Djibouti entrepreneurs can open a UK company by registering with Companies House, verifying director identity, and securing a compliant UK business bank account. Compliance requires accurate reporting, AML verification, and ongoing filing obligations to maintain legal and financial standing in the UK.

Why do Djibouti entrepreneurs choose the UK for company formation?

Djibouti entrepreneurs choose the UK because it offers fast company registration, global banking access, and a trusted legal framework. The UK enables non-residents to operate internationally with low setup costs, transparent tax structures, and strong financial credibility.

The UK ranks among the top 10 easiest countries for business formation. Company registration typically completes within 24 to 48 hours. This speed appeals to founders seeking rapid market entry. The legal system supports non-residents. Directors do not require UK citizenship or residency. This allows Djibouti-based entrepreneurs to manage operations remotely while maintaining full ownership.

UK companies gain access to global payment networks. These include SEPA transfers, SWIFT payments, and multi-currency accounts. This infrastructure simplifies international trade. The UK also maintains strict compliance standards. These standards increase trust among suppliers, investors, and financial institutions. A verified UK entity signals operational legitimacy.

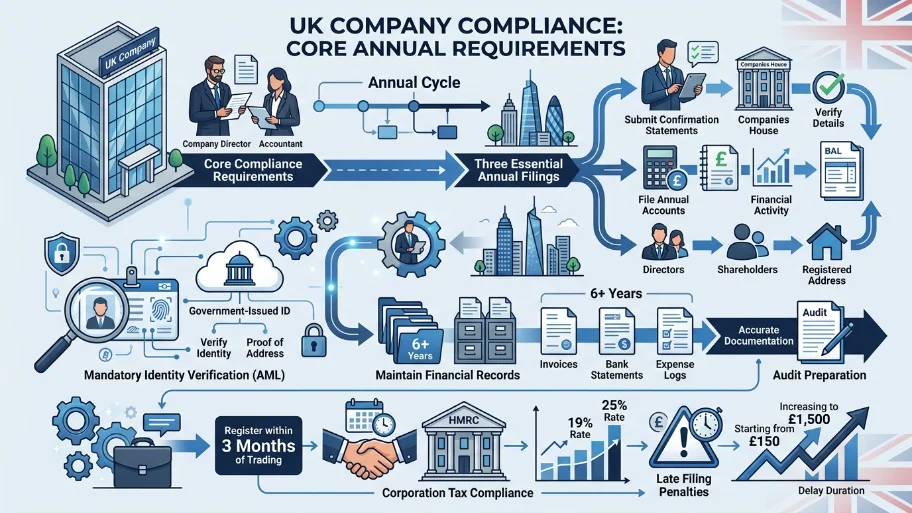

What are the core compliance requirements for UK companies?

UK companies must comply with Companies House filings, maintain accurate financial records, and meet anti-money laundering (AML) obligations. Directors must verify identity, submit annual accounts, and confirm company details annually to remain legally active.

Every UK company must file three essential records annually:

- Submit confirmation statements verifying company details

- File annual accounts showing financial activity

- Report changes in directors, shareholders, or registered address

Identity verification is mandatory under UK AML regulations. Directors must provide government-issued ID and proof of address. Verification systems cross-check identity against official databases. Companies must maintain accounting records for at least six years. These records include invoices, bank statements, and expense logs. Accurate documentation ensures compliance during audits.

Tax compliance involves registering for Corporation Tax within three months of trading. The current UK Corporation Tax rate ranges from 19% to 25%, depending on profit levels. Failure to comply leads to penalties. Late filings incur fines starting from £150 and increasing to £1,500 based on the delay duration.

How can Djibouti entrepreneurs open a UK business bank account?

Djibouti entrepreneurs can open a UK business bank account by completing identity verification, submitting company documents, and selecting a bank that supports non-residents. Digital banks and EMI platforms provide faster onboarding compared to traditional UK banks.

Traditional UK banks often require physical presence. This creates barriers for non-residents. Digital banking platforms remove this limitation through remote onboarding.

Three common banking options include:

- Digital banks such as Wise Business and Revolut Business

- Electronic Money Institutions (EMIs) offering multi-currency accounts

- Fintech platforms providing API-based payment solutions

Banks verify three core elements:

- Confirm director’s identity using passport and biometric checks

- Validate company registration through Companies House records

- Assess business activity for AML compliance

Approval timelines vary. Digital banks process applications within 2 to 5 days. Traditional banks may take 2 to 6 weeks. Entrepreneurs improve approval rates by providing clear business descriptions, transaction forecasts, and proof of operational intent.

What banking challenges do Djibouti residents face?

Djibouti residents face challenges such as strict AML checks, limited access to traditional UK banks, and enhanced due diligence requirements. Financial institutions classify non-resident applicants as higher risk, which increases documentation requirements and onboarding time.

Banks apply enhanced due diligence for applicants from jurisdictions with limited financial transparency. This includes deeper identity verification and source-of-funds validation.

Common barriers include:

- Limited acceptance by high-street UK banks

- Requests for UK-based proof of operations

- Additional verification of business activities

Financial institutions often require detailed documentation. This includes business plans, supplier contracts, and projected revenue streams. Transaction monitoring also increases. Banks track international payments to detect unusual patterns. Suspicious activity triggers account reviews or restrictions. These challenges do not prevent account approval. They extend the onboarding process and increase compliance scrutiny.

How does AML and KYC verification work for non-residents?

AML and KYC verification for non-residents involves identity authentication, source-of-funds validation, and risk assessment. UK financial institutions use automated systems and manual reviews to ensure compliance with international financial regulations and prevent illicit activities.

Verification begins with identity authentication. Directors submit passports and proof of address. Systems validate documents using optical recognition and database checks. The next step involves source-of-funds verification. Applicants must explain how business capital was obtained. Acceptable sources include savings, business revenue, or investment funds.

Risk profiling follows. Banks assess factors such as:

- Country of residence

- Industry type

- Transaction volume

Higher-risk profiles trigger enhanced due diligence. This includes additional document requests and manual compliance reviews. Verification systems operate under frameworks such as the UK Money Laundering Regulations 2017. These regulations align with Financial Action Task Force (FATF) standards.

What documents are required for UK company banking?

UK company banking requires incorporation documents, director identification, proof of address, and business activity details. Banks use these documents to verify identity, validate company legitimacy, and assess financial risk before approving accounts.

Core documents include:

- Certificate of Incorporation issued by Companies House

- Memorandum and Articles of Association

- Passport copies of directors and shareholders

- Proof of residential address dated within three months

Banks also require business-related information. This includes:

- Description of products or services

- Expected monthly transaction volume

- Countries involved in trading activities

Providing accurate documentation speeds approval. Missing or inconsistent information leads to delays or rejections. Entrepreneurs benefit from structured preparation. Organising documents in advance reduces verification friction.

How can Djibouti entrepreneurs ensure compliance after company formation?

Djibouti entrepreneurs ensure compliance by maintaining accurate records, meeting filing deadlines, and monitoring financial transactions. Ongoing compliance includes tax reporting, director updates, and adherence to UK regulatory standards.

Compliance extends beyond company registration. It requires continuous monitoring of legal obligations.

Three critical compliance actions include:

- File annual accounts within 9 months of the financial year-end

- Submit confirmation statements every 12 months

- Update Companies House with structural changes immediately

Accounting systems play a key role. Digital tools automate transaction tracking and reporting. This reduces manual errors and improves accuracy. Tax compliance requires the timely submission of Corporation Tax returns. Companies must also track VAT obligations if taxable turnover exceeds £90,000. Regulatory compliance strengthens business credibility. It ensures uninterrupted banking operations and avoids financial penalties.

What is the step-by-step process to start from Djibouti?

Djibouti entrepreneurs can start by registering a UK company, verifying identity, selecting a banking provider, and completing compliance checks. The process includes document submission, approval verification, and ongoing regulatory adherence.

The process follows a structured sequence:

- Register the company with Companies House using the director’s details

- Verify identity through AML-compliant systems

- Choose a banking provider supporting non-residents

- Submit the required documents for account approval

- Activate your account and begin financial operations

Each step requires accurate data submission. Errors during registration or verification delay the process. Entrepreneurs streamline setup by using dedicated services such as the Djibouti company formation service, which integrates registration, compliance, and banking support into one process.

How does banking integration impact business operations?

Banking integration impacts business operations by enabling international payments, automating financial tracking, and supporting multi-currency transactions. Efficient banking systems improve cash flow visibility and reduce operational friction for global businesses.

Integrated banking systems connect with accounting platforms. This enables real-time tracking of income and expenses. Multi-currency accounts reduce conversion costs. Businesses can hold, send, and receive funds in GBP, USD, and EUR without frequent exchange fees.

Payment automation improves efficiency. Businesses can process invoices, payroll, and supplier payments without manual intervention. Financial visibility improves decision-making. Entrepreneurs track performance metrics such as cash flow, profit margins, and transaction volume. Reliable banking infrastructure supports scalability. It allows businesses to expand into new markets without financial limitations.

Explore our Comoros,

How Comoros Entrepreneurs Can Start and Manage a UK Company Internationally

Where can Djibouti entrepreneurs get structured support?

Djibouti entrepreneurs can access structured support through specialised service providers offering company formation, banking setup, and compliance management. These services streamline processes, reduce errors, and ensure regulatory alignment from the start.

Professional services reduce complexity. They handle registration, document preparation, and compliance checks in one workflow. From My Company provides integrated solutions tailored for non-residents. These services include company formation, identity verification, and banking facilitation.

Entrepreneurs benefit from guided onboarding. This reduces rejection risks and improves approval timelines. For a deeper understanding of compliance and banking workflows, review this guide on how Djibouti residents can navigate banking and compliance when opening a UK company. Those ready to proceed can explore options to open a UK company from Djibouti with full banking support and structured onboarding assistance.

UK company banking and compliance for Djibouti entrepreneurs require structured execution, accurate documentation, and ongoing regulatory adherence. Each stage, registration, verification, and banking, demands precision. From My Company delivers a unified solution that aligns company formation, compliance, and banking integration. This approach reduces onboarding friction and ensures long-term operational stability for international entrepreneurs.

Frequently Asked Questions

Can I open a UK company from Djibouti as a non-resident?

Yes, you can open a UK company from Djibouti as a non-resident. From My Company enables Djibouti entrepreneurs to register a UK entity without requiring UK residency or citizenship.

What banking options are available to UK companies owned by Djibouti residents?

Djibouti residents can access UK business banking through digital banks and Electronic Money Institutions that support non-residents. From My Company guides clients toward compliant banking providers compatible with Djibouti-based directors.

Are there compliance requirements for UK companies owned by Djibouti entrepreneurs?

Yes, UK companies owned by Djibouti entrepreneurs must file annual accounts, submit confirmation statements, and meet anti-money-laundering verification requirements. From My Company ensures that Djibouti clients maintain ongoing compliance with Companies House requirements.

How long does it take to form a UK company from Djibouti?

UK company formation from Djibouti typically completes within 24 to 48 hours after document submission. From My Company streamlines the Djibouti registration process to accelerate approval timelines.

Do Djibouti entrepreneurs need a UK address for company registration?

No, Djibouti entrepreneurs do not need a UK address personally, but a UK registered office address is mandatory. From My Company provides a compliant registered office service for Djibouti-based directors forming UK companies.