A private limited company (Ltd) suits most businesses with limited liability for shareholders and flexible share issuance for growth, while a Limited Liability Partnership (LLP) fits professional services like law or accounting with partner-managed liability protection and pass-through taxation. Both register via Companies House for £12 online, but Ltds require directors/shareholders and annual accounts, whereas LLPs need designated members and profit-sharing agreements. Choose Ltd for scalability, LLP for simplicity in partnerships.

Comparing private limited company vs LLP UK helps entrepreneurs select optimal business structures for company formation under the Companies Act 2006 and Limited Liability Partnerships Act 2000. With over 800,000 annual registrations at Companies House, Ltds dominate (95%) for startups offering liability caps, 19-25% Corporation Tax, and SEIS funding, while LLPs (4%) appeal to solicitors, architects, and consultants avoiding corporate bureaucracy. Keywords like private limited company vs LLP UK highlight differences in directors vs designated members, shareholders vs partners, and compliance burdens.

Semantic factors—registered office, SIC codes, VAT (£90k threshold), PAYE—apply to both, but Ltds file public accounts, LLPs submit lighter returns. Post-Brexit, non-residents favour Ltds for investor appeal. Risks like fines (£1,500 Confirmation lapses) underscore choice’s impact.

This authoritative 2026 analysis, drawn from extensive UK formation expertise, breaks down formation, taxation, and scalability with examples. Whether launching tech (SIC 62012) or a law firm, understand these to align structure with goals, ensuring compliance and growth.

Step-by-Step Comparison: Formation and Structure Differences

Formation: Both file online (£12 Ltd, £40 LLP via IN01/LL IN01). Ltd needs company name, director(s), shareholder(s), registered office, SIC codes, memorandum/articles. LLP requires name, designated members (min. 2), registered office, LLP agreement (profit shares).

Management: Ltd mandates directors (1+ natural persons) with fiduciary duties (s.172); shareholders vote dividends. LLP partners self-manage without directors; designated members handle filings.

Ownership: Ltd shares transferable, scalable for investors. LLP partner interests non-transferable without consent, capped at members.

Timeline: Ltd instant-24hrs; LLP 24-48hrs due agreement review.

Example: Tech startup forms Ltd “CodeFlow Ltd” (1 director/shareholder, virtual office, SIC 62012)—CRN Day 1, issues shares for VC. Accounting duo forms “Smith LLP” (2 designated members, profit split 50/50)—LLP agreement outlines exits, files lighter accounts. Ltd scales nationally; LLP stays boutique. This step-wise view reveals Ltd flexibility vs LLP simplicity.

Benefits and Potential Risks of Each Structure

Ltd Benefits: Limited liability to unpaid shares protects assets; “Ltd” credibility aids banks/investors. Shares raise capital (SEIS 50% relief); Corporation Tax 19-25% with dividends (£500 allowance). Scalable to PLC.

LLP Benefits: Pass-through taxation—profits taxed as income (avoid double tax); flexible profit allocation. No annual accounts audit for small LLPs; privacy on partner salaries.

Risks: Ltd public accounts expose finances; director disqualification (15 years) for misconduct. LLP partners liable for own tax (45% higher bands); dissolution winds personal assets if indemnity gaps.

Case: Manchester Ltd issues 20% shares for £100k, deducts R&D—grows 3x. LLP accountants split £200k profits tax-efficiently but cap at partnership scale. Ltd suits growth; LLP stability. Trade-offs demand goal alignment.

Legal and Compliance Considerations: Ltd vs LLP

Filing: Ltd annual Confirmation Statement (£13), accounts (micro balance sheet free). LLP CS (£13), annual review statement, lighter accounts (no profit/loss for small).

Tax: Ltd Corporation Tax CT600 iXBRL (12 months year-end); PAYE for salaries, VAT MTD. LLP self-assessment partnership return (partners SA100); no CT, PAYE only employees.

Duties: Ltd directors ss.170-177 (good faith); LLP members unlimited fiduciary but limited liability.

Dissolution: Ltd strike-off £8-£10; LLP winding via members.

GDPR/ICO £40+ both. Brexit EORI same.

Example: Bristol Ltd files abridged accounts (£200 accountant), PSC public. LLP submits turnover only (£100)—less scrutiny. Ltd suits public-facing; LLP private practices. Compliance costs Ltd 20% higher annually.

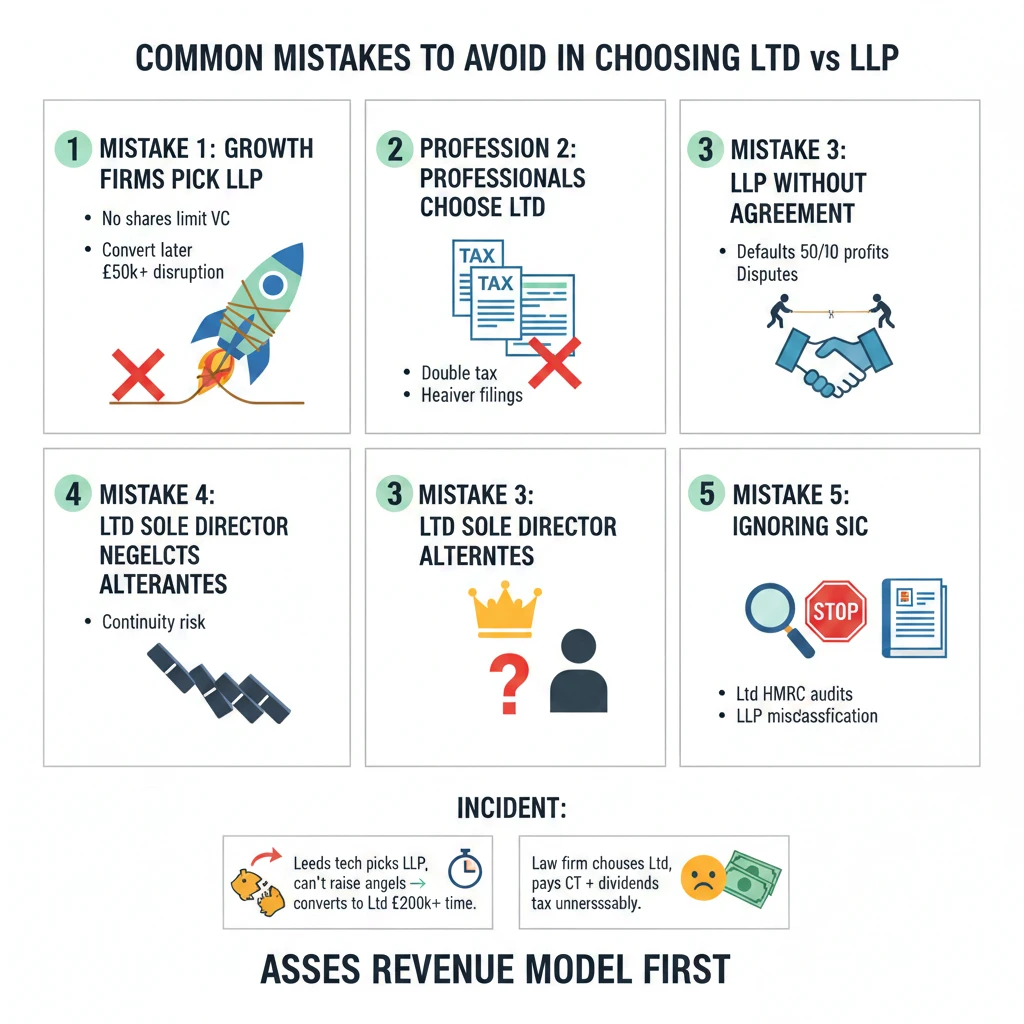

Common Mistakes to Avoid in Choosing Ltd vs LLP

Mistake 1: Growth firms pick LLP—no shares limit VC; convert later (£50+ disruption).

Mistake 2: Professionals choose Ltd—double tax, heavier filings.

Mistake 3: LLP without agreement—defaults 50/50 profits, disputes.

Mistake 4: Ltd sole director neglects alternates—continuity risk.

Mistake 5: Ignoring SIC—Ltd HMRC audits; LLP misclassification.

Incident: Leeds tech picks LLP, can’t raise angels—converts to Ltd (£200+ time). Law firm chooses Ltd, pays CT + dividends tax unnecessarily. Assess revenue model first.

Practical Tips and Best Practices for Structure Selection

Assess scalability: Projected >£100k Year 2? Ltd. Partners 2-20? LLP.

Tax model: Corporate 19% + dividends? Ltd. Pass-through? LLP.

Consult accountant (£150 session). Draft LLP agreement (£300 solicitor).

File both online pre-noon weekdays. Ltd: Model articles. LLP: Partnership deed template.

Example: Edinburgh consultancy (2 founders, £50k projected)—Ltd for shares. Architects (4 partners)—LLP for tax flow. Review annually; convert via Companies House. Hybrid models rare.

Frequently Asked Questions (FAQs)

Private limited company vs LLP UK: Which is better for startups?

Ltd—shares attract investors, SEIS relief. LLP limits equity raises.

Can one person form an LLP in the UK?

No; minimum 2 designated members. Ltd allows solo director/shareholder.

Tax differences between Ltd and LLP?

Ltd: Corporation Tax 19-25%, dividends. LLP: Partner income tax, no CT.

Switching from LLP to private limited company UK?

Yes; incorporate Ltd, transfer assets (£50 filing + stamp duty).

Compliance burden: Ltd vs LLP?

Ltd heavier accounts; LLP lighter but self-assessment complex.

Private limited company vs LLP UK choice shapes trajectory—Ltd for expansion, LLP for partnerships. Align with goals for optimal compliance and growth.

If you’re ready to register your company with confidence, Form My Company provides fast, fully online company formation with expert compliance support, VAT & PAYE setup, virtual office solutions, and professional guidance. Get started today and let our specialists handle the paperwork while you focus on growing your business.