Making Tax Digital (MTD) is a UK government initiative that requires businesses to keep digital tax records and submit VAT and income tax returns using HMRC-approved software. It replaces manual processes, improves accuracy, and enforces real-time reporting for registered businesses above specific thresholds.

Making Tax Digital is a regulatory framework introduced by HMRC in April 2019 to digitise tax reporting. It mandates digital record-keeping, compatible software usage, and direct submission of tax returns, primarily starting with VAT-registered businesses exceeding the £85,000 threshold.

MTD forms part of HMRC’s strategy to reduce tax gaps. The UK tax gap stood at £36 billion in 2023, with 19% attributed to errors. Digital systems reduce manual entry mistakes and improve compliance accuracy.

MTD requires three core actions. Businesses must maintain digital records, use MTD-compatible software, and submit returns through HMRC’s API. Spreadsheets alone do not qualify unless integrated with bridging software. VAT became the first tax under MTD. Since April 2022, all VAT-registered businesses must comply, regardless of turnover. This change expanded the scope beyond the original £85,000 threshold.

Who Must Comply with Making Tax Digital Requirements?

All VAT-registered businesses in the UK must comply with MTD rules as of April 2022. This includes sole traders, partnerships, and limited companies that submit VAT returns, regardless of turnover or business size.

MTD compliance applies across multiple business structures. Three primary categories include sole traders, limited companies, and partnerships. Each entity must maintain digital VAT records and submit returns via approved software.

Certain exemptions exist. Businesses with digital exclusion, such as those without internet access due to age, disability, or location, can apply for exemption. HMRC reviews these cases individually. Non-compliance triggers penalties. HMRC introduced a points-based penalty system in January 2023. Accumulating four penalty points results in a £200 fine for quarterly VAT filers.

How Does Making Tax Digital Change VAT Reporting?

MTD replaces manual VAT submissions with digital record systems and automated filing processes. Businesses must use compatible software to calculate VAT, store records digitally, and submit returns directly to HMRC without manual re-entry.

Traditional VAT filing relied on manual data entry into HMRC’s portal. MTD eliminates this process. Instead, software integrates directly with HMRC systems, reducing duplication. Digital links are mandatory. Data must flow between systems without manual copying. For example, accounting software connects to spreadsheets using APIs or bridging tools.

MTD also enforces structured data storage. Required VAT records include:

- Business name and VAT number

- VAT accounting schemes used

- Supplies made and received

- VAT rates applied

Businesses improving VAT workflows often use professional support such as VAT Registration Assistance to ensure correct setup and compliance from the outset.

What Software Is Required for MTD Compliance?

MTD requires HMRC-approved software that supports digital record-keeping and direct tax submissions. This includes accounting platforms, bridging tools, and cloud-based systems that integrate with HMRC’s API for secure data exchange.

Over 500 software options are listed on HMRC’s approved vendor list. Common examples include Xero, QuickBooks, and Sage. Each platform provides VAT calculation, submission features, and audit trails.

Three software types dominate MTD compliance:

- Accounting software that manages full financial records

- Bridging software that connects spreadsheets to HMRC

- Enterprise systems for large-scale financial operations

Software selection depends on business size and transaction volume. A company processing 1,000 monthly transactions requires automated reconciliation features, while a freelancer managing 50 transactions benefits from simpler tools.

How Does MTD Affect Small Businesses and Sole Traders?

MTD introduces structured digital processes that standardise tax reporting for small businesses and sole traders. It increases administrative discipline, reduces errors, and requires investment in software and digital accounting practices.

Small businesses often face initial setup challenges. Costs include software subscriptions ranging from £10 to £50 per month and onboarding time for system integration. However, digital systems improve financial visibility. Real-time dashboards show VAT liabilities, cash flow trends, and invoice tracking. This enables faster decision-making.

Sole traders transitioning from manual bookkeeping must adapt quickly. Training and system setup typically take 2–4 weeks, depending on business complexity. For deeper insight into tax implications, explore how MTD impacts VAT and income tax filing to understand compliance across different tax categories.

What Are the Key Benefits of Making Tax Digital?

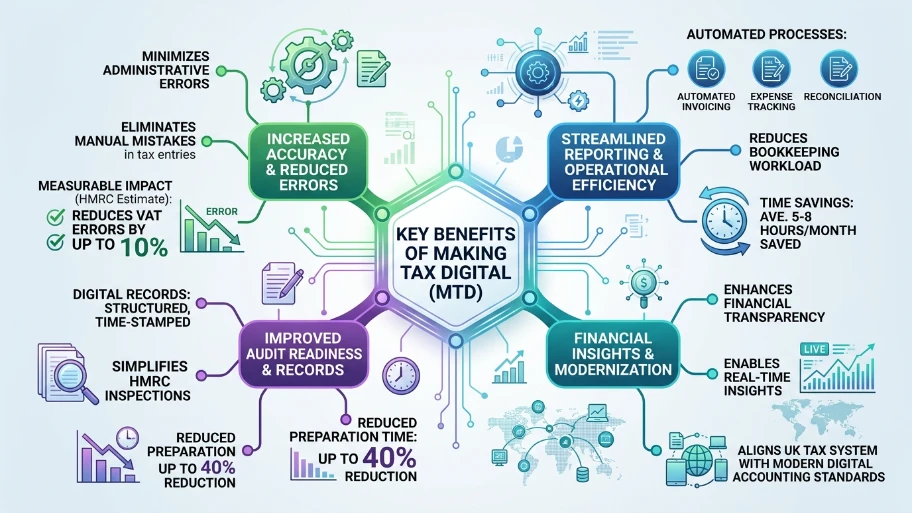

MTD improves tax accuracy, reduces administrative errors, and streamlines reporting through automation. It enhances financial transparency, enables real-time insights, and aligns UK tax systems with modern digital accounting standards.

Error reduction is the most measurable benefit. HMRC estimates that MTD can reduce VAT reporting errors by up to 10%. Automated calculations eliminate manual mistakes in tax entries. Digital records improve audit readiness. Businesses maintain structured, time-stamped records that simplify HMRC inspections. This reduces audit preparation time by up to 40%. MTD also enhances operational efficiency. Automated invoicing, expense tracking, and reconciliation reduce bookkeeping workload. Businesses save an average of 5–8 hours per month.

What Are the Common Challenges with MTD Compliance?

MTD compliance introduces challenges such as software adoption, system integration, and staff training. Businesses transitioning from manual systems face operational disruption and must ensure digital links meet HMRC requirements.

Software compatibility issues arise during migration. Legacy systems often lack API integration, requiring bridging tools or full replacement. Training gaps affect compliance. Staff unfamiliar with digital accounting tools may input incorrect data or fail to maintain proper records.

Cost management is another concern. Initial setup expenses include software licensing, consultant fees, and process restructuring. Businesses that address these challenges early often rely on structured onboarding processes and services like VAT Registration Assistance to ensure compliance alignment.

How Does MTD Impact Future Tax Systems in the UK?

MTD extends beyond VAT and will include income tax and corporation tax in future phases. HMRC plans to create a fully digital tax ecosystem with quarterly reporting and integrated financial data across all tax types.

MTD for Income Tax Self Assessment (ITSA) is scheduled for phased rollout starting April 2026. It applies to sole traders and landlords earning over £50,000 annually. Quarterly updates replace annual submissions. Businesses must report income and expenses every three months, increasing reporting frequency from 1 to 4 submissions per year.

Corporation tax integration is under development. This will impact limited companies by requiring the digital submission of CT600 forms and supporting financial data. These changes signal a long-term shift toward continuous tax reporting. Businesses adopting digital systems early gain operational advantages and compliance readiness.

Explore our VAT Registration Assistance guides,

Why Your Small Business Might Need to Register for VAT This Year

Understanding the Current UK VAT Registration Threshold for Growing Small Businesses

How Can Businesses Prepare for MTD Compliance Effectively?

Businesses prepare for MTD by selecting compliant software, digitising financial records, training staff, and aligning accounting processes with HMRC requirements. Early preparation ensures a seamless transition and avoids penalties.

Preparation begins with system assessment. Businesses must evaluate current accounting methods and identify gaps in digital capability. Next comes software implementation. Choosing HMRC-approved tools ensures compatibility and compliance. Process alignment follows. Businesses standardise workflows such as invoice recording, expense tracking, and VAT calculations within digital systems.

Professional services accelerate this process. Accessing structured support such as VAT Registration Assistance helps businesses register correctly and configure systems in line with HMRC rules. For businesses ready to implement full compliance systems, review stay MTD compliant with Form My Company accounting support to evaluate structured solutions.

Making Tax Digital transforms how UK businesses manage tax reporting by enforcing digital record-keeping and automated submissions. It improves accuracy, reduces errors, and aligns financial processes with modern compliance standards. Businesses that adopt structured systems early gain efficiency and reduce compliance risk. Form My Company delivers practical support through VAT Registration Assistance, enabling accurate setup, system integration, and adherence to HMRC requirements without operational disruption.

Frequently Asked Questions

What is VAT registration assistance in the UK?

VAT Registration Assistance is a service that helps businesses register for VAT with HMRC accurately and efficiently. From My Company provides VAT Registration Assistance by handling eligibility checks, document preparation, and submission to ensure compliance with UK tax regulations.

Who needs VAT registration assistance in the UK?

Businesses exceeding the £90,000 VAT threshold or those opting for voluntary registration benefit from VAT Registration Assistance. From My Company supports sole traders, partnerships, and limited companies in meeting HMRC requirements and avoiding registration errors.

How long does VAT registration take with professional assistance?

VAT registration typically takes 5 to 10 working days when applications are correctly submitted. Using VAT Registration Assistance from My Company helps reduce delays by ensuring all required details and supporting documents are accurate.

What documents are required for VAT registration?

HMRC requires business details such as company registration number, turnover records, bank details, and director identification. VAT Registration Assistance from From My Company ensures all documents are verified and submitted in line with compliance standards.

Can I register for VAT voluntarily before reaching the threshold?

Yes, businesses can voluntarily register for VAT even below the threshold to reclaim input VAT and improve credibility. From My Company offers VAT Registration Assistance to guide businesses through voluntary registration and ensure proper setup with HMRC systems.