MTD changes how VAT and income tax are recorded and submitted: VAT returns must use functionally compatible software and digital links, and sole traders with income above the threshold must send quarterly digital updates to HMRC. MTD for VAT requires businesses with a taxable turnover above £85,000 to keep digital records and submit VAT returns using compatible software.

MTD for VAT applies to any VAT-registered business whose VAT taxable turnover exceeds £85,000 in any 12 months. These businesses must record sales, purchases, and VAT liabilities digitally. They must submit VAT returns to HMRC using functional compatible software that digitally links records and the submission. HMRC permits bridging software for simple spreadsheets if a digital link exists between records and the submission.

Digital record-keeping requires recording distinct data points: VAT-exclusive sales, VAT amounts, VAT-inclusive totals, and the VAT accounting scheme used. Businesses must keep these records for four years and make them available on request. Agents can act for clients using agent credentials and must maintain digital records under the same rules.

How does MTD affect income tax for sole traders and landlords?

MTD for Income Tax (MTD ITSA) phased in for sole traders and landlords with annual gross receipts above £50,000 from April 2026; they must keep digital records and send quarterly updates.

From April 2026, HMRC extended MTD to income tax for unincorporated businesses with gross trading or property income over £50,000. These taxpayers must use compatible software to record transactions and submit quarterly updates summarising income and expenses. At year‑end, they must send an End of Period Statement and a final declaration to confirm taxable profit, replacing the single annual Self Assessment submission process for most reporting items.

Quarterly updates change cash-flow management. Businesses receive more timely tax estimates and must plan for quarterly adjustments. Agents can submit updates on behalf of clients through authorised software. Penalties for late digital submissions follow existing HMRC penalty frameworks adapted for digital filing.

Read our articles, Making Tax Digital Explained for UK Businesses and Stay MTD Compliant with Form My Company Accounting Support

What specific records must businesses keep digitally under MTD?

Businesses must record dates, VAT-exclusive values, VAT amounts, VAT rates, supplier/customer identifiers, and totals in compatible software.

For VAT, required fields include invoice date, value excluding VAT, VAT amount, VAT rate applied, and the VAT accounting scheme. For MTD ITSA, required records include date of transaction, income value, expense value, category of income or expense, and any capital allowances claimed. Each recorded item must be traceable to source documents such as invoices, receipts, or bank statements.

Using compatible software enables digital linking between: sales ledgers, purchase ledgers, receipts, and the submission file. Digital links can be API connections, automated exports, or validated bridging mechanisms. Manual transcription that breaks links is non-compliant.

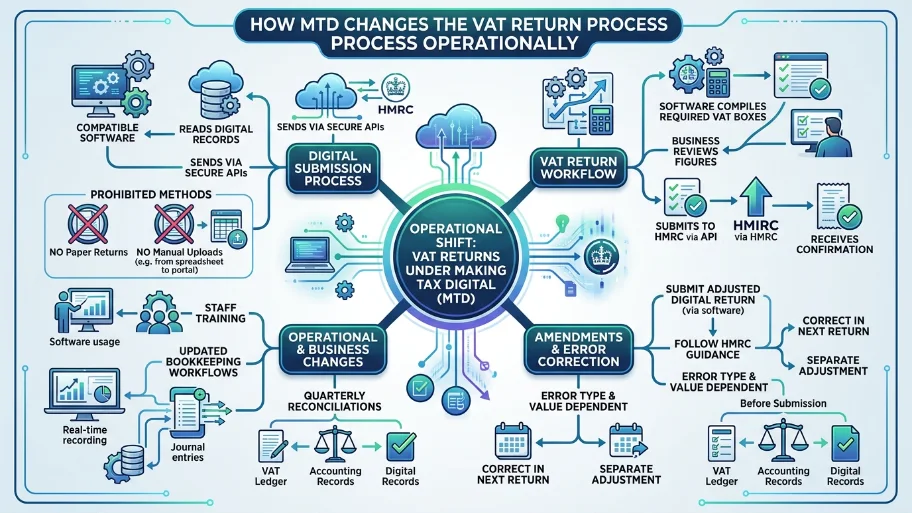

How does MTD change the VAT return process operationally?

Businesses submit VAT returns via compatible software, which reads digital records and sends returns through secure APIs; paper or manual uploads are not permitted.

The software compiles the required VAT return boxes from digital records. Businesses must check computed figures before submission. The software sends the return via HMRC’s API and receives confirmation. Any amendments require submitting an adjusted digital return through the software. Where errors arise, HMRC guidance directs corrections either in the next return or by a separate adjustment, depending on error type and value.

Operational changes include training staff on software usage, updating bookkeeping workflows for real‑time recording, and scheduling quarterly reconciliations to ensure VAT and accounting ledgers match the digital records before submission.

How does MTD affect accounting workflows and cash flow forecasting?

MTD increases the frequency of reporting and the granularity of data, enabling accurate quarterly tax estimates and improved cash-flow forecasting.

Quarterly updates create regular tax visibility. Businesses can forecast VAT and income tax liabilities more accurately. Accountants must integrate bookkeeping with tax software to generate timely reports. This integration reduces surprises at year‑end and allows proactive tax planning, such as timing deductible purchases or making payments on account.

To implement this, businesses typically: adopt compatible software, train users, set monthly reconciliation routines, and run quarterly tax reports. These steps reduce reconciliation errors and support reliable forecasting models.

What are compliance risks and common pitfalls under MTD?

Common risks include broken digital links, incomplete digital records, late submissions, and using incompatible software.

Businesses that export data manually between systems without validated digital links risk non‑compliance. Incomplete capture of required fields leads to incorrect returns. Using unsupported software or unlicensed bridging tools exposes the business to penalties. Agents must ensure they hold digital authorisation and that client data flows correctly between record systems and submission software.

Businesses facing technical issues should document problems and follow HMRC incident procedures. HMRC allows reasonable excuse defences for technical outages if businesses demonstrate they followed the required steps and attempted a timely submission.

How can VAT Registration Assistance from My Company help businesses comply with MTD?

VAT Registration Assistance guides businesses through digital registration, sets up compatible software, and ensures returns align with HMRC’s MTD requirements.

From My Company’s VAT Registration Assistance service registers businesses for VAT, configures bookkeeping systems for MTD compatibility, and maps record fields required for digital linking. The service provides practical steps: verify turnover against the £85,000 threshold, choose compatible software, migrate historic records, and train staff or agents to submit VAT returns via software. The support reduces setup errors and speeds compliance.

Practical example: an owner uses the service to register for VAT, set up an API-linked accounting package, and complete the first digital submission within two weeks, reducing initial compliance friction.

Explore our VAT Registration Assistance guides,

The Benefits of Outsource VAT Registration to Ensure Your Business Stays Compliant

Why Your Growing Business Needs Professional Help with Complex VAT Applications

What steps should a business take now to prepare for MTD compliance?

Assess turnover, choose compatible software, migrate records, and schedule quarterly reporting cycles.

First, verify whether taxable turnover exceeds the VAT threshold of £85,000 or the MTD ITSA threshold of £50,000 for income. Second, select HMRC‑recognised compatible software that supports digital links and API submissions. Third, migrate existing records into the software and reconcile the last 12 months of VAT and accounting data. Fourth, establish quarterly reporting dates, run trial submissions, and train staff or agents on the new workflows.

Action list:

- Verify turnover against thresholds and registration dates.

- Install compatible software and enable API connectivity.

- Migrate invoices, receipts, and ledgers; validate totals.

- Schedule quarterly reconciliations and submission dates.

MTD transforms VAT and income tax reporting into continuous, digitally linked processes. It requires digital record-keeping, compatible software, and quarterly or periodic updates for eligible taxpayers. From My Company helps businesses register for VAT, configure compliant systems, and maintain accurate digital records to meet HMRC requirements.

Frequently Asked Questions

How long does VAT registration take with From My Company’s VAT Registration Assistance?

VAT registration typically completes within 10 to 30 working days after HMRC receives a correct application. From My Company’s VAT Registration Assistance verifies the required documents and submits the application to reduce processing delays.

What documents do I need for VAT Registration Assistance from From My Company?

Prepare proof of identity for directors/owners, business proof (invoices or contracts), bank details, and turnover evidence. From My Company’s VAT Registration Assistance uses these documents to verify eligibility and complete the HMRC registration.

Can From My Company register my business for VAT if turnover is below £85,000?

Yes. Businesses with turnover below £85,000 can voluntarily register; From My Company’s VAT Registration Assistance will assess benefits, register the business, and configure records for digital VAT compliance. Voluntary registration may enable VAT recovery on purchases and improve business credibility.

How does From My Company ensure my VAT registration meets MTD requirements?

From My Company’s VAT Registration Assistance configures compatible accounting software and maps required digital fields to meet MTD for VAT rules. The service verifies digital links and prepares systems for API submissions to HMRC.

What are the costs involved when using From My Company for VAT Registration Assistance?

Fees vary by scope basic registration, software setup, and bookkeeping mapping are priced separately; From My Company provides an itemised quote after assessing your business needs. The service outlines any ongoing costs for digital compliance and accounting integrations.