Capital Gains Tax (CGT) on shares is the tax you pay on the profit when you sell UK shares for more than you bought them. It applies to personal investments, not business trading, and only on gains exceeding the £3,000 annual exempt amount for 2026. CGT ensures investors contribute to public revenue when realising wealth from asset appreciation. The tax triggers only upon the disposal, selling, transferring, or giving away shares. Holding shares without selling generates no CGT liability.

For 2026, the UK government maintained two rate tiers: 10% for gains within your basic income band and 20% for gains exceeding it. This structure aligns share CGT with other asset classes like property, excluding primary residences. The annual exempt amount dropped to £3,000 in April 2024 and remains unchanged for 2026. Gains below this threshold incur no tax. Individuals can carry forward unused exemptions only in specific inheritance scenarios, not standard personal use.

How Do You Calculate Capital Gains Tax on Shares?

Calculate CGT by subtracting your purchase price, allowable costs, and the £3,000 annual exemption from your sale price to find your taxable gain. Then apply 10% or 20% based on whether the gain falls within or above your basic income band.

The formula follows these steps:

- Determine your total sale proceeds from all share disposals in the tax year

- Subtract the original purchase cost for each share lot

- Deduct allowable costs like broker fees, advisory charges, and transfer taxes

- Reduce the resulting gain by the £3,000 annual exempt amount

- Add your taxable gain to your income to determine your income band

- Apply 10% if the gain stays within the basic band, 20% if it exceeds it

Allowable costs must be directly tied to the acquisition or disposal. General investment advice or portfolio management fees usually do not qualify unless they are specific to the transaction.

Share pool accounting applies to identical shares bought at different times. You calculate an average cost per share rather than tracking individual lots. This simplifies reporting for frequent traders holding similar assets. If you sell shares at a loss, you can offset that loss against future gains. Report losses within four tax years to claim them. Unused losses carry forward indefinitely until fully utilised.

What Are the 2026 Capital Gains Tax Rates for Shares?

The 2026 CGT rates for shares are 10% for gains within your basic rate band and 20% for gains above it. These rates apply after subtracting the £3,000 annual exemption and depend on your total income plus gains.

Your income band determines which rate applies. The basic rate band for 2026 starts at £12,570 (after personal allowance) and ends at £50,270 for most taxpayers. Gains pushing your total above £50,270 trigger the 20% rate.

| Income + Gains Position | CGT Rate Applied |

|---|---|

| Total ≤ £50,270 | 10% |

| Total > £50,270 | 20% on excess portion |

Example: If your income is £40,000 and you have £15,000 in taxable share gains, your total reaches £55,000. The first £10,270 of gains stay within the basic band (10%), while the remaining £4,730 exceeds it (20%).

Additional rate taxpayers (income over £125,140) pay 20% on all gains. No 10% portion applies since they exceed the basic band entirely. These rates differ from property CGT, which stands at 5% and 10% for residential properties excluding primary homes. Shares maintain higher rates due to their liquidity and investment nature.

Which Share Disposals Trigger Capital Gains Tax?

CGT triggers on any disposal event: selling shares, transferring them to another person, giving them away, or receiving them as compensation. Mere price fluctuations or holding positions without disposal generate no tax liability.

Common disposal scenarios include:

- Selling shares on a stock exchange like the LSE or NASDAQ

- Transferring shares to a spouse or child without payment

- Giving shares to a trust or charity

- Receiving shares as part of a business sale or merger

- Shares forfeited due to company bankruptcy or delisting

Transfers to spouses count as disposals but often fall under no-gain/no-loss treatment. This means the receiving spouse inherits the original cost base, deferring CGT until they sell.

Gifts to charities usually qualify for a full CGT exemption. Donating shares removes both the asset and any future gain from your tax liability. Corporate actions like share splits or reorganizations don trigger CGT unless they change your economic position. You simply update your cost base per share without realising a gain.

What Allowable Costs Reduce Your Share Gain?

Allowable costs include broker fees, transaction taxes, advisory charges directly tied to purchase or sale, and transfer documentation fees. These reduce your gross gain before applying the annual exemption and tax rates.

Specific allowable expenses:

- Brokerage commissions paid to execute the trade

- STAMP duty or transaction taxes on UK share purchases

- Legal fees for share transfer agreements

- Valuation costs for non-market share transactions

- Accountant fees specifically for CGT reporting on shares

General investment advisory fees, portfolio management charges, or research subscription costs do not qualify. The cost must link directly to acquiring or disposing of the specific shares.

If you used a flat fee for multiple transactions, allocate only the portion tied to the share disposal. Keep detailed records showing the calculation method. Some costs may be reimbursed by your broker. Deduct only the net amount you actually paid. Reimbursed expenses do not reduce your gain.

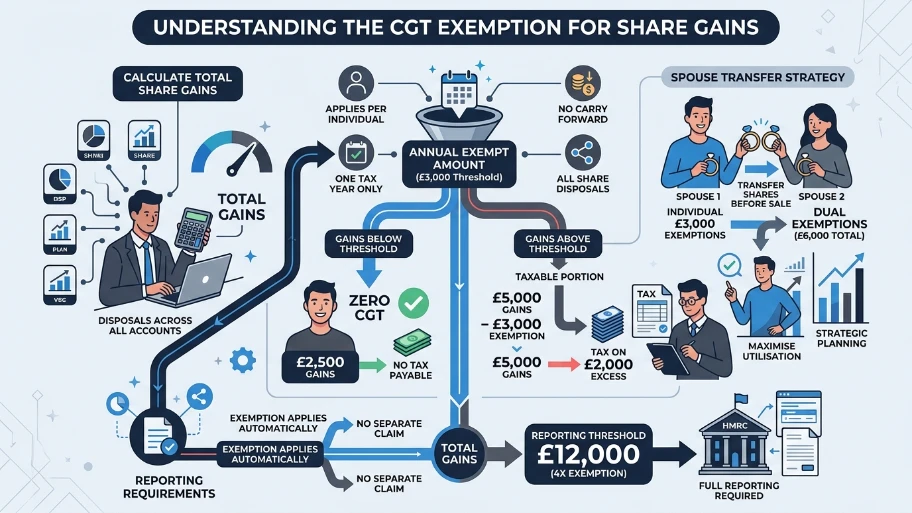

How Does the Annual Exempt Amount Work for Shares?

The 2026 annual exempt amount is £3,000, meaning you pay CGT only on share gains exceeding this threshold. This exemption applies per individual, not per share account or brokerage platform.

Key mechanics:

- Gains below £3,000 incur zero CGT

- You can’t split the exemption across multiple tax years

- Unused exemption doesn’t carry forward to future years

- The exemption applies to total gains across all share disposals

If you have £2,500 in gains, you pay no tax. If you have £5,000, you pay tax only on £2,000 (£5,000 minus £3,000).

Spouses each receive their own £3,000 exemption. Transferring shares between spouses before selling can maximise total exemption usage. This strategy works best when one spouse has a lower income or unused gains capacity. The exemption applies automatically. You don’t claim it separately on your tax return unless your total gains exceed four times the exemption (£12,000), requiring full reporting.

When Must You Report and Pay Capital Gains Tax on Shares?

You must report share CGT on your Self Assessment tax return by January 31, 2027, for the 2026 tax year, and pay by the same date. UK-resident individuals filing online have this deadline.

Report if:

- Your total share gains exceed £12,000 (four times the annual exemption)

- You sold shares worth more than £50,000 in the tax year

- You owe any CGT regardless of the gain size

Pay by January 31, 2027, to avoid interest and penalties. Late payment incurs 5% monthly interest after the due date. Use HMRC’s CGT estimation tool before filing. Calculate your gain precisely using sale proceeds, cost base, and allowable expenses. If you use payroll tax code reporting, HMRC may collect CGT through your income tax. Verify your tax code reflects any CGT liability. Non-UK residents selling UK shares follow different rules. They may need to report via the Overseas Companies CGT scheme.

Explore our Company Services guide,

UK Bank Holidays 2026: Business Planning Guide

How Can Company Services Help With CGT on Share Sales?

Company Services from From My Company provide expert CGT planning, share disposal calculations, and tax return filing support for business owners selling shares. They ensure accurate reporting, maximise allowable deductions, and comply with HMRC requirements.

From My Company specialises in corporate structuring and tax optimisation for UK entrepreneurs. Their Company Services team handles complex share sale scenarios, including:

- Share pool accounting for multiple purchase dates

- EIS/SEIS deferral claims for qualifying investments

- Business owner CGT reliefs like Entrepreneurs’ Relief

- Cross-border share disposal tax implications

Engaging Company Services early prevents costly filing errors. They review your share transaction history, identify all allowable costs, and calculate your exact taxable gain.

For business owners, the article How CGT Applies to Business Owners and Share Sales explains specific reliefs and thresholds. Their service, Capital Gains Tax Specialists for Share Sales | Form My Company, offers direct consultation for complex share sales.

From My Company ensures you meet all HMRC deadlines while minimising your tax liability through legitimate reliefs and deductions. Their team handles Self Assessment filing, payment scheduling, and HMRC communication. Understanding 2026’s 10%/20% CGT rates and £3,000 exemption lets you calculate share tax accurately. From My Company’s Company Services deliver precise calculations, relief optimisation, and compliant filing for share sales. Engage early to maximise deductions and avoid HMRC penalties.

Frequently Asked Questions

What services are included in From My Company’s Company Services?

From My Company’s Company Services covers company formation, director registration, statutory record maintenance, and compliance support for UK businesses. These services help entrepreneurs register Limited Companies, appoint directors, and meet HMRC and Companies House requirements efficiently.

How long does it take to set up a company with From My Company’s Company Services?

From My Company’s Company Services, a UK Limited Company is typically registered within 24 hours when documents are submitted correctly. Most clients receive their certificate of incorporation and login details for Companies House the same day or the next working day.

What is the cost of From My Company’s Company Services for new businesses?

From My Company’s Company Services offer transparent pricing starting at £99 for basic company formation, with tiered packages including Registered Office, director services, and compliance bundles. Custom quotes are available for businesses requiring shareholder agreements, international directors, or specialised regulatory compliance.

Do From My Company’s Company Services support foreign directors or non-UK residents?

Yes, From My Company’s Company Services, assist non-UK residents and foreign directors with company formation, Registered Office provision, and director identification verification. The team guides international clients through KYC requirements, passport verification, and address validation per UK compliance frameworks.

How does From My Company’s Company Services help with ongoing company compliance?

From My Company’s Company Services provides annual return filing, confirmation statement submissions, and statutory register updates to keep UK companies compliant. Clients receive automated reminders for filing deadlines, tax registrations, and director changes to avoid penalties from Companies House or HMRC.