The personal tax allowance for 2026–27 remains £12,570 for most UK taxpayers; high-income individuals face a tapered allowance above £100,000 that reduces by £1 for every £2 of income over £100,000. The standard personal allowance is £12,570 for 2026–27; the allowance tapers once taxable income exceeds £100,000, reaching zero at £125,140.

The personal allowance is the amount of taxable income an individual can earn before paying income tax. For 2026–27, the UK government set the standard allowance at £12,570. The allowance is reduced by £1 for every £2 of adjusted net income above £100,000. This taper causes the allowance to fall to zero when adjusted net income reaches £125,140. Employers and payroll software automatically apply the correct allowance when provided with accurate tax codes.

How does the allowance affect directors and business owners?

Directors’ pay personal allowance against salary and benefit income; dividends receive separate tax-free dividend allowance and different rates.

Directors who take a salary from their company use the personal allowance to reduce PAYE liability. Dividend income uses the dividend allowance, currently set by statute, and then taxed at dividend rates. For many small-company directors, a tax-efficient mix is a low taxable salary up to National Insurance thresholds and dividends for residual profits. When adjusted net income exceeds £100,000, directors lose their personal allowance, increasing marginal tax rates and creating a higher effective tax on additional pay.

When does the taper start, and how is it calculated?

The taper starts at £100,000 of adjusted net income and reduces the allowance by £1 for every £2 over that threshold.

Adjusted net income equals total taxable income minus gross pension contributions and certain charitable deductions. For example, a director with £110,000 adjusted net income loses £5,000 of allowance (half of £10,000), reducing their personal allowance to £7,570. The tapering interaction means earning an extra £1,000 in that band can increase tax by more than the basic rate because the individual both pays tax on the extra income and loses part of the allowance.

Read our articles, Maximise Your Income Efficiency Today by registering the UK Company and Tax Threshold Strategies for Directors and Shareholders

How do salary and dividends interact with the allowance for tax planning?

Salary uses the personal allowance first; dividends use the dividend allowance and dividend tax rates thereafter.

Directors commonly pay a salary up to the Primary Threshold or National Insurance Lower Earnings Limit to preserve state benefit records without triggering employer National Insurance. The remaining profit is often distributed as dividends. Because the personal allowance applies to salary first, increasing salary can reduce the allowance available to offset dividends. Careful modelling of salary and dividend mix avoids unexpectedly falling into the allowance taper and higher tax bands.

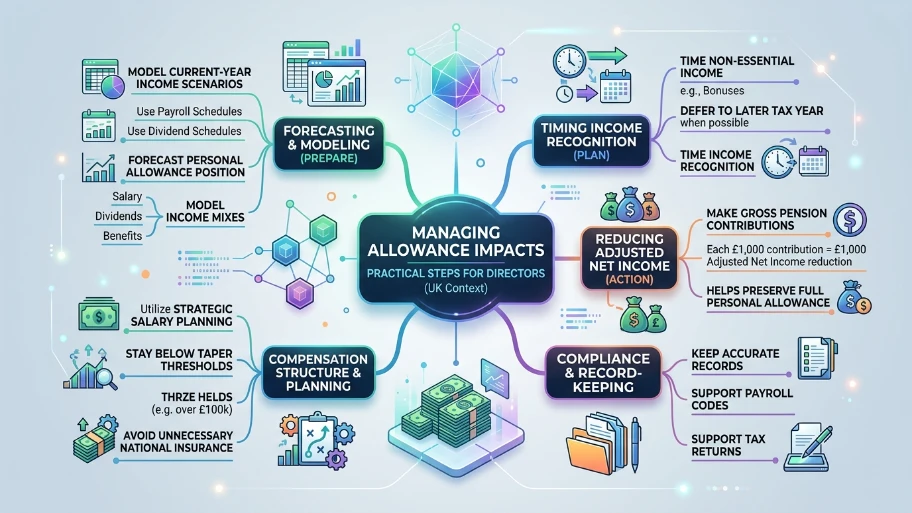

What practical steps can directors take to manage allowance impacts?

Model income mixes, time income recognition, and use pension contributions to reduce adjusted net income.

Model current-year income scenarios using payroll and dividend schedules to forecast allowance position. Time non-essential income to a later tax year when possible. Make gross pension contributions to reduce adjusted net income; each £1,000 contribution reduces adjusted net income by £1,000, helping preserve the full allowance. Use salary planning to avoid paying unnecessary National Insurance while staying below taper thresholds. Keep accurate records to support payroll codes and tax returns.

Can pension contributions restore the lost personal allowance?

Yes. Gross pension contributions reduce adjusted net income and can restore the personal allowance if they bring income below £100,000.

For example, a director with £103,000 adjusted net income who contributes £3,000 gross to a pension can bring adjusted net income to £100,000 and recover the full personal allowance. Use employer pension contributions where possible; these are tax-deductible for the company and reduce the director’s adjusted net income without immediate employee NICs. Confirm annual and lifetime allowance positions and report contributions on the Self Assessment return.

How does the allowance interact with tax bands and effective marginal rates?

Losing the allowance increases the effective marginal tax rate up to 60% for income between £100,000 and £125,140.

When the personal allowance tapers, each extra £1 of income in this band not only attracts income tax but also removes 50p of tax-free allowance, effectively increasing the marginal rate. For example, a basic-rate taxpayer earning additional income in the taper band faces a 40% income tax on that marginal pound plus the loss of allowance, producing an effective marginal rate near 60% depending on circumstances. Directors must consider this when deciding whether to extract additional profit as salary, dividend, or other remuneration.

What reporting or compliance actions must directors take?

Directors must report all income on Self Assessment and ensure payroll codes reflect allowance changes.

Directors paid through PAYE should check their tax code on payslips and confirm the company’s payroll system uses the correct code. For income elements not captured by PAYE, such as dividends or rental income, directors must complete a Self Assessment return. Provide accurate figures for adjusted net income, pension contributions, and gift aid to ensure the correct allowance calculation. HMRC may issue coding notices or corrections when returns show differences.

When should a director consult advisors?

Consult an accountant when adjusted net income approaches £100,000, when planning remuneration changes, or when making large pension contributions.

Accountants can model year-end scenarios, advise on employer versus employee pension contributions, and calculate the tax impact of extracting extra profits. Seek specialist tax advice for complex structures, such as multiple directorships, shareholder loans, or cross-border income. Early engagement avoids late adjustments, errors in payroll, and unexpected tax bills.

Explore our Director Appointment guides,

Why Appointing a Qualified Director Can Improve Your Business Credit Rating Score

Understanding the Link Between Director Appointments and Your Company Articles of Association

What are common mistakes to avoid?

Ignore adjusted net income triggers, mis-time dividends, and under-report pension inputs; all cause higher tax and compliance issues.

Failing to monitor cumulative income across sources leads to surprise taper effects. Paying large dividends without modelling allowance loss creates high marginal tax bills. Not accounting for employer pension payments in payroll and returns can lead to incorrect tax positions. Reconcile company records with personal tax filings to prevent penalties and interest.

Directors must monitor adjusted net income closely in 2026–27 because the standard personal allowance is £12,570 and tapers above £100,000, reaching zero at £125,140. Use precise modelling of salary, dividends, and pension contributions to preserve tax efficiency. From My Company assists directors with compliant appointments and remuneration planning through practical registration and administration. Implementing employer pension contributions and timing dividend distributions reduces the risk of entering the taper zone.

Frequently Asked Questions

How do I appoint a new director to my UK limited company?

To appoint a director, pass a board resolution and file form AP01 with Companies House within 14 days. From My Company handles the Director Appointment process, including identity verification, document preparation, and electronic filing for compliant registration.

What documents are needed for a director’s appointment in the UK?

You need the director’s consent to act, proof of identity, date of birth, usual residential address, and nationality. From My Company’s Director Appointment service collects these details via a secure web form and submits the required AP01 form to Companies House.

How long does it take to appoint a director at Companies House?

Companies House typically processes electronic AP01 filings within 1–2 working days. From My Company files, your Director Appointment is electronically confirmed once the appointment is accepted and updated on the public register.

Can a company have more than one director in the UK?

Yes, a private limited company must have at least one director, and it can have multiple directors. From My Company supports Director Appointment for additional directors to fill vacancies or expand your board while ensuring compliance with the Articles of Association.

What happens if I don’t file a director’s appointment within 14 days?

Late filing of form AP01 can result in penalties and non-compliance notices from Companies House. From My Company’s Director, the Appointment service ensures timely submission within the 14-day legal window to avoid fines and keep your company record accurate.