A company limited by guarantee differs fundamentally from a limited company (Ltd) as it has no shares or shareholders, with members instead guaranteeing a nominal sum like £1 upon insolvency, suiting non-profits such as charities and clubs. In contrast, a limited company issues shares to shareholders who own the business and receive dividends from profits, ideal for profit-driven enterprises seeking investment. Choosing between them hinges on your goals—social impact versus commercial growth—each offering limited liability but distinct governance and funding paths under UK law.

Navigating UK business structures requires precision, especially when comparing a company limited by guarantee to a private company limited by shares (Ltd), both registered at Companies House yet tailored for divergent purposes. The former thrives in non-profit realms like associations, sports clubs, and mission-driven organisations where profits reinvest into objectives rather than distribute as dividends. Limited companies, however, power most startups and SMEs, enabling equity raises, dividend payouts, and scalable growth. As experts at Form My Company, we’ve assisted thousands through company formation, witnessing how misalignment leads to costly restructures or compliance headaches.

This in-depth analysis unpacks their mechanics, drawing from the Companies Act 2006, to equip entrepreneurs with actionable insights. Semantic factors like directors’ duties, shareholders’ rights, VAT thresholds, PAYE obligations, and registered office requirements shape decisions amid evolving HMRC scrutiny. Real-world examples—think Oxfam (guarantee) versus a tech startup Ltd—illustrate implications for funding, tax, and exit strategies. Whether launching a community trust or e-commerce venture, understanding these structures ensures compliance from day one, safeguarding your vision while optimising for grants, investors, or tax reliefs.

Step-by-Step Explanation: Core Differences Between Structures

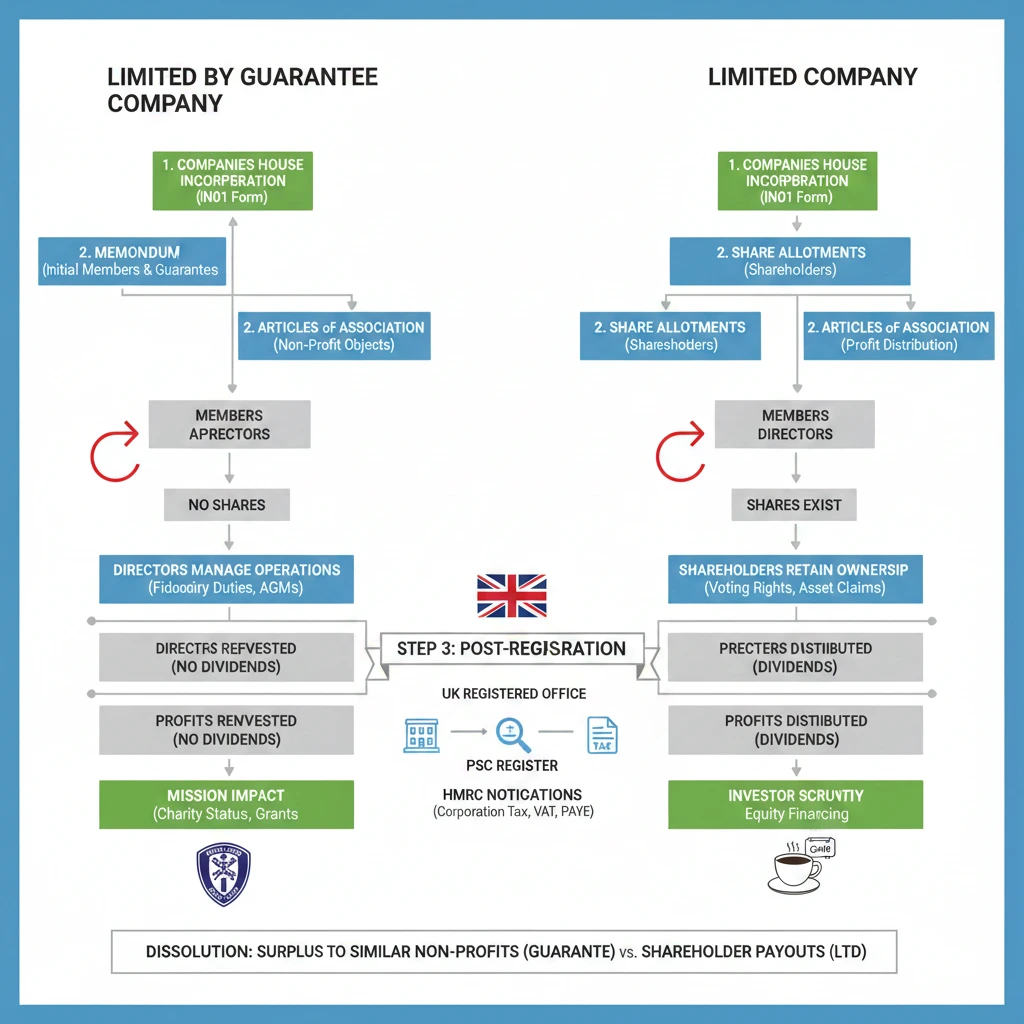

Both structures begin with Companies House incorporation via the IN01 form, but diverge immediately in documentation and ownership. For a limited by guarantee company, drafters submit a memorandum listing initial members and their guarantee amounts (e.g., £1 each), paired with articles of association defining non-profit objects like “advancing public education.” No shares exist; members appoint directors, who manage operations with fiduciary duties to pursue objectives, holding AGMs for oversight. Profits reinvest—no dividends allowed—making it unfit for investor-backed firms.

Conversely, forming a limited company involves share allotments to shareholders upon incorporation, with articles permitting profit distribution via dividends post-tax. Shareholders elect directors but retain ownership rights, including voting on major decisions and residual claims on assets in liquidation. Step three: post-registration, both need a UK registered office (virtual addresses work seamlessly), PSC register if applicable, and HMRC notifications for Corporation Tax, VAT (over £90,000 turnover), and PAYE for employees.

Operationally, guarantee companies file adapted accounts emphasising mission impact, often pursuing Charity Commission status for exemptions. Ltds submit profit/loss statements, enabling investor scrutiny. Example: a guarantee company sports club uses membership fees for facilities; an Ltd café pays shareholder dividends after covering costs. This foundational split influences everything from fundraising (grants vs equity) to dissolution (surplus to similar non-profits vs shareholder payouts).

Benefits and Potential Risks of Each Structure

Limited by guarantee companies excel in liability protection without equity dilution—members cap exposure at nominal guarantees, attracting volunteer directors wary of personal risk. Benefits include tax reliefs (e.g., Gift Aid if charitable), grant eligibility from bodies like Sport England, and public credibility for tenders. No shareholder disputes simplify governance for clubs, while flexibility in articles allows custom rules like quorate voting.

Limited companies shine commercially: shares facilitate angel investment, venture capital, or crowdfunding, with dividends incentivising growth. Entrepreneurs scale rapidly, selling shares for exits. Both shield personal assets, but Ltds offer R&D tax credits unavailable to pure non-profits.

Risks temper advantages. Guarantee companies can’t issue shares, hobbling equity funding; insolvency triggers member contributions, though rare. Directors risk personal liability for breaches, and VAT partial exemption complicates trading charities. Ltds face shareholder activism, dividend pressure straining cashflow, and higher audit thresholds. Example: a guarantee company housing association thrives on grants but struggles with debt; an Ltd retailer accesses loans but navigates investor returns. Weigh these against your model—Form My Company tailors setups to maximise upsides.

Legal and Compliance Considerations

Under the Companies Act 2006, both demand annual confirmation statements, accounts filing, and director notifications within 14 days. Guarantee companies adapt Model Articles for non-profits, prohibiting private benefits; Ltds use standard articles enabling dividends. Registered office mandates a physical UK address for statutory mail—virtual services from Form My Company ensure privacy.

Tax compliance diverges: both register for Corporation Tax, but guarantee entities claim trading reliefs; Ltds deduct dividends pre-tax. VAT registration at £90,000 applies identically, with reclaim nuances for non-profits. PAYE kicks in for payroll, requiring RTI submissions. Charity overlaps demand dual Charity Commission filings for guarantee companies, escalating scrutiny.

PSCs must disclose controllers; audits trigger at £10.2m turnover for Ltds or £632k for guarantee entities. GDPR binds member/shareholder data. Breaches invite fines (£5,000+), strikes-off, or disqualifications. Practical edge: Ltds suit B Corp hybrids; guarantee fits mutuals. Proactive compliance via Form My Company’s packages averts pitfalls like late PSC updates, seen in recent HMRC crackdowns.

Common Mistakes to Avoid When Choosing Between Them

Misaligning purpose tops errors—selecting guarantee for profit-making ventures blocks dividends, forcing restructures costing £1,000+. Vague objects in guarantee articles invite Companies House rejections; Ltds falter on share class oversights, sparking disputes. Neglecting VAT/PAYE from launch burdens startups—guarantee clubs overlook trading exemptions, inflating costs.

Both suffer dormant filing lapses leading to dissolution. Guarantee setups skip dissolution clauses, risking asset fights; Ltds ignore pre-emption rights, alienating investors. Rushing solo incorporation omits bespoke articles—professionals prevent this. Example: a startup chose guarantee expecting tax perks, pivoting painfully to Ltd. Audit miscalculations hit growing Ltds. Solution: assess via Form My Company’s free consultations, ensuring Companies House-compliant formation.

Practical Tips and Best Practices

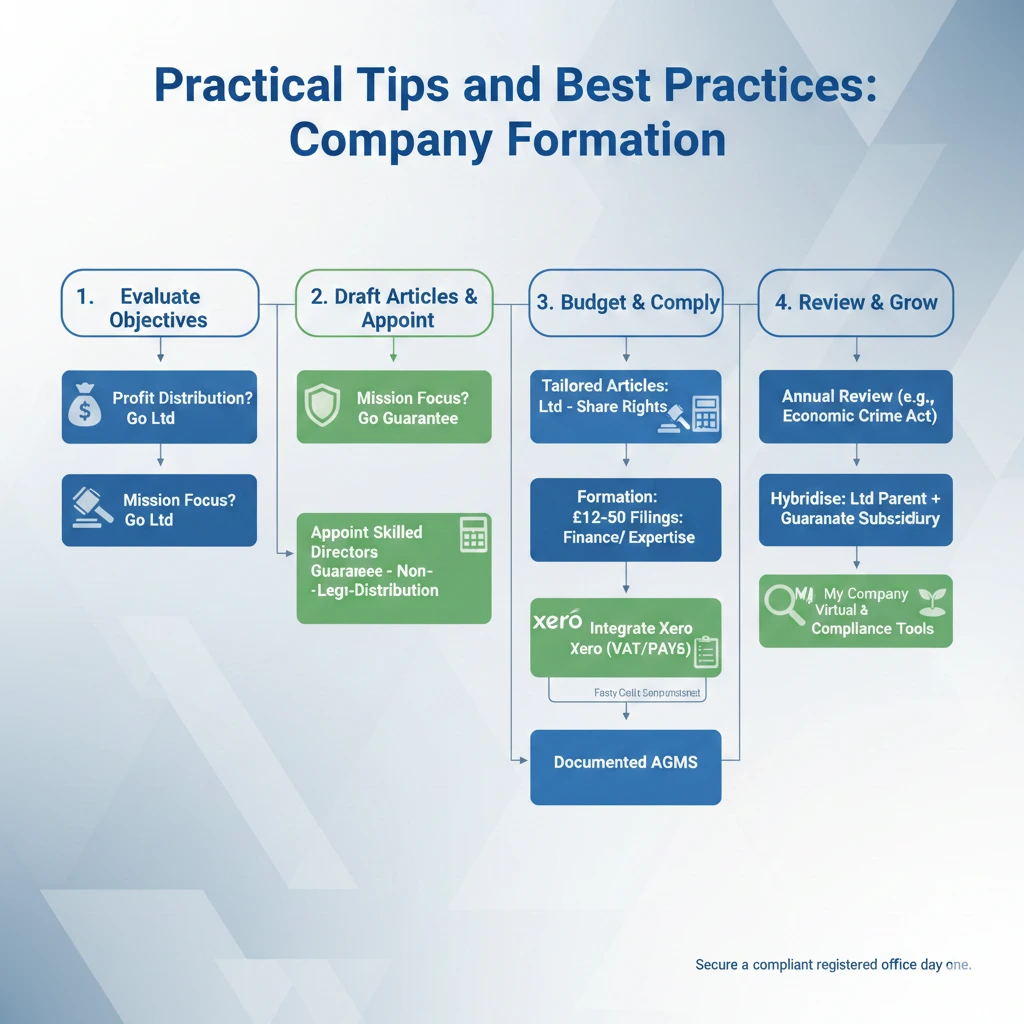

Evaluate objectives first: profit distribution? Go Ltd. Mission focus? Guarantee. Draft tailored articles—guarantee specifies non-distribution; Ltd details share rights. Appoint skilled directors early, blending finance/legal expertise. Secure a compliant registered office day one for credibility.

Budget compliance: £12-50 formation, £100+ yearly filings. Integrate Xero for VAT/PAYE. Hold documented AGMs. For Ltds, use EMI schemes for staff shares; guarantee leverages memberships. Review annually amid law changes like Economic Crime Act. Hybridise: Ltd parent with guarantee subsidiary. Form My Company’s virtual office and compliance tools streamline this.

FAQs

When should I choose limited by guarantee over Ltd?

Opt for guarantee if non-profit, e.g., charities needing grants without dividends. Ltd suits trading with investors seeking returns.

Do both have shareholders?

No—guarantee uses members/guarantors; Ltd has shareholders owning via shares. Both limit liability.

What about taxes and VAT for each?

Identical Corporation Tax/VAT rules apply; guarantee accesses charity reliefs. PAYE same for employees.

Can I convert between structures?

Yes, via special resolution and Companies House re-registration, but costly—plan ahead.

How many directors are required?

At least one for both; guarantee often needs more for governance.

Company limited by guarantee prioritises mission with capped liability sans shares; limited companies fuel profit via equity. Selecting right hinges on funding, tax, compliance—both excel with proper setup.

If you’re ready to register your company with confidence, Form My Company provides fast, fully online company formation with expert compliance support, VAT & PAYE setup, virtual office solutions, and professional guidance. Get started today and let our specialists handle the paperwork while you focus on growing your business.