Bangladeshi residents can form a UK company, but they face UK tax residency tests, potential personal tax on UK-source income, and compliance risks such as PSC reporting, AML checks, and bank-account refusal. Follow documented verification and UK filing rules to minimise exposure.

What taxes apply when a Bangladeshi resident registers a UK company?

A UK-registered company pays UK corporation tax on its UK taxable profits; Bangladeshi resident directors may face UK personal tax only on UK-source employment or directorship income and on profit distributions if UK-resident for tax.

A UK company is taxable under UK corporation tax at a single rate of 25% for profits above the marginal threshold in 2026. The company must file CT600 returns and pay corporation tax within nine months and one day after the accounting period end. Dividends paid to Bangladeshi shareholders are not taxed by the company but may generate personal tax obligations in Bangladesh under local rules; verify double taxation relief under the UK–Bangladesh Double Tax Agreement for dividend withholding and relief. Directors who perform duties in the UK or receive employment income from the UK company must register for UK PAYE and may be liable for UK income tax and National Insurance contributions on that income. The company must operate PAYE for any UK tax-liable payments and maintain payroll records.

What personal tax risks do Bangladeshi founders face with a UK company?

Personal tax risk arises if the director becomes UK tax-resident, performs duties in the UK, receives UK-source income, or extracts profits as dividends, which may attract tax in Bangladesh or require double-tax relief claims.

Residence status uses the UK Statutory Residence Test. If a director spends 183+ days in the UK in a tax year or meets sufficient ties, HMRC will treat them as UK tax-resident. UK tax residents pay UK tax on worldwide income; non-residents pay UK tax on UK-source income only. Dividend extraction creates reporting obligations: the company issues dividend vouchers, and shareholders must declare dividends to local tax authorities. Bangladeshi tax law may tax foreign dividends; the UK–Bangladesh treaty outlines relief mechanisms and withholding rules. Directors should track travel days, duties performed remotely versus in the UK, and maintain clear payroll documentation to limit unintended UK personal tax exposure.

Read our articles, What Bangladeshi Applicants Face When Registering a UK Company: Documents, Delays, Approval Odds, and Register Your UK Company from Bangladesh with Full Compliance & Banking Setup.

What compliance and reporting obligations does a UK company face after formation?

A UK company must register with Companies House, file annual accounts and confirmation statements, report Persons with Significant Control (PSC), and comply with Anti-Money Laundering (AML) and Know Your Customer (KYC) checks.

Companies House registration requires a registered office in the UK, a director, and a PSC declaration within 14 days. Annual accounts must follow UK GAAP or IFRS for small-company thresholds and file within nine months of the year end. The confirmation statement (CS01) must update shareholder and director details every 12 months. AML checks require verification of beneficial owners and identity sources; firms use passport checks, biometric scans, and address validation as three common verification methods. Failure to comply triggers penalties, the possibility of strike-off, and reduced chances of opening UK business bank accounts.

How likely is a UK bank to open a business account for a Bangladesh-based applicant?

Banks approve accounts based on risk assessments; many UK banks decline non-resident directors without UK presence, while specialist fintech and international banks accept verified Bangladeshi applicants after enhanced due diligence.

High-street banks apply strict AML and economic substance checks. They assess director residency, business activity, and transactional patterns. Banks prefer a UK-resident director or business operations in the UK. Specialist providers and challenger banks often accept non-UK resident directors when applicants provide certified ID, proof of address, business plans, and PSC documentation. Prepare notarised documents, certified translations, and proof of expected turnover to increase approval odds. Expect longer onboarding: 2–12 weeks, depending on provider and documentation quality.

What AML and KYC checks will Bangladeshi applicants undergo?

Applicants face identity verification, beneficial ownership validation, and source-of-funds checks; typical methods include passport checks, biometric scans, and address validation with certified documents.

UK firms follow the Money Laundering Regulations 2017 framework. Identity verification uses government-issued passports and photo ID. Address validation requires utility bills, bank statements, or certified letters dated within three months. Beneficial owners are authenticated against UK corporate registries and PSC records. Source-of-funds checks validate capital used to start the company and initial deposits, usually via bank statements or certified transaction evidence. Businesses dealing in high-risk sectors—crypto, trading, or cash-heavy operations face enhanced due diligence and transaction monitoring.

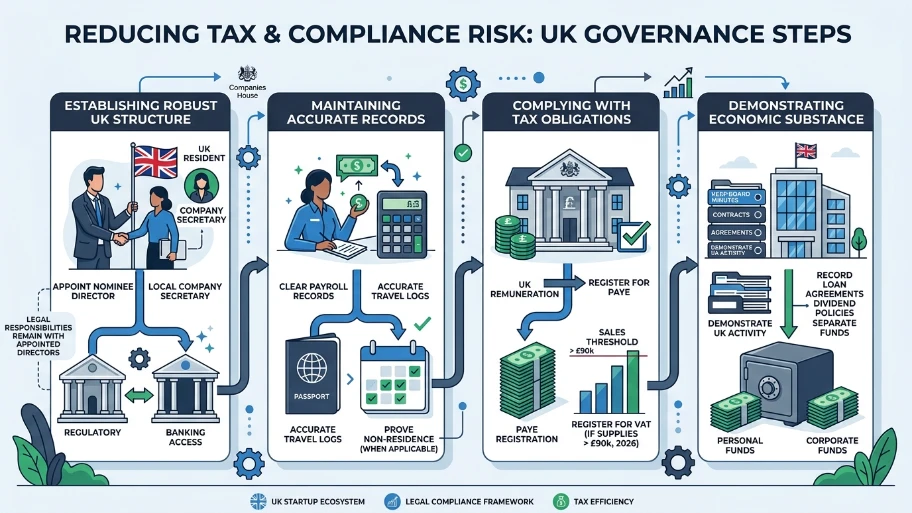

What governance steps reduce tax and compliance risk?

Appoint a UK-resident nominee director or local company secretary, maintain clear payroll and travel records, register for PAYE and VAT where required, and document economic substance in the UK.

Nominee or local directors provide a UK presence for banks and regulators, but legal responsibilities remain with the appointed directors. Maintain accurate travel logs to prove non-residence when relevant. Register for PAYE if directors receive UK remuneration and register for VAT when taxable supplies exceed the VAT threshold (£90,000 in 2026). Create a UK business address and keep board minutes, contracts, and rent/service agreements that demonstrate genuine UK economic activity. Record loan agreements and dividend policies to show separation between personal and corporate funds.

What are the main legal and reputational risks for non-resident founders?

Legal and reputational risks include failure to register PSCs, late filing penalties, AML breaches, and being flagged by banks or HMRC for suspicious activity that can lead to account closure or fines.

Companies House enforcement imposes fines for late accounts and confirmation statements. Failure to disclose PSCs risks criminal penalties and restrictions on share transfers. AML failures can trigger large fines and director disqualification. Banks may freeze accounts or close relationships when onboarding documentation appears incomplete or when transaction patterns deviate from declared business activity. Transparent governance, timely filings, and consistent bookkeeping reduce red-flag exposure and protect the company’s reputation.

What practical process should a Bangladeshi applicant follow to register and operate compliantly?

Register the company with Companies House, verify identities with certified documents, open a suitable bank account, set up PAYE and VAT as required, and keep annual filings and PSC data current.

Step 1: Choose a company structure and prepare the Memorandum and Articles of Association. Step 2: Register with Companies House using a registered UK address and list directors and PSCs. Step 3: Verify director and shareholder identities using passport checks, biometric scans, and address validation. Step 4: Apply to banks that accept non-resident customers and provide certified KYC and business evidence. Step 5: Register for corporation tax within three months of starting a business, register for PAYE for any UK pay, and register for VAT if turnover is anticipated to exceed the threshold. Step 6: File annual accounts, confirmation statements, and CT600 returns on schedule.

Forming a UK company from Bangladesh is a practical option with clear rules. The primary fiscal obligation is UK corporation tax on company profits at 25% for relevant profits. Personal tax only arises for UK-source income or if directors become UK tax-resident under the Statutory Residence Test. Compliance risks centre on PSC reporting, AML/KYC, and banking acceptance; thorough documentation and a local presence reduce those risks. From My Company provides end-to-end company formation, verification support, and banking advisory to help Bangladeshi applicants meet UK compliance requirements.

Frequently Asked Questions

Can I register a UK company from Bangladesh?

Yes, Bangladeshi residents can register a UK company remotely. From My Company supports applicants in Bangladesh with full compliance, document verification, and PSC registration for UK company formation.

What documents do I need to form a UK company from Bangladesh?

You need a certified passport copy, proof of address (utility bill or bank statement), and a signed Memorandum of Association. From My Company guides Bangladesh applicants through certified document submission and UK Companies House filing.

Will a UK bank accept a company director based in Bangladesh?

Many UK banks require a UK-resident director, but specialist and fintech banks accept non-UK residents after enhanced AML checks. From My Company helps Bangladesh-based directors open business accounts with compliant providers that welcome international applicants.

Do I need to pay UK tax if I run a UK company from Bangladesh?

The UK company pays UK corporation tax on its taxable profits. As a Bangladeshi resident, you pay UK personal tax only on UK-source income or if you become UK tax-resident under the Statutory Residence Test.

How long does UK company formation take for applicants in Bangladesh?

Standard processing takes 24–48 hours once verified documents are submitted, but AML and banking onboarding can add 2–12 weeks. From My Company streamlines verification for Bangladesh applicants to reduce delays and improve approval odds.