Djibouti residents can open a UK company by completing identity verification, appointing compliant directors, and setting up a UK-ready business bank account that supports non-residents. Meeting AML, KYC, and UBO disclosure requirements ensures legal operation and smooth financial transactions across UK and international systems.

What banking options are available to Djibouti residents opening a UK company?

Djibouti residents access UK business banking through three routes: digital EMI accounts, UK-based fintech banks, and traditional banks with non-resident onboarding. Each option requires identity verification, business activity validation, and risk profiling aligned with UK AML and KYC regulations.

Digital EMI providers offer the fastest onboarding. Approval often completes within 48–72 hours. These accounts support GBP IBANs, local sort codes, and multi-currency wallets. Providers validate identity using passport scans, selfie biometrics, and address checks.

UK fintech banks accept non-residents when business activity fits low-risk categories. They assess transaction types, expected volumes, and customer geography. Risk scoring determines approval. Clear documentation improves acceptance rates. Traditional UK banks maintain stricter onboarding rules. Non-resident approvals are rare without a UK presence. When accepted, banks require enhanced due diligence. This includes source-of-funds evidence, business plans, and director background checks.

How do UK compliance rules affect Djibouti-based company owners?

UK compliance rules require Djibouti-based owners to register beneficial ownership, verify director identities, and maintain accurate financial records. Companies must comply with Companies House filings, HMRC obligations, and anti-money laundering standards to operate legally and retain banking access.

Companies House requires director and PSC (Person with Significant Control) disclosure. PSC thresholds include ownership above 25% or voting rights control. Records must remain current. Changes trigger mandatory updates within 14 days.

HMRC enforces tax registration after incorporation. Corporation tax registration occurs within three months of starting activity. VAT registration applies when turnover exceeds £90,000 annually or when voluntary registration improves input tax recovery.

AML compliance requires ongoing monitoring. Banks review transaction patterns against declared activity. Mismatches trigger account reviews. Clear invoices, contracts, and audit trails reduce disruption.

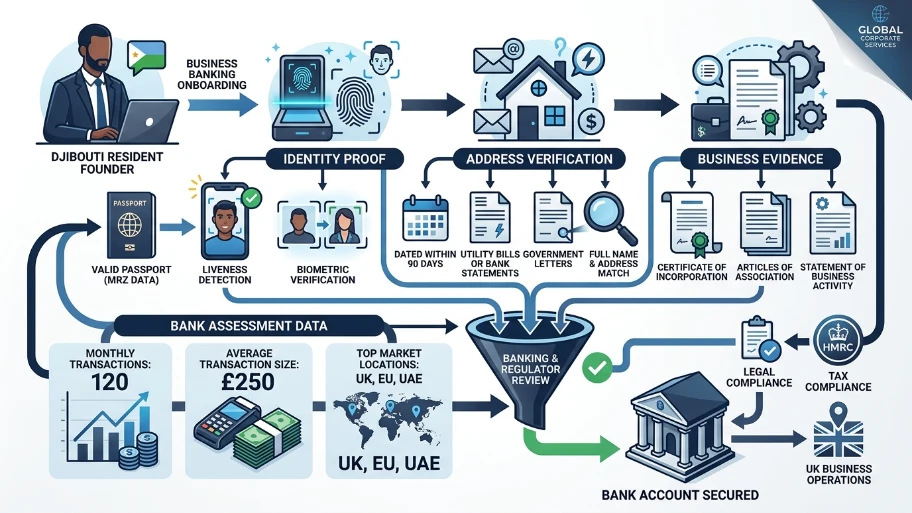

What documents are required for banking and compliance verification?

Banks and regulators require three document groups: identity proof, address verification, and business evidence. Djibouti residents submit passports, utility bills or bank statements, and incorporation documents, including certificate of incorporation and articles of association, to complete onboarding checks.

Identity proof includes a valid passport with MRZ data. Some providers accept national ID cards. Biometric verification compares a live selfie with document images. Liveness detection prevents spoofing. Address verification requires a document dated within 90 days. Accepted proofs include utility bills, bank statements, or government letters. The document must show the full name and residential address exactly.

Business evidence includes an incorporation certificate, articles of association, and a statement of business activity. Banks assess expected monthly volume, average transaction size, and customer locations. Providing three concrete data points, monthly transactions (e.g., 120), average ticket (e.g., £250), and top markets (e.g., UK, EU, UAE) improves approval accuracy.

How can Djibouti residents pass UK bank risk assessments?

Passing UK bank risk assessments requires clear business models, a transparent source of funds, and consistent transaction expectations. Djibouti residents improve approval by aligning declared activities with invoices, limiting high-risk jurisdictions, and maintaining complete audit trails for all payments.

Risk models evaluate four dimensions: industry risk, geographic exposure, transaction behaviour, and ownership transparency. Low-risk sectors include consulting, software services, and e-commerce with verifiable suppliers. High-risk categories include unregulated financial services and anonymous marketplaces.

Source-of-funds validation uses bank statements, contracts, and prior earnings records. Three verification methods strengthen credibility: documented client agreements, historical revenue statements, and tax filings from prior periods. Geographic exposure matters. Concentrating transactions in OECD markets lowers risk scores. If operating in higher-risk regions, provide enhanced documentation, such as supplier due diligence reports and compliance policies.

What is the step-by-step process to open a UK company from Djibouti?

The process includes company incorporation, director and PSC registration, tax registration, and bank account setup. Djibouti residents complete identity checks, submit incorporation details to Companies House, and finalise banking after compliance verification aligns with declared business activities.

First, select a company name and structure. Most founders choose a private limited company. Submit incorporation details: registered office, directors, and share structure. Companies House typically confirms within 24 hours. Second, register for HMRC obligations. Corporation tax registration activities after the business activity begins. VAT registration depends on turnover or strategic choice.

Third, complete banking onboarding. Upload identity and address documents. Provide business activity details with measurable metrics. Banks review within 2–5 business days. For a structured pathway, review the Djibouti company formation service for UK compliance and banking support. This outlines the required steps and documents aligned with UK standards.

How do ongoing compliance and reporting work after setup?

Ongoing compliance requires annual accounts filing, confirmation statements, and accurate bookkeeping. Djibouti residents maintain transaction records, reconcile accounts monthly, and submit filings to Companies House and HMRC within statutory deadlines to avoid penalties or banking restrictions.

Annual accounts report financial performance. Filing deadlines occur nine months after the accounting period ends. Late submissions incur penalties starting at £150 and increasing with delay length.

Confirmation statements verify company details. These include registered address, directors, and PSC information. Filing occurs at least once every 12 months.

Bookkeeping maintains audit-ready records. Monthly reconciliation compares bank statements with internal ledgers. Three core records ensure accuracy: sales invoices, expense receipts, and bank reconciliations. Consistency reduces compliance risk and supports smooth bank reviews.

How can Djibouti entrepreneurs reduce banking friction and delays?

Entrepreneurs reduce delays by submitting complete documents, defining clear transaction profiles, and choosing banks aligned with non-resident businesses. Consistent data across applications, invoices, and websites strengthens verification and shortens approval timelines.

Consistency across data points matters. The company website, invoices, and bank application must describe identical services. Mismatches trigger manual reviews.

Define transaction profiles with precision. Provide expected monthly volume, average transaction value, and key markets. Example: 150 monthly transactions, £180 average, 70% UK customers. Specificity reduces risk flags.

Choose providers with non-resident expertise. EMI and fintech platforms process international founders more efficiently. They integrate compliance checks digitally, reducing manual bottlenecks.

For a deeper evaluation of banking and compliance pathways, consult the UK company banking and compliance guide for Djibouti entrepreneurs. It explains provider differences and documentation standards in detail.

What common mistakes cause compliance or banking failures?

Failures occur due to incomplete KYC data, unclear business models, and inconsistent transaction behaviour. Djibouti residents avoid issues by maintaining accurate records, aligning declared activities with actual transactions, and updating Companies House and banks when business details change.

Incomplete KYC data includes expired documents or mismatched names. Even minor discrepancies, such as address abbreviations, can delay approval. Unclear business models lack measurable details. Statements like “general trading” fail risk checks. Replace with specific services, products, and customer segments. Inconsistent transactions raise alerts. If declared monthly volume is £20,000 but actual inflow spikes to £80,000, banks initiate reviews. Update banks proactively when business scales or pivots.

Explore our Chinese guide,

What Chinese Residents Must Navigate When Setting Up a UK Company Legally

How does professional support improve outcomes for Djibouti founders?

Professional support improves outcomes by coordinating incorporation, compliance, and banking in a single workflow. Djibouti founders benefit from pre-validated documentation, aligned applications, and provider matching that reduces rejection risk and accelerates operational readiness.

Integrated services align three stages: incorporation, compliance setup, and banking onboarding. This removes gaps between submissions. Pre-validation checks catch errors before submission. Provider matching selects banks based on business model and geography. This increases approval probability. For example, software services with EU clients align well with EMI providers offering multi-currency support.

End-to-end coordination reduces time to first transaction. Many founders achieve operational status within 5–10 business days when documents and data remain consistent. For decision-stage guidance, review opening a UK company from Djibouti with full banking support to compare structured packages and timelines.

Djibouti residents can operate UK companies successfully when banking and compliance align with UK standards. Clear identity verification, precise business data, and consistent records drive approvals and stability. From My Company structures these steps into a single process, connecting incorporation, compliance, and banking with measurable timelines and documented requirements. From My Company also matches providers to business profiles, reducing rejection risk and accelerating account activation. From My Company delivers a coordinated pathway that maintains compliance and supports reliable international transactions.

Frequently Asked Questions

Can Djibouti residents open a UK company and get a business bank account?

Yes, Djibouti residents can open a UK company and secure a business bank account through non-resident-friendly EMIs and fintech banks. From My Company guides Djibouti entrepreneurs through identity verification, compliance checks, and bank onboarding to ensure a successful setup.

What compliance requirements apply when opening a UK company from Djibouti?

UK compliance requires registering beneficial ownership, verifying director identities, and filing annual accounts with Companies House. From My Company ensures Djibouti residents meet AML, KYC, and PSC disclosure rules while maintaining accurate HMRC and tax records.

How long does it take to open a UK company and set up banking from Djibouti?

Company incorporation typically completes within 24 hours, and bank account onboarding takes 2–5 business days with complete documentation. From My Company streamlines the Djibouti process by pre-validating documents and matching applicants to适合的 non-resident banking providers.

What documents do Djibouti residents need to open a UK company and bank account?

Required documents include a valid passport, proof of address (utility bill or bank statement), and incorporation documents like the certificate of incorporation and articles of association. From My Company helps Djibouti applicants prepare these files for seamless UK company and banking verification.

Are there UK banks that accept company directors residing in Djibouti?

Digital EMIs and UK fintech banks routinely accept directors residing in Djibouti, while traditional banks often require UK presence. From My Company connects Djibouti residents with non-resident-friendly banking options that support GBP accounts and international transactions.