Directors and shareholders can reduce tax liability by structuring income across salary, dividends, and allowances, while utilising thresholds such as the Personal Allowance (£12,570), Dividend Allowance (£500), and basic rate band (£37,700) to maximise net income and maintain compliance with UK tax regulations.

How do tax thresholds impact director and shareholder income planning?

Tax thresholds define how income is taxed across bands, allowing directors and shareholders to split earnings efficiently between salary and dividends to minimise tax exposure while remaining compliant with HMRC rules.

Tax thresholds directly influence how business owners extract profits. In the UK, three main thresholds shape income planning: the Personal Allowance (£12,570), the basic rate band (£37,700), and dividend tax rates starting at 8.75%. Directors often combine a low salary with dividends. A salary set near the National Insurance threshold (£9,100 for employers in 2026) ensures state benefits without triggering excess tax. Dividends were then utilised from the remaining allowances.

When income crosses thresholds, tax rates increase sharply. Dividend tax jumps from 8.75% to 33.75% once income exceeds the basic rate band. This makes precise income allocation critical. Tax thresholds also interact with corporation tax. Companies pay between 19% and 25%, depending on profits. Directors must calculate whether retaining profits or distributing dividends produces better outcomes.

What is the optimal salary and dividend split for tax efficiency?

The most tax-efficient strategy sets a director’s salary between £9,100 and £12,570, then distributes remaining profits as dividends within the basic rate band to minimise income tax and National Insurance contributions.

A low salary reduces both employer and employee National Insurance contributions. Setting salary at £9,100 avoids employer NIC while still qualifying for state pension credits. Increasing salary to £12,570 uses the full Personal Allowance. This works when the company can absorb the additional NIC cost or when corporation tax relief offsets it.

Dividends then fill the remaining income space. The first £500 falls under the Dividend Allowance and is tax-free. Additional dividends within the basic rate band are taxed at 8.75%, which remains significantly lower than PAYE rates. This split works best when total income stays below £50,270. Once income exceeds this threshold, dividend tax increases to 33.75%, reducing efficiency. Directors must calculate total taxable income carefully. This includes salary, dividends, and any other earnings such as rental income or interest.

How can directors maximise the Personal Allowance effectively?

Directors maximise the Personal Allowance by aligning salary to £12,570 and ensuring total taxable income does not exceed £100,000, where the allowance begins to taper and creates an effective 60% marginal tax rate.

The Personal Allowance reduces taxable income to zero for the first £12,570. Using it fully prevents wasted tax-free income. Problems arise when income exceeds £100,000. For every £2 earned above this level, £1 of allowance is removed. This creates an effective 60% tax rate between £100,000 and £125,140.

Directors can manage this threshold by adjusting dividend timing. For example, deferring £10,000 of dividends into the next tax year can preserve the full allowance. Pension contributions also reduce adjusted net income. A £20,000 pension contribution can bring income below £100,000, restoring the allowance entirely. Business owners reviewing their income strategy often benefit from aligning corporate structure early, such as through a compliant director appointment service that ensures accurate role and tax positioning.

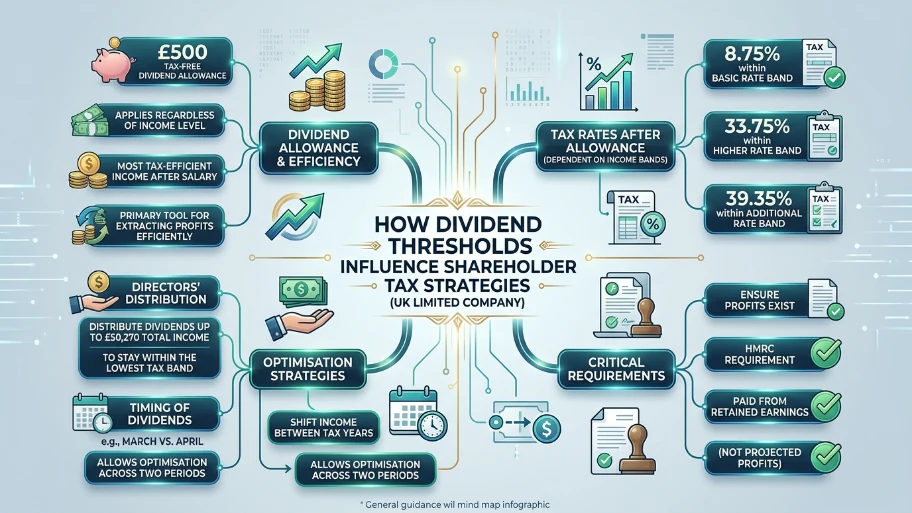

How do dividend thresholds influence shareholder tax strategies?

Dividend thresholds allow shareholders to receive £500 tax-free and then pay lower tax rates within the basic band, making dividends the primary tool for extracting profits efficiently from a UK limited company.

Dividends remain the most tax-efficient income method after salary. The £500 Dividend Allowance applies regardless of income level.

After this allowance, tax rates depend on income bands:

- 8.75% within the basic rate band

- 33.75% within the higher rate band

- 39.35% within the additional rate band

Directors often distribute dividends up to £50,270 in total income to stay within the lowest tax band. Timing plays a key role. Dividends declared in March versus April can shift income between tax years. This allows directors to optimise thresholds across two periods. Shareholders must also ensure profits exist before issuing dividends. HMRC requires dividends to be paid from retained earnings, not projected profits.

What role does corporation tax play in income extraction decisions?

Corporation tax affects how much profit remains available for distribution, requiring directors to balance reinvestment and dividend payouts based on tax rates ranging from 19% to 25%, depending on company profits.

Corporation tax applies before dividends are issued. Companies earning under £50,000 pay 19%, while profits above £250,000 face 25%. This creates a planning decision. Retaining profits allows reinvestment but delays personal income. Distributing profits triggers dividend tax but provides immediate access to funds.

Marginal relief applies between £50,000 and £250,000. This creates a gradual increase in effective tax rates, which must be factored into dividend planning. Directors often extract profits annually to avoid accumulation that pushes the company into higher tax brackets. Business owners evaluating incorporation benefits can explore income structuring strategies in this guide on maximising your income efficiency today by registering a UK company.

How can directors use pension contributions to manage tax thresholds?

Pension contributions reduce taxable income and preserve tax allowances, allowing directors to avoid higher tax bands while building long-term retirement savings in a tax-efficient structure.

Employer pension contributions are deductible business expenses. This reduces corporation tax while avoiding income tax on the director. For example, a £30,000 contribution reduces company profit and lowers corporation tax liability. At the same time, it prevents personal income from exceeding higher-rate thresholds.

Annual pension allowance stands at £60,000 for most individuals. Contributions above this level trigger tax charges. Pensions also help avoid the £100,000 allowance taper. Reducing adjusted income keeps the Personal Allowance intact. This strategy works best for directors with fluctuating income. High-profit years allow larger contributions to offset tax spikes.

When should directors adjust income timing across tax years?

Directors adjust income timing by shifting dividends and bonuses between tax years to stay within lower tax bands and preserve allowances, especially near thresholds like £50,270 and £100,000.

Income timing creates flexibility unavailable to salaried employees. Directors control when dividends are declared and paid. Declaring dividends in early April instead of late March shifts income into a new tax year. This resets allowances and tax bands.

This strategy is effective when income is close to key thresholds. For example:

- £48,000 income allows only £2,270 of dividends before entering higher-rate tax

- Deferring £5,000 to the next year avoids the 33.75% rate entirely

Directors must document dividend decisions properly. Board minutes and dividend vouchers validate compliance with HMRC requirements. Using structured services, such as Director Appointment, ensures governance records align with tax planning decisions.

How does the company structure affect tax threshold strategies?

Company structure determines how income flows to directors and shareholders, influencing eligibility for dividends, tax planning flexibility, and compliance with HMRC rules on profit distribution and director responsibilities.

A limited company provides separation between personal and business income. This allows directors to control how profits are extracted. Sole traders lack this flexibility. All profits are taxed as personal income, often pushing earnings into higher tax bands. Adding shareholders allows income splitting. For example, issuing shares to a spouse enables dividend distribution across two Personal Allowances and basic rate bands.

However, HMRC enforces rules such as the settlements legislation. Share allocations must reflect genuine ownership and rights. Proper structuring begins at incorporation or when roles change. Services like director appointment support accurate registration and compliance with Companies House requirements, ensuring tax strategies remain valid.

Explore our Director Appointment service guides,

Purchase Our Director Appointment Bundle to Successfully Manage All Your Board Changes

Sign Up Now for Expert Director Appointment Assistance and Professional Record Management

How can directors ensure compliance while optimising tax thresholds?

Directors ensure compliance by maintaining accurate records, issuing dividends from retained profits, filing returns on time, and aligning income strategies with HMRC regulations to avoid penalties and audits.

Tax efficiency must align with legal compliance. HMRC actively reviews director income patterns, especially where salary is minimal and dividends are high.

Key compliance actions include:

- Maintain dividend documentation, including vouchers and board minutes

- File self-assessment tax returns by 31 January annually

- Report PAYE income through Real Time Information submissions

- Confirm profits exist before issuing dividends

Errors often occur when directors overdraw from company accounts. This creates director’s loan accounts, which trigger additional tax charges if not repaid within nine months. Working with structured processes ensures that tax planning does not conflict with statutory obligations. For a deeper understanding of how allowances impact planning, review personal tax allowance 2026: what business owners need, and maximise your income efficiency today by registering a UK company.

Tax threshold strategies define how directors and shareholders extract income efficiently while maintaining compliance. Accurate use of allowances, dividend planning, and timing decisions directly impacts net income and tax exposure. From My Company supports structured business decisions through compliant processes such as Director Appointment, ensuring directors are correctly registered and positioned to implement effective tax strategies within UK regulatory frameworks.

Frequently Asked Questions

What is a director appointment and why is it required for a UK company?

A director appointment is the formal process of registering a company director with Companies House, which is legally required for all UK limited companies. From My Company handles this Director Appointment service to ensure compliance with UK corporate governance rules.

How do I appoint a director to my UK limited company?

To appoint a director, you must submit form AP01 to Companies House within 14 days, providing the director’s name, address, and date of birth. From My Company simplifies this Director Appointment process with accurate, fast filing and full regulatory compliance.

What are the eligibility requirements to become a company director in the UK?

A director must be at least 16 years old, not disqualified by a court, and not an undischarged bankrupt. The Director Appointment service from From My Company verifies all eligibility criteria before submission to prevent rejection.

Can a company have more than one director, and is there a maximum limit?

Yes, a UK limited company can have one or more directors, with no legal maximum limit. From My Company supports multiple Director Appointment filings to help businesses scale their leadership team efficiently.

What happens if I fail to register a director appointment on time?

Late registration of a Director Appointment can result in penalties, fines, and potential legal action against the company and its officers. From My Company ensures timely Director Appointment submissions to keep your company compliant and avoid enforcement risks.