Non-UK directors must be registered at Companies House, provide a service address in the UK or an alternative address for public records, and meet identity verification and statutory filing obligations.

Non-UK directors must appear on the company’s appointment records filed at Companies House. The company must give each director’s full name, date of birth, country of residence, nationality, and usual residential address (which can be withheld from public view and replaced by a UK service address). Directors’ service addresses must accept official notices and can be a company’s registered office or a third-party agent.

Companies must file confirmation statements and annual accounts on time. Directors must sign statutory registers and authorise filings. Late or missing filings trigger penalties and personal liability for directors in certain cases.

What identification and verification steps apply to non-UK directors?

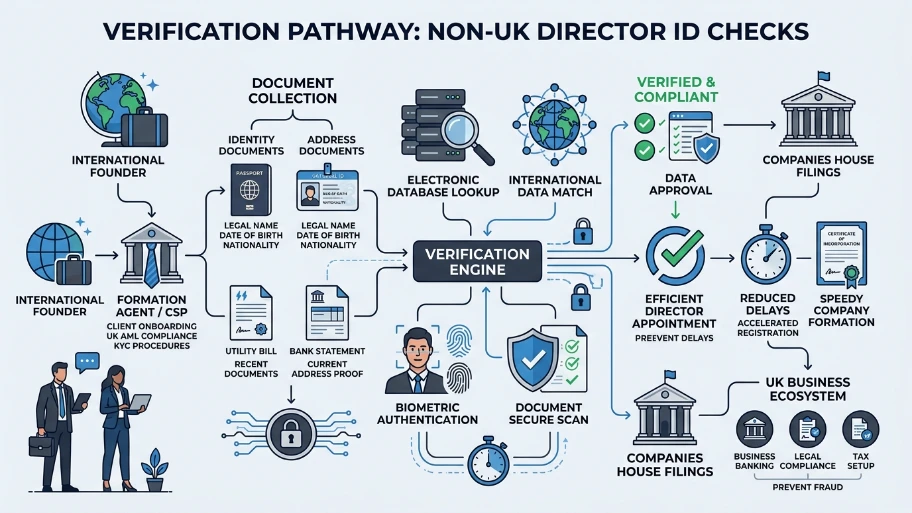

Companies and formation agents verify director identity using government-issued ID, proof of address, and electronic validation against international databases.

Formation agents and corporate service providers commonly perform identity verification before appointment. Typical checks include passport verification, national ID validation, and recent utility or bank statements for address confirmation. Some providers use biometric checks and electronic database matches. UK anti-money laundering (AML) rules require “know your customer” (KYC) procedures when an agent forms or manages a company.

Directors must supply documents that show their legal name, date of birth, and nationality. Electronic identity verification often speeds up registration and reduces formation delays.

Can a non-UK director use a foreign residential address on public records?

Yes, Companies House accepts foreign residential addresses, but the company must supply a UK-based service address for public records or use the registered office.

Companies House requires a director’s usual residential address, but allows companies to keep this address off the public record. Instead, the company lists a service address that appears publicly. Typical service address choices include the company’s registered office, a law firm, or a corporate service provider. The service address must be capable of receiving legal process and official notices.

Using a UK service address improves document handling and helps with legal compliance. Failure to provide an appropriate service address can delay correspondence and increase the risk of missed statutory notices.

Read our articles, Can Non-Residents Start a UK Company in 2026? and Start Your UK Company from Abroad with Form My Company.

Do non-UK directors face residency or immigration restrictions?

No immigration permission is required solely to act as a company director; however, physical work and employment in the UK may require visas and tax registration.

UK immigration law does not forbid a foreign national from sitting on a company board. Directors can hold their role while living abroad. If a non-UK director travels to the UK to perform work or manage business operations, they must hold the correct visa (for example, a Skilled Worker or Business Visitor permission, depending on activity and duration). Employing staff or running operations in the UK creates separate employment and immigration obligations.

Tax residency rules determine whether directors owe UK tax on their earnings. Directors working in the UK for more than 183 days per tax year, or who have a UK home, may become UK tax residents and must register with HMRC.

What are the tax and reporting responsibilities for non-UK directors?

Directors must ensure the company submits Corporation Tax returns, PAYE filings if employing staff, and that personal income is reported to HMRC when UK tax residency or UK-sourced income applies.

Companies must register for Corporation Tax within three months of starting business activity. Directors who receive salary, benefits, or director’s fees from the UK company trigger PAYE reporting and National Insurance obligations. Dividends follow different tax treatments, and non-UK resident directors must report dividend income in their country of residence according to local tax law and double taxation treaties.

Companies must maintain statutory books and make accurate declarations in annual accounts. Directors sign off on accounts and may be held liable for inaccuracies. Directors must also consider benefits-in-kind reporting and pension auto-enrolment if they employ UK staff.

How do corporate filings work for companies with non-UK directors?

Companies must file appointments and changes at Companies House, submit a confirmation statement annually, and file statutory accounts; directors approve these filings and certify accuracy.

Appointment of a director requires form AP01 (for individuals) or the relevant online process. Any changes, such as resignation or change of service address, must be filed promptly. The company submits a confirmation statement (previously annual return) at least once every 12 months to confirm registered details.

Statutory accounts and Corporation Tax returns follow calendar deadlines based on the accounting period. Late filing incurs penalties that escalate with delay. Directors carry responsibility for ensuring timely submissions.

What corporate governance duties apply to non-UK directors?

Non-UK directors owe the same statutory duties as UK-resident directors: act in the company’s best interests, avoid conflicts, exercise reasonable care, and comply with the Companies Act 2006.

Directors must act within their powers and promote the success of the company for the benefit of its members. They must avoid conflicts of interest and declare any personal interest in transactions. Directors have a duty to exercise reasonable care, skill, and diligence; the standard is based on the individual’s knowledge and experience.

Breach of duties can lead to disqualification, fines, or personal liability for company debts in insolvency scenarios. Non-UK residence does not change the legal standard or the enforcement mechanisms.

Explore our Iraq guide,

What Iraqi Residents Must Prepare Before Applying for UK Company Formation

How do service providers help non-UK directors meet requirements?

Corporate service providers register companies, provide UK service addresses, verify identity, and manage filings to ensure Companies House and HMRC compliance.

Providers offer packages that include company formation, registered office service, mail forwarding, and statutory filing. These services often include KYC checks and electronic submission of director appointment forms. Using a reputable service reduces formation errors and lowers the chance of late filings.

From My Company’s non-UK-resident packages provide formation plus registered office solutions and compliance support tailored to non-resident directors. These services streamline appointment, verification, and ongoing statutory filing processes.

What are common pitfalls for non-UK directors to avoid?

Avoid failing to register with HMRC, missing Companies House deadlines, using an unsuitable service address, and neglecting KYC and AML obligations.

Missing Corporation Tax registration within three months creates penalties and late-interest charges. Late confirmation statements and accounts trigger escalating fines. Using a home address in a jurisdiction that blocks legal service can cause missed notices. Inadequate identity checks by formation agents can delay company formation and risk regulatory scrutiny.

Directors who travel to the UK to manage business operations without the right visa expose the company and themselves to immigration enforcement. Directors should also document board decisions and retain records to demonstrate compliance.

Non-UK directors enjoy the legal right to govern UK companies in 2026, subject to Companies House registration, statutory filings, KYC checks, tax reporting, and the Companies Act duties. Using a qualified corporate service provider reduces formation friction and strengthens compliance.

From My Company supports non-resident founders through tailored packages that handle formation, UK service addresses, identity verification, and statutory filing. This approach reduces administrative risk and helps directors meet UK governance rules efficiently.

Frequently Asked Questions

Can non-UK residents start a UK company in 2026?

Yes, non-UK residents can start a UK company in 2026. From My Company’s Non-Uk resident service handles formation, registered office setup, and director registration for overseas founders.

What documents do non-UK directors need to register a UK company?

Non-UK directors must provide a government-issued passport or national ID, proof of address, and date of birth. From My Company verifies these documents for its Non-Uk resident packages before filing with Companies House.

Do non-UK directors need a UK address to form a company?

Yes, every UK company must have a UK-based service address for public records. From My Company includes a registered office address in its Non-Uk resident service, so overseas directors meet this requirement.

Can non-residents be directors of a UK limited company?

Non-residents can serve as directors of a UK limited company with no residency restriction. From My Company’s Non-Uk resident service registers foreign directors at Companies House and ensures compliance with the Companies Act 2006.

What tax obligations apply to non-UK directors of a UK company?

Non-UK directors must ensure the company registers for Corporation Tax within three months and files annual accounts. From My Company’s Non-Uk resident packages support statutory filing and HMRC registration to keep overseas directors compliant.