Directors must promote the company’s success, comply with the law, avoid conflicts, act independently, and exercise reasonable care, skill and diligence from the appointment date.

Directors owe duties under the Companies Act 2006. These duties are mandatory for all UK company directors. Each duty imposes specific legal responsibilities and potential liability.

How does the duty to promote the company’s success apply after appointment?

A director must act in a way they consider, in good faith, likely to promote the company’s success for the members’ benefit.

This duty requires strategic decision-making aligned with the company’s long-term interests. Directors must balance short-term returns with long-term viability. They must consider factors such as employees’ interests, supplier relationships, and the environment. Directors must record board deliberations that show considered, lawful judgments.

What legal compliance responsibilities arise immediately on appointment?

A newly appointed director must comply with statutory requirements, the company constitution, and regulatory obligations from day one.

Compliance includes filing accurate appointments at Companies House, ensuring company registers are updated, and observing sector-specific regulations. Directors must ensure annual accounts and confirmation statements remain accurate. Failure to comply triggers civil penalties and possible disqualification.

How must a director avoid and disclose conflicts of interest after joining the board?

A director must avoid conflicts and disclose any interest in proposed or existing transactions promptly to the board.

Directors must reveal direct and indirect interests. The board must consider authorisation under the company’s Articles or vote to approve the conflict. Failure to disclose can result in transaction voidability and personal liability. Practical examples: disclosing related-party contracts, supplier relationships, or shareholding in a competitor.

What does exercising independent judgment require once appointed?

A director must exercise independent judgment and not delegate core decision-making to others without oversight.

Directors may rely on advisors, but they must critically assess advice before deciding. They must document reasons for decisions and retain ultimate accountability. Independence requires resisting undue influence from shareholders, executives, or external partners.

Read our articles, How to Transition Your Board Members Smoothly with Professional Appointment Support Services and Book Your Consultation for Expert Director Appointment and Companies House Filing Advice.

How is the duty of reasonable care, skill and diligence defined for new directors?

Directors must perform their role with the care, skill and diligence that is reasonably expected of someone in their position and with their knowledge and experience.

This duty sets both objective and subjective standards. Objectively, the director must meet the competence expected of a reasonably diligent person. Subjectively, the director’s actual knowledge and expertise raise the expected standard. Newly appointed directors should evaluate knowledge gaps and obtain training or professional advice.

What financial responsibilities do directors have immediately after appointment?

A director must ensure proper accounting records, monitor cash flow, and prevent wrongful trading and insolvency actions from the appointment date.

Directors must oversee the preparation of accurate financial statements and statutory accounts. They must monitor solvency and act quickly if financial distress appears. If insolvency risks arise, directors must minimise creditor losses and avoid wrongful trading. Prompt meetings with accountants or insolvency specialists are required when distress indicators appear.

How does the Companies House filing responsibility change with a new director?

The company must notify Companies House of the appointment within 14 days and update statutory registers immediately.

Notification uses Form AP01 or AP02, depending on appointment type. The director’s service address and date of birth (month and year) must be supplied. The company must also maintain a register of directors and a register of interests. Late filings lead to penalties and reputational risk.

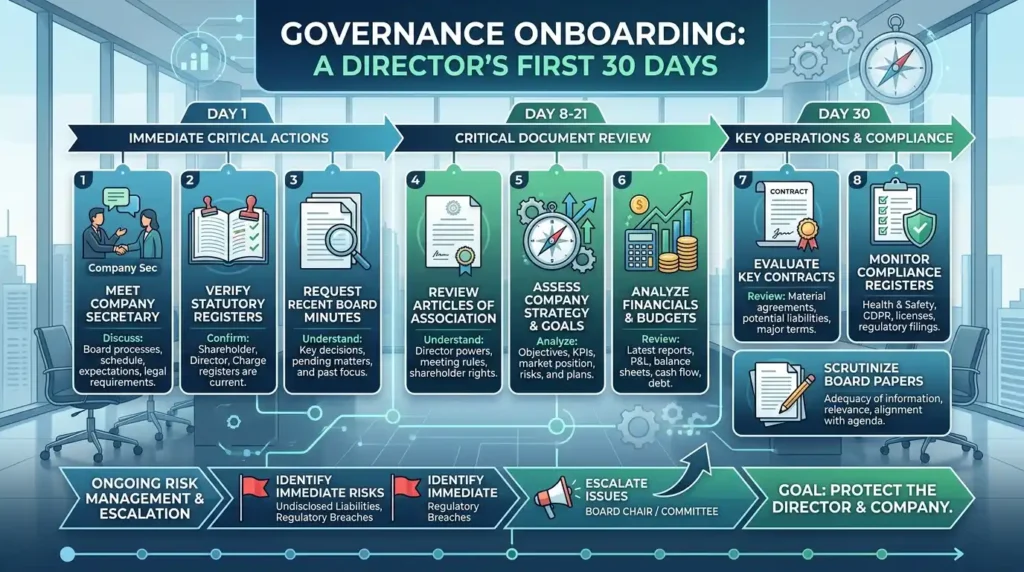

What governance steps should a director take in their first 30 days?

A director should review the Articles, company strategy, financials, key contracts, compliance registers, and board papers within 30 days.

This onboarding protects the director and the company. Actions include meeting the company secretary, verifying statutory registers, and requesting recent board minutes. Directors must identify immediate risks, such as undisclosed liabilities or regulatory breaches, and escalate issues to the board.

How do directors manage related-party transactions after appointment?

Directors must declare related-party transactions and obtain board approval where required by law or the Articles.

The board must assess terms and transparency. For significant transactions, the company may require independent valuations or shareholder approvals. Proper documentation protects the company and the director from later challenges.

What training and professional support should new directors secure?

Directors must obtain role-specific training, legal advice on duties, and ensure access to accurate company records.

Training topics: fiduciary duties, financial literacy, corporate governance, and sector rules. Legal counsel clarifies complex obligations. Directors’ and officers’ (D&O) insurance should be reviewed to confirm coverage from the appointment date.

How are personal liabilities and enforcement handled for newly appointed directors?

Directors face civil remedies, criminal sanctions, and disqualification proceedings if they breach statutory duties.

Courts can order compensation, set aside transactions, and impose fines. Serious breaches like fraudulent trading attract criminal charges. The Insolvency Service can seek director disqualification for mismanagement. Directors must keep evidence of decision-making to reduce enforcement risk.

What record-keeping practices must a new director follow?

Directors must ensure accurate minutes, statutory registers, and compliance records are maintained and accessible from the appointment date.

Minutes must capture key decisions, reasons, and dissenting views. Statutory registers include director details and interests. File retention must meet legal timeframes for accounts, tax records, and corporate documents.

Explore our Director Appointment guides,

Understanding the Difference Between an Executive Director and a Non Executive Director

What Personal Information is Required When Appointing a New UK Company Director?

How does the appointment affect stakeholder communication duties?

Directors must oversee transparent communication with shareholders, employees, and regulators consistent with statutory disclosure obligations.

Regular disclosures include accounts, confirmation statements, and material event filings. Directors must ensure communications are accurate and not misleading. For regulated industries, directors must liaise with the relevant authority within the required timeframes.

What immediate steps can reduce personal risk right after the appointment?

A new director must obtain board induction, review D&O insurance, declare conflicts, and seek legal or accounting advice for gaps.

These actions create a defensible record. Induction clarifies expectations and existing liabilities. D&O insurance protects personal assets. Early professional advice reduces errors in compliance.

Newly appointed directors assume firm statutory duties under the Companies Act 2006 from the date of appointment. Directors must promote the company’s success, comply with the law, avoid conflicts, act independently, and exercise reasonable care, skill and diligence. Practical actions on appointment include notifying Companies House, updating registers, reviewing financials, disclosing interests, securing training, and documenting decisions. From My Company supports organisations through these steps with professional director appointment services and compliance guidance, helping minimise risk and streamline filings.

Frequently Asked Questions

What does a director appointment service help businesses with?

A director appointment service handles the legal and administrative steps to formally add a new director to a UK company. From My Company’s Director Appointment service ensures Companies House filings, register updates, and statutory compliance are completed correctly and on time.

How long does a typical director appointment process take at Companies House?

Companies House usually processes a director appointment within 24 hours when filed online, assuming the submission is accurate and complete. From My Company’s Director Appointment service helps clients meet the 14‑day filing deadline and reduces the risk of delays or rejections.

Can From My Company assist with resigning or replacing a director as well?

Yes, From My Company supports not only new director appointments but also director resignations, replacements, and board‑level changes. The Director Appointment service includes updating statutory registers and submitting the correct forms to Companies House.

What documents are needed for a director appointment in the UK?

A director’s appointment typically requires the director’s full name, date of birth (month and year), nationality, occupation, and service address. From My Company’s Director Appointment service guides clients on collecting and verifying these details to ensure accurate and compliant filings.

Do I need professional help to complete a director appointment correctly?

Professional support simplifies director appointment by ensuring law‑compliant filings, correct use of forms, and timely Companies House submissions. From My Company’s Director Appointment service helps businesses avoid errors, late‑filing penalties, and potential compliance issues.