quarterly. Adjust for bad debts separately. No complex accruals needed.

Switch to the standard scheme if turnover exceeds £1.35 million. Monitor thresholds yearly.

When Should You Use the Margin Scheme?

Retailers of second-hand goods, antiques, or artwork use the Margin Scheme. Charge VAT only on profit margin, not the full selling price.

Two versions exist: the standard Margin Scheme and global accounting. Standard applies to individual items. Global aggregates purchases and sales.

Calculate the margin as the selling price minus the purchase price. Apply 20% VAT to this difference. Keep purchase invoices.

Antique dealers verify item history. Motor dealers track second-hand vehicles.

Register separately if needed. HMRC inspects records during audits.

Combine with other schemes cautiously. Avoid double-counting VAT.

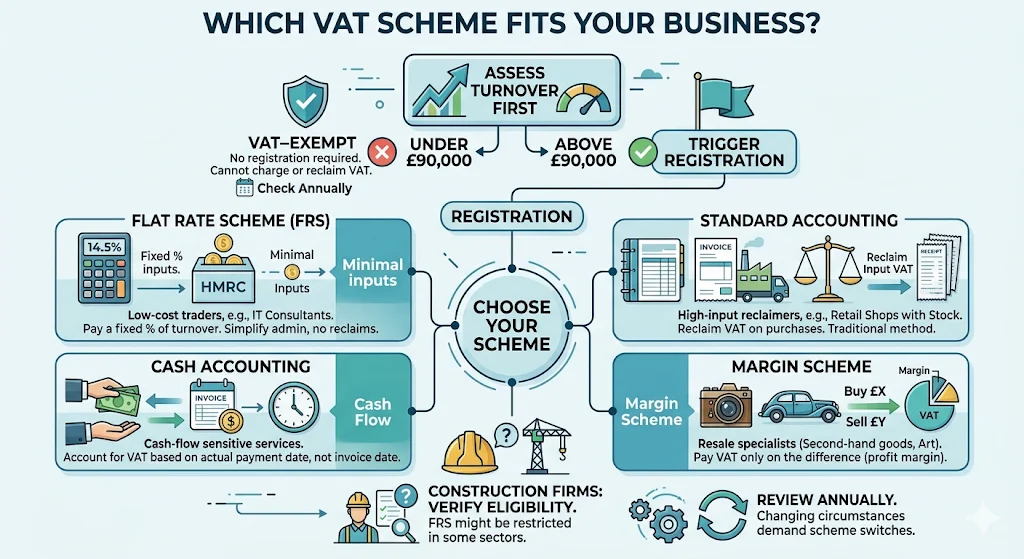

Which VAT Scheme Fits Your Business Type?

Match schemes to business models: standard for high-input reclaimers, FRS for low-cost traders, Cash Accounting for cash-flow sensitive services, and Margin for resale specialists.

Assess turnover first. Under £90,000 stays VAT-exempt. Above triggers registration.

Services like IT consultants pick FRS at 14.5%. Save on admin despite no reclaims.

Retail shops with stock choose the standard. Reclaim VAT on inventory purchases.

Construction firms verify eligibility. Some sectors restrict FRS.

Review annually. Changing circumstances demand scheme switches.

What Are the Key Differences Between These Schemes?

Standard charges full VAT with reclaims; FRS uses flat rates without; Cash Accounting ties to payments; Margin taxes profits only on specific goods.

| Scheme | Turnover Limit | VAT Calculation | Input VAT |

|---|---|---|---|

| Standard | None post-registration | On sales value | Reclaimable |

| Flat Rate | £150,000 | Fixed % of turnover | None |

| Cash Accounting | £1.35 million | On payments | On payments |

| Margin | Varies by goods | On profit margin | None |

Choose based on expenses. High costs favor standard. Low overheads suit FRS.

Cash Accounting eases seasonal businesses. Margin protects resale markups.

How Do You Switch Between VAT Schemes?

Notify HMRC via VAT return or form VAT615. Approval takes effect next quarter. Provide updated turnover figures.

Submit the request before the period ends. A standard switch requires an accrual accounting setup.

FRS exit demands input VAT tracking. Restart reclaims immediately.

Cash to standard needs invoice-based records. Train staff on changes.

Margin scheme changes need stock revaluation. Document all transitions.

From My Company handles transitions in VAT Registration Assistance.

What Are the Compliance Rules for Each Scheme?

File quarterly returns on time. Keep records for six years. Use MTD-compliant software for digital submissions.

The standard scheme demands detailed ledgers. Separate VAT accounts.

FRS requires turnover verification. Retain invoices without reclaim claims.

Cash Accounting logs payment dates. Reconcile bank statements.

Margin scheme mandates purchase proofs. Calculate margins accurately.

Penalties hit late filers. Read Why Late VAT Registration Penalties are Not Worth the Risk for Startups for details.

How Do Turnover Thresholds Affect Scheme Choice?

Thresholds dictate options: £90,000 triggers registration, £150,000 caps FRS, £1.35 million limits Cash Accounting.

Monitor rolling 12-month turnover. Forecast growth quarterly.

Sole traders scale faster under FRS. Switch at £150,000.

Exceeding limits forces the standard scheme. Plan reclaims.

Dormant periods reset clocks. Recalculate precisely.

What Records Must Small Businesses Maintain?

Store invoices, receipts, and bank statements for six years. Use digital tools for MTD compliance.

Input VAT proofs for the standard scheme. Turnover summaries for FRS.

Payment ledgers for Cash Accounting. Margin calculations for resale.

HMRC audits unannounced. Digital records speed verifications.

Backup data securely. Shred after six years.

Why Compare Schemes Before Registering?

Schemes cut tax bills by 10-20% for matches. Mismatched choices raise costs and audits.

Run projections. FRS saves £2,000 yearly for £100,000 turnover traders.

Standard reclaims £15,000 on £100,000 purchases.

Test scenarios. Consult experts early.

Decide with Let Our Experts Handle Your Entire VAT Registration Process from Start

to Finish for seamless setup.

Also explore,

5 Common Mistakes New Business Owners Make Before Registering for UK VAT

How VAT Registration Works for Businesses Selling Goods and Services Online

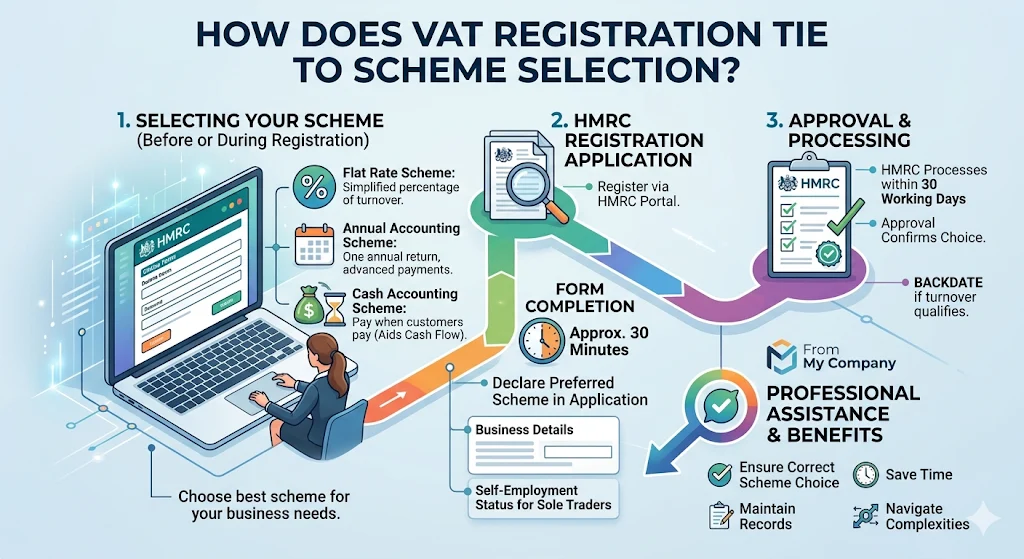

How Does VAT Registration Tie to Scheme Selection?

Register via the HMRC portal. Declare the preferred scheme during the application. Approval confirms the choice.

The online form takes 30 minutes. Provide business details.

HMRC processes in 30 days. Backdate if turnover qualifies.

From My Company streamlines this in VAT Registration Assistance.

Sole traders list self-employment status.

What Penalties Arise from Wrong Scheme Use?

HMRC fines 30% of unpaid VAT for errors. Late switches add interest at 2.75% annually.

Audits recover overclaimed amounts. FRS misuse blocks future use.

Cash Accounting breaches demand repayments.

An accurate choice prevents 70% of disputes.

Small businesses and sole traders select VAT schemes based on turnover, costs, and operations. Standard suits reclaim-heavy firms. FRS simplifies low-expense models. Cash Accounting aligns with payments. Margin protects resale profits.

From My Company delivers VAT Registration Assistance to match schemes precisely. Register correctly. Comply fully. Grow without tax hurdles.

Frequently Asked Questions

What is VAT registration assistance?

VAT registration assistance helps UK small businesses and sole traders complete HMRC’s online VAT registration process accurately. From My Company provides VAT Registration Assistance to verify eligibility, select schemes like Flat Rate or Cash Accounting, and submit forms within 30 days. This ensures compliance from the start without penalties.

Who needs VAT registration assistance in the UK?

Businesses with a taxable turnover over £90,000 in 12 months require VAT registration. Sole traders, startups, and SMEs benefit from VAT Registration Assistance to navigate thresholds and schemes correctly. From My Company assists with mandatory filings to avoid late registration fines up to 30% of VAT due.

How long does VAT registration take with assistance?

Standard HMRC processing takes 10-30 working days after submission. From My Company’s VAT Registration Assistance speeds setup by preparing documents and choosing optimal schemes like the Margin Scheme upfront. Approval allows immediate VAT charging and reclaiming.

What documents are needed for VAT registration assistance?

Key documents include business details, UTR number, ID proofs, and turnover projections. VAT Registration Assistance from My Company reviews these for accuracy, ensuring MTD-compliant submissions. Submit via Government Gateway for the fastest approval.

Can VAT registration assistance help choose a scheme?

Yes, assistance evaluates turnover and business type to recommend schemes like Standard, Flat Rate, or Cash Accounting. From My Company tailors VAT Registration Assistance to minimise tax liability while meeting HMRC rules. Switch schemes later via VAT returns if needed.