No, you do not always need to operate PAYE if you are the sole director of your UK company and do not employ anyone else. However, if you pay yourself a salary, HMRC requires you to register for PAYE to handle income tax and National Insurance deductions properly.

This setup raises common questions for new business owners navigating UK employment rules. As the only director, your company structure often falls under a private limited company (Ltd), where you might draw income through dividends or salary. Understanding PAYE Pay As You Earn is crucial because it governs how employers deduct taxes from earnings. Even without staff, sole directors must assess their personal remuneration against HMRC guidelines to stay compliant and avoid penalties.

Understanding PAYE and Its Role for UK Companies

PAYE serves as HMRC’s system for collecting income tax and National Insurance contributions (NICs) directly from wages, salaries, and certain benefits before employees receive their pay. For UK companies, registration typically occurs when hiring staff, but sole directors face unique considerations. HMRC defines employers broadly, including directors who process their own salary payments.

If your company operates as a director-only entity, dividends alone do not trigger PAYE since they count as post-tax distributions rather than employment income. However, opting for a salary even a minimal one to qualify for state benefits like maternity pay or to optimize tax efficiency requires PAYE setup. This involves obtaining a PAYE reference number, maintaining payroll records, and submitting Real Time Information (RTI) returns monthly or quarterly.

Form My Company specializes in simplifying these processes through their PAYE Registration Assistance service, ensuring director-only businesses meet HMRC standards without hassle. Semantic keywords like “PAYE obligations for single shareholders” highlight how even micro-entities must comply if salaries feature in their remuneration strategy.

When Does a Sole Director Trigger PAYE Requirements?

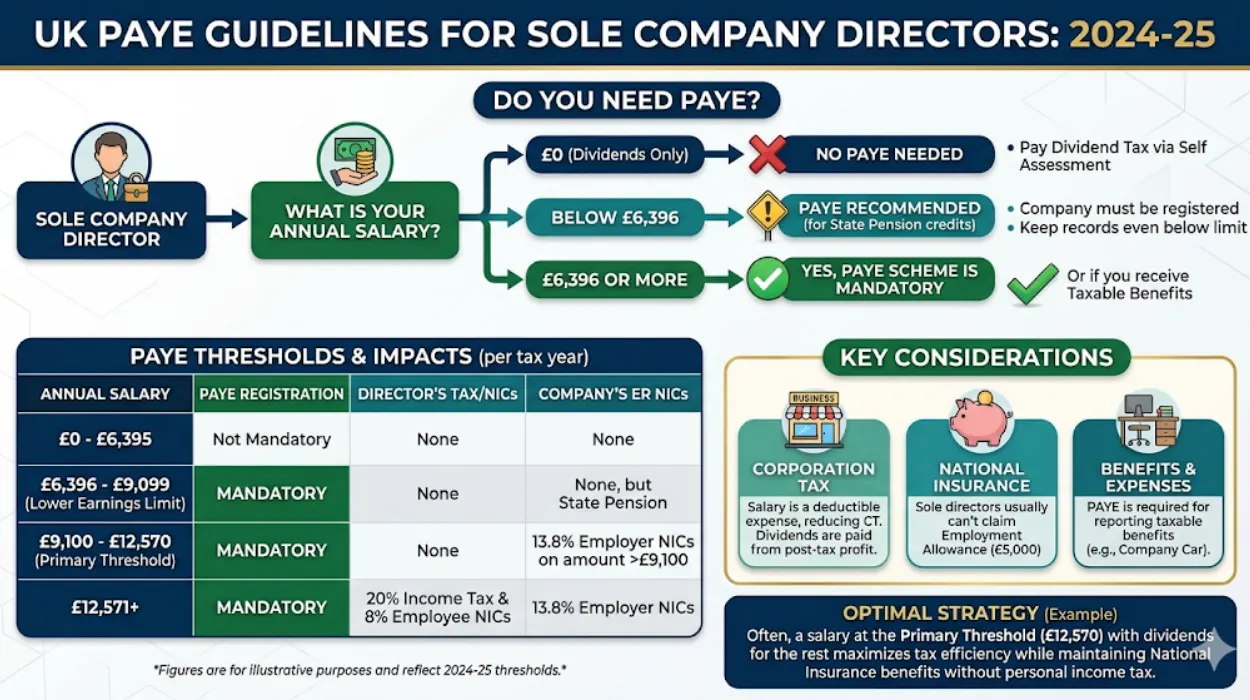

Sole directors often wonder if their status exempts them from payroll bureaucracy. HMRC clarifies that PAYE applies whenever the company acts as an employer to itself via director’s salary. For instance, setting a salary above the personal allowance threshold currently £12,570 for 2025/26 necessitates deductions.

Consider a typical scenario: You form a UK Ltd company and decide on a £8,000 annual salary to preserve corporation tax relief while building National Insurance credits. Without PAYE, HMRC views this as undeclared employment income, risking fines up to £3,000 per tax year for non-compliance. Registration must happen before your first payroll run, ideally within the same tax month or by month’s end.

Directors drawing no salary sidestep this entirely, relying solely on dividends taxed via self-assessment. Yet, many choose modest salaries for tax advantages salaries reduce taxable profits before corporation tax (19% for profits under £50,000), while dividends face additional dividend tax rates starting at 8.75%. HMRC’s Employment Status Indicator tool confirms your director role as employed for PAYE purposes, emphasizing structured payroll even for one person.

Legal Thresholds and Exemptions for Director-Only Companies

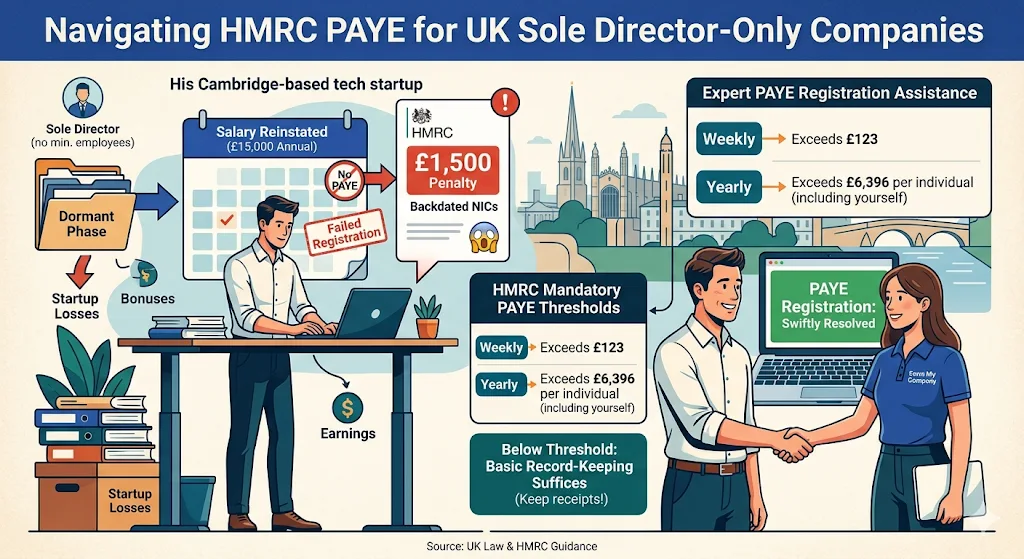

UK law sets clear PAYE thresholds, but sole directors benefit from no minimum employee count. HMRC mandates registration if you anticipate paying salaries, bonuses, or benefits exceeding £123 weekly (£6,396 annually) per individual, including yourself. Below this, basic record-keeping suffices, though salary payments still demand PAYE if they qualify as earnings.

Exemptions rarely apply to active directors. Dormant companies or those paying only expenses avoid it, but resuming salary triggers retrospective registration up to two years prior. A case-study-style example illustrates: A Cambridge-based tech director paused salary during startup losses, then reinstated £15,000 annually. Failing PAYE registration led to a £1,500 HMRC penalty plus backdated NICs; prompt PAYE Registration Assistance from experts like Form My Company resolved it swiftly.

Entity-based compliance underscores this: PAYE schemes integrate with HMRC’s Government Gateway, requiring an Employer Payment Summary for NIC reconciliations. Sole directors must also consider auto-enrolment pensions if earnings hit £520 monthly, layering on duties despite no staff.

Steps to Register for PAYE as a Single Director

Registering PAYE demands precision to align with HMRC timelines. Start online via the Government Gateway portal, providing your Companies House number, UTR, and payroll details. Approval yields a PAYE reference (e.g., 123/A45678) within 5-10 days, followed by starter checklists for new “employees” yes, including yourself.

Next, select payroll software or spreadsheets compliant with RTI submissions. For director-only setups, tools like HMRC’s Basic PAYE Tools suit low-volume needs, calculating deductions automatically. Run payroll monthly, reporting via FPS (Full Payment Submission) by the payment date.

Penalties loom for delays: Late registration incurs £100 fixed fines, escalating to daily charges. Proactive steps prevent this many sole directors link registration to company formation for seamless setup.

Benefits and Tax Strategies Involving PAYE for Sole Directors

Embracing PAYE unlocks strategic perks beyond compliance. Salaries optimize tax brackets; for example, drawing £12,570 salary incurs zero income tax or employee NICs, sheltering dividends from higher bands. This “salary sacrifice” approach minimizes overall liability while qualifying for benefits like the state pension.

Moreover, PAYE builds employment history for loans or visas. In a volatile economy, director-only firms use it to demonstrate stability to banks. To deepen payroll savvy, explore how to choose the right payroll software for your UK startup for scalable tools fitting growth.

Structured remuneration via PAYE also aids cash flow forecasting, as NICs (13.8% employer rate) become predictable expenses deductible from profits.

Common Misconceptions About PAYE for Solo Directors

Many assume sole directors escape PAYE entirely, but HMRC treats director service contracts as employment. Another myth: Dividends fully replace salary needs no, they lack NIC credits essential for benefits. IR35 rules further complicate contractors posing as directors, mandating PAYE for deemed employment.

A practical insight: A London sole director ignored PAYE for a £10,000 “consulting fee” to himself, facing reclassification and £2,000 in arrears. Proper setup via professional services averts such pitfalls.

Navigating Compliance Challenges and Long-Term Planning

Sole directors juggle multiple HMRC obligations PAYE dovetails with VAT, corporation tax, and self-assessment. Annual P60s and P11D forms detail your earnings for transparency. As businesses scale, PAYE records facilitate hiring.

For expedited compliance, get your employer PAYE reference number fast with our team at Form My Company, turning bureaucracy into efficiency.

Mastering PAYE as a sole director ensures fiscal health and regulatory peace. Form My Company delivers professional PAYE Registration Assistance, empowering UK entrepreneurs to focus on growth, not paperwork. Consult HMRC updates regularly, as rules evolve your compliant foundation supports enduring success.

What is PAYE registration for a UK company?

PAYE registration is HMRC’s process for employers to deduct income tax and National Insurance from salaries before paying employees. Sole directors paying themselves a salary must register to comply with UK payroll rules. Form My Company offers PAYE Registration Assistance to handle this setup efficiently.

Do sole directors need PAYE registration in the UK?

Yes, sole directors need PAYE registration if they draw a salary from their company, as it counts as employment income under HMRC guidelines. Dividends alone do not trigger it, but salaries require RTI submissions and deductions. PAYE Registration Assistance from Form My Company simplifies compliance for director-only businesses.

How long does PAYE registration take for UK businesses?

PAYE registration typically takes 5-10 working days via HMRC’s online portal after submitting company details. Delays occur with incomplete applications, so prepare your UTR and Companies House number in advance. Form My Company’s PAYE Registration Assistance ensures fast processing and accurate setup.

What documents are needed for PAYE registration UK?

Key documents include your Unique Taxpayer Reference (UTR), Companies House registration number, and bank details for payments. HMRC also requires payroll start dates and employee counts, even for sole directors. Expert PAYE Registration Assistance from Form My Company verifies everything for seamless approval.

What happens if you don’t register for PAYE on time UK?

Late PAYE registration incurs HMRC penalties starting at £100, plus daily fines and backdated NICs up to £3,000 per year. Non-compliance risks audits and interest charges on unpaid tax. Form My Company’s PAYE Registration Assistance prevents these issues with timely, compliant registration.