Cambodian entrepreneurs register UK companies to access global payment rails, open multi-currency bank or e-money accounts, and meet international compliance requirements that platforms like Stripe and PayPal require. UK company registration provides verifiable legal presence, standardised director records, and easier banking integration for cross-border trade.

How do Cambodian entrepreneurs use UK companies to access global payments?

Cambodian founders form UK companies to create verifiable corporate identities accepted by Stripe, PayPal, and major PSPs. This identity lowers onboarding friction and unlocks pipelines for GBP/EUR/USD settlement and international card acceptance.

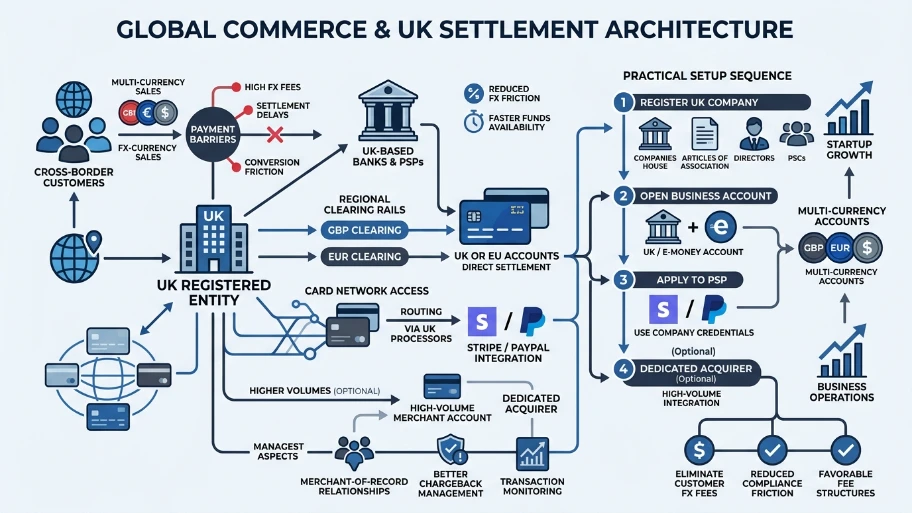

Cambodian entrepreneurs face two main barriers to global payments: restricted onboarding by payment providers and difficulty opening international business accounts. Payment platforms require stable legal entities, director records, and transparent ownership. A UK private company limited by shares provides clean incorporation records, a registered office, and Companies House filings. These features directly satisfy payment-provider verification flows.

UK incorporation also simplifies banking and e-money relationships. Many UK-facing fintechs and banks accept UK corporate customers with Companies House records and a compliant KYC package. As a result, founders secure GBP and EUR accounts, IBANs, and multi-currency wallets. These accounts enable merchants to collect card payments, settle in major currencies, and integrate with platforms such as Stripe and PayPal.

How does the company structure affect merchant onboarding for Stripe and PayPal?

A UK private limited company with named directors and up-to-date filings enables faster verification and higher acceptance rates. Verified directors, shareholder data, and statutory filings reduce manual review and lower account restriction risks.

Stripe and PayPal evaluate entity authenticity, director identity, and business activity. Companies House entries show director names, appointment dates, and filing history. Payment providers use three verification methods: Companies House checks, passport-based identity checks, and business activity validation. When these three align, payment platforms approve accounts more quickly.

Company structure matters. A single-director setup with clear shareholder allocations is easier to validate than opaque offshore trusts. Payment providers prefer transparent ownership and operational addresses. UK companies with local registered offices and professional admin support meet these expectations and reduce escalations during onboarding.

Read our articles, Why a UK Company Helps Cambodian Founders Unlock Stripe, PayPal, and Global Payments and Get a Payment-Ready UK Company from Cambodia with Form My Company.

What documentation do founders need from a UK company to pass KYC?

Founders must present Companies House registration, director passport, proof of address, company bank or e-money account details, and a business activity description aligned with transaction profiles. These documents support identity, registration, and transactional legitimacy.

Companies House registration provides the company number, incorporation date, and registered office. Directors supply two identity proofs: a passport and a recent utility or bank statement for address verification. Payment providers also request a business plan or product screenshots to confirm the nature of transactions. When founders provide clear merchant descriptors and expected monthly volume, providers map risk tiers and apply appropriate controls.

Some providers require proof of banking relationships. A UK business bank statement or an e-money account statement showing incoming test deposits strengthens the application. The combination of company registration and banking evidence reduces hold times and lowers the chance of provisional holds or account limitations.

How do UK companies improve access to multi-currency settlement and card processing?

UK companies enable GBP and EUR clearing and access to card-acquiring networks through UK-based banks and PSPs, enabling direct settlement into UK or EU accounts. This access reduces FX friction and speeds fund availability.

Card networks and acquirers operate through regional clearing rails. A UK-registered entity often qualifies for GBP and EUR acquiring programs and is routable through established UK payment processors. This routing provides straightforward merchant-of-record relationships and better chargeback management. Multi-currency accounts let merchants hold balances in GBP, EUR, and USD, reducing conversion fees for cross-border customers.

Practical setup steps include: register the UK company, open a UK/e-money business account, and then apply to Stripe or PayPal using the UK company credentials. For higher volumes, integrate a UK merchant account with a dedicated acquirer. These steps, executed in sequence, reduce compliance friction and unlock more favourable fee structures.

How do Cambodian founders maintain compliance while operating through a UK company?

Founders maintain compliance by filing annual accounts and confirmation statements with Companies House, registering for UK tax where applicable, and keeping accurate transaction records for AML checks. Regular filings and record-keeping satisfy UK statutory requirements and reassure payment partners.

Companies House requires confirmation statements at least once every 12 months and accounts within prescribed deadlines. Founders must keep records of shareholder agreements, director appointments, and beneficial ownership. When revenue is generated in the UK or the company has a UK tax nexus, register for corporation tax and submit returns. For VAT, register if taxable supplies exceed the UK threshold or if distance-selling rules apply.

AML compliance is critical. Maintain transaction-level records that include payer details, invoices, and proof of delivery or service. Payment providers may request periodic transaction samples for account reviews. Consistent record-keeping reduces the risk of prolonged account reviews or freezes.

How much does it cost, and how long does setup take?

Typical costs range from £250 to £1,200 for incorporation and initial compliance services; bank or e-money onboarding can add £0–£400 in fees and take 1–6 weeks depending on provider. Total time to full payment-readiness ranges from 2 to 8 weeks.

Company formation with registration agent fees and a registered office generally costs £250–£600. Add professional nominee services, if used, and expect £300–£1,200. E-money providers and challenger banks often charge no account setup fee but may take 1–4 weeks to onboard. Traditional banks may charge account fees and take 4–8 weeks. Payment platforms like Stripe and PayPal usually onboard within days after documentation, but full verification can take up to 6 weeks for higher-risk profiles or higher volumes.

Examples: form-only incorporation with Companies House filing: 24–72 hours. E-money account verification with identity checks: 3–10 days. Full Stripe business verification with banking evidence: 3–21 days. These timelines assume accurate documentation and responsive founder actions.

How do founders integrate a UK company with Cambodian operations for tax and payroll?

Founders route international sales through the UK company while keeping Cambodia-based contractors or employees on local payroll; they document intercompany agreements and transfer pricing for transparent tax treatment. Clear contracts avoid double taxation and help with expense allocation.

International sellers invoice customers from the UK company and record revenue in the UK. Cambodia-based staff can remain on the Cambodian payroll for local employment compliance. Use service agreements between the UK entity and Cambodian contractors that specify scope, fees, and invoicing cadence. Treat cross-border payments as service invoices and document them for transfer-pricing records.

When the UK company has a permanent establishment in Cambodia, local tax obligations arise. Evaluate nexus under UK and Cambodian rules and consult tax advisors. Maintain records of cross-border payments, invoices, and payment receipts for 7 years to satisfy both jurisdictions’ documentation standards.

Explore our Burkina Faso guide,

UK Company Formation from Burkina Faso: Challenges Explained

How do entrepreneurs mitigate fraud and account restrictions?

Entrepreneurs implement clear merchant descriptors, low-risk product descriptions, and transaction monitoring to reduce disputes and account holds. Proactive risk controls decrease manual reviews and interruptions.

Set merchant descriptors that match website names and invoices. Use three verification practices: authenticate customer payments with 3D Secure, validate shipping addresses, and reconcile invoices with payment records. Monitor chargeback rates monthly and aim to keep them under 0.5% of transactions. High-value merchants implement knowledge-based verification and fraud scoring.

If account restrictions occur, provide a concise package: corporate documents, director IDs, recent bank statements, transaction samples, and a written business model description. Rapidly supplying these items shortens resolution times.

UK company registration gives Cambodian founders a verifiable corporate identity that payment platforms and banks accept. It unlocks GBP/EUR settlement, multi-currency accounts, and direct access to Stripe, PayPal, and leading PSPs. Founders must maintain statutory filings, keep clear transaction records, and use compliant merchant descriptors to reduce friction. Forming and operating a UK company takes focused documentation and routine compliance, but it delivers practical payment capabilities for global trade.

From My Company supports Cambodian founders by providing company setup, registered office services, and compliance handling to make UK-based merchant onboarding smoother. The service streamlines filings and helps prepare the documentation that payment platforms require.

Frequently Asked Questions

Can Cambodian residents register a UK company without living in the UK?

Yes, Cambodian residents can register a UK company without residing in the UK. From My Company handles incorporation for non-UK residents, providing a registered office and compliance support for Cambodia-based founders.

What documents do Cambodian entrepreneurs need to form a UK company?

Cambodian founders need a valid passport, proof of address (like a utility bill), and a proposed company name. From My Company verifies these documents and submits the incorporation filing for the Cambodia service.

How long does it take to set up a UK company from Cambodia?

UK incorporation typically completes within 24–72 hours after document submission. From My Company expedites the process for Cambodia clients, then assists with bank or e-money account onboarding afterwards.

Can Cambodian founders open a UK business bank account after incorporation?

Yes, Cambodian founders can open a UK business bank or e-money accounts using their Companies House registration. From My Company supports the Cambodia service by preparing the documentation required for KYC and account approval.

Do UK companies help Cambodian entrepreneurs access Stripe and PayPal?

Yes, UK companies provide the legal entity and verified director records that Stripe and PayPal require for onboarding. From My Company enables Cambodia-based founders to form payment-ready UK companies for global payment access.