UK limited companies offer significant tax advantages over sole traders, including 19–25% corporation tax on profits, tax-efficient salary/dividend mixes, full expensing for capital investments, and R&D tax reliefs reclaiming up to 27% of qualifying spend. These benefits make limited companies ideal for businesses with profits over £50,000 annually, enabling reinvestment and growth while minimising overall tax liability. Dividends face lower effective rates (8.75–39.35%) without National Insurance, unlike sole trader income tax (20–45%) plus NI contributions.

Registering a UK limited company through Companies House unlocks a sophisticated tax framework designed to incentivise business investment, innovation and scalability—benefits unavailable to sole traders or partnerships. Under the Corporation Tax Act 2010 and ongoing reforms, directors can strategically extract profits via low-tax dividends after paying competitive corporation tax, while claiming generous allowances for assets, R&D and pensions. Semantic searches like “UK limited company tax benefits 2026,” “corporation tax savings vs sole trader,” and “dividend allowance limited company” reflect entrepreneur interest as thresholds stabilise and new reliefs emerge.

With 2026 bringing a 40% first-year allowance for main rate assets (excluding full expensing qualifiers) and stable 25% main corporation tax rate, limited structures shine for trading entities. Unlike sole traders facing Making Tax Digital quarterly reporting and higher marginal rates, limited companies separate business tax from personal, shielding shareholders via limited liability. This guide details reliefs, calculations, compliance and pitfalls, empowering founders to optimise take-home pay—e.g., a £80k profit Ltd saves £2,500+ annually versus sole trader per HMRC models.

Step-by-Step: How Limited Company Tax Benefits Work

UK limited company taxation begins post-incorporation via HMRC registration (unique CT UTR within 3 months trading). Profits face corporation tax: 19% on £0–£50k (small profits rate), marginal relief to 25% at £250k+, divided by associated companies. Example: £60k profit yields £11,400 tax (19% effective), leaving £48,600 for salary/dividends.

Optimal extraction: Pay director’s salary to £12,570 personal allowance (0% tax/NI), then dividends—£500 allowance (2026), basic rate 8.75% to £37,700, higher 33.75%. No NI on dividends saves 9%+ versus sole trader Class 4. Reinvest pre-tax via full expensing (100% deduction new plant/machinery) or 2026’s 40% FYA for leasers/unincorporated exclusions.

R&D relief: SMEs claim 186% super-deduction (effective 33% tax saving) or 27% cash credit if loss-making. File i024 with CT600. VAT (£90k threshold) allows input reclaims. PAYE operates for employees/directors. A £100k profit company extracts £65k post-tax optimally, versus £58k sole trader—benefits compound with growth.

Key Tax Benefits and Their Impact on Growth

Corporation tax at 19–25% undercuts sole trader’s 40–47% top marginal (income tax + NI), enabling retention for reinvestment. Full expensing deducts 100% qualifying capex immediately—e.g., £50k machinery saves £12.5k tax at 25%, boosting cashflow versus depreciating pools. From 1 Jan 2026, 40% FYA aids leasers/hire firms previously excluded, per Deloitte TaxScape.

Dividends optimise: post-CT, basic rate shareholders pay 8.75% (total effective ~26%) versus 32% sole trader NI-inclusive. Pension contributions deduct fully—e.g., £10k saves £2.5k CT, grows tax-free. R&D: enhanced deductions or 14.5% SME credit (27% cash if unprofitable), fuelling tech/services. SEIS/EIS attract investors with 50–30% reliefs. Implications: £70k profit Ltd director takes £45k (salary £12k + dividends £33k) post-tax, sole trader £41k—£4k saved reinvests.

Trading allowance absent, but losses carry forward indefinitely against future profits.

Potential Risks and Mitigation Strategies

Lower headline rates belie risks: IR35 off-payroll rules tax “disguised employment” at income tax/NI if control suggests employee status—mitigate via PSC contracts. Late CT600 filings incur £100+ penalties escalating daily. Dividend mismatches (higher rate without planning) erode savings. Associated companies inflate thresholds (e.g., 2 firms halve £50k limit).

VAT registration (£90k) mandates quarterly returns, though reclaims offset sales tax. PAYE errors for salaries trigger HMRC deductions. 2026 transfer pricing/DPT repeal tightens multinationals. Mitigate: optimal salary £12,570, track marginal relief, use accountants (£500–£1k/year). Risks manageable; unmitigated, fines exceed savings.

Legal and Compliance Requirements for Tax Optimisation

Directors must file CT600 annually (12 months post-period), confirmation statements (£34), accounts per size (micro-entity <£632k turnover). PSC register discloses >25% control. Corporation tax self-assessed; HMRC enquiries probe extractions (salary too low flags “settlements”). PAYE RTI submits real-time for salaries/NI. VAT via Making Tax Digital quarterly from scratch.

Companies Act 2006 binds fiduciary duties—tax planning legitimate if commercial. 2026 ID verification mandatory for directors. Non-compliance dissolves firms. EEAT compliance demands accurate SIC, registered office filings. Form My Company streamlines VAT/PAYE setup alongside Companies House.

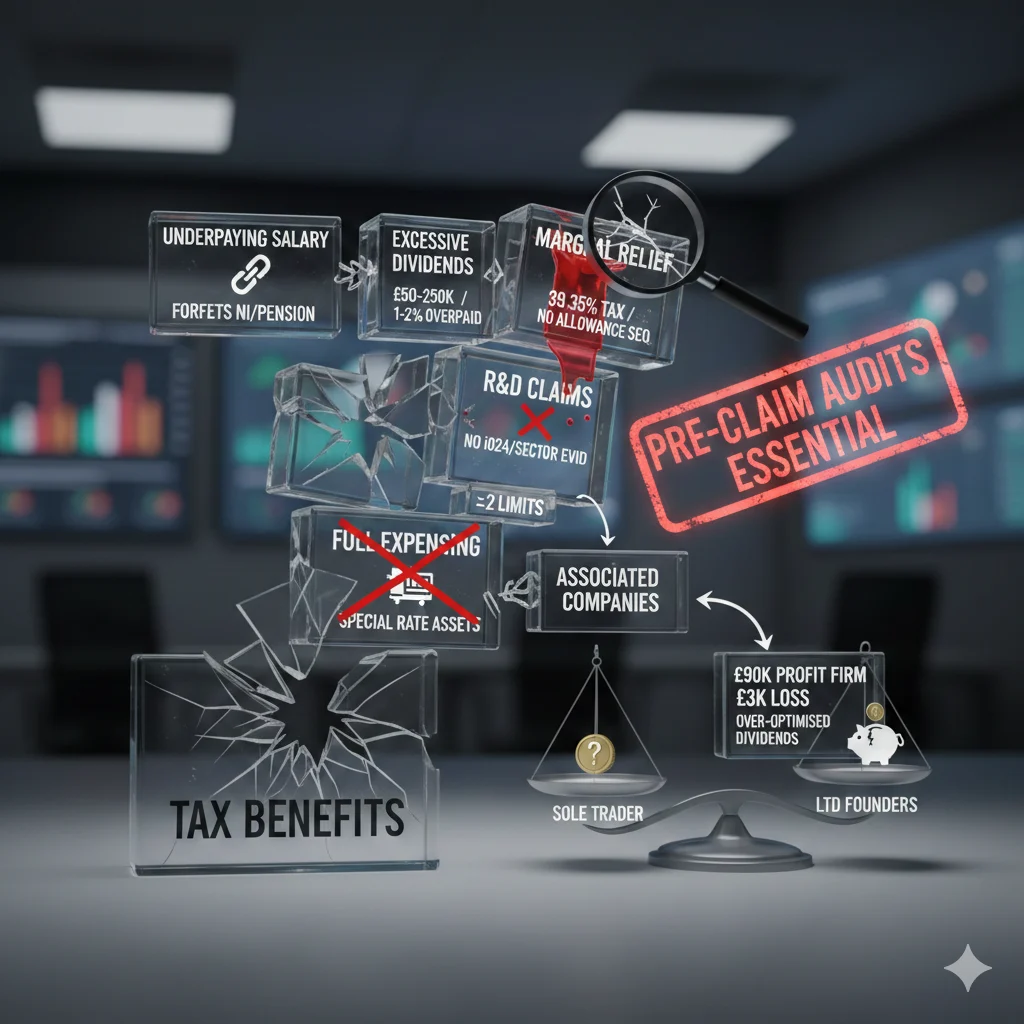

Common Mistakes Limiting Tax Benefits

Underpaying salary forfeits NI credits/state pension—minimum £12,570. Excessive dividends hit 39.35% without allowance sequencing. Ignoring marginal relief at £50–250k overpays 1–2%. R&D claims without i024/sector evidence rejected. Full expensing misapplication (special rate assets ineligible). Associated companies undisclosed halve limits.

Sole trader comparisons ignore NI; Ltd founders skip pensions. A £90k profit firm loses £3k over-optimising dividends. Pre-claim audits essential.

Practical Tips and Best Practices for Maximisation

Model scenarios: £12k salary + remainder dividends; claim FYAs promptly. Integrate Xero for CT/VAT/PAYE. Quarterly R&D logs. Pension max £60k/year tax-free. EORI for exports reclaims. Annual tax reviews adjust Budget changes (stable 2026 rates). SEIS roadshows fundraise. Outsource compliance scales benefits.

FAQs: UK Limited Company Tax Benefits

How much tax does a limited company pay on £100k profits?

~£19k CT (19–25% blended), extract £65k+ via salary/dividends vs £55k sole trader.

What is full expensing?

100% deduction new plant/machinery year 1, saving up to 25p/£1 invested.

Do dividends avoid NI?

Yes—no employee/employer NI, just dividend tax post-CT.

R&D relief for small companies?

186% deduction or 14.5% credit (27% cash if loss-making).

When to register for VAT?

Mandatory £90k turnover; voluntary below reclaims inputs.

UK limited company tax benefits—CT efficiency, dividends, reliefs—drive profitability when optimised.

If you’re ready to register your company with confidence, Form My Company provides fast, fully online company formation with expert compliance support. Get started today and let our specialists handle the paperwork while you focus on growing your business.