Brunei residents can structure income through a UK company without double tax exposure by ensuring tax residency, transfer pricing, and controlled foreign company (CFC) rules are addressed; they must rely on Brunei–UK tax principles and seek professional tax rulings to secure non-UK taxation on retained foreign-source profits.

What determines whether a Brunei resident pays tax in the UK or Brunei?

A company’s tax liability depends on the company’s residency, management location, and source of income. The UK taxes companies resident in the UK and companies with a UK permanent establishment. Residency is determined by central management and control, typically where board decisions occur. Income source rules classify revenues as UK-source or foreign-source for corporation tax and withholding tax assessment.

Most Brunei-resident controllers avoid UK corporate residency by keeping board meetings, directors, and strategic control outside the UK. They treat the UK company as a non-resident entity for UK corporation tax where lawful. Brunei’s domestic tax rules then determine whether profit distributions and retained profits are taxable in Brunei. Proper governance, documented meeting minutes, and local director arrangements help demonstrate non-UK management.

How does the UK tax system treat non-UK resident companies?

Non-UK resident companies pay UK tax only on UK-source profits or profits attributable to a UK permanent establishment.UK corporation tax applies to profits arising from UK activities. A non-resident company with sales to UK customers or UK-based operations may have UK-source income. A UK permanent establishment (fixed place of business or branch with significant activity) creates a taxable presence. Transfer pricing rules require arm’s-length pricing for cross-border transactions to prevent base erosion.

Brunei residents must segregate UK activities from overseas functions. They should prepare transfer pricing documentation, maintain separate accounting, and avoid UK permanent establishments by locating sales, logistics, or service delivery outside the UK. This reduces the risk of UK taxation on foreign-derived profits.

Read our articles, Can Brunei Residents Open UK Companies? 2026 Breakdown and Build a Tax-Efficient UK Company from Brunei with Form My Company.

Can the Brunei–UK tax relationship prevent double taxation?

A tax residency analysis and available reliefs determine double taxation outcomes; the UK and Brunei do not have a comprehensive double taxation agreement (DTA) as of 2026. Because there is no bilateral DTA, taxpayers rely on domestic reliefs and unilateral relief mechanisms. The UK grants relief for taxes paid abroad where income is taxable in the UK; Brunei’s tax regime applies domestic rules for foreign income inclusion or exemption. Absence of a DTA increases the importance of structuring to establish primary taxing rights clearly in one jurisdiction.

Brunei taxpayers should document the source of each income stream and claim unilateral reliefs where applicable. They must also consider Brunei’s territorial tax features: Brunei primarily taxes on-source activities and offers allowances for certain offshore income. Professional tax advice is essential to map taxation outcomes before profit distribution.

Which corporate structures work best for Brunei residents seeking tax efficiency?

A private UK limited company with non-UK resident directors and clear operational separation commonly provides tax efficiency while limiting exposure. Using a UK limited company limits shareholder liability and isolates UK-source operational risk. Retaining strategic control and decision-making outside the UK supports non-resident company status. Alternatively, a UK LLP typically taxes partners individually and can create UK tax exposure for UK-sourced partner activity.

Companies should adopt documented governance: appoint non-UK resident directors, hold regular board meetings outside the UK, and keep decision-making records. They should also maintain arm’s-length commercial agreements for services, royalties, and management fees to support transfer pricing positions.

How do transfer pricing and intercompany agreements affect double taxation risk?

Proper transfer pricing and written intercompany agreements allocate profits to the jurisdiction that provides value, reducing disputes and double taxation risk. Transfer pricing rules require that related-party transactions reflect market terms. Documentation must demonstrate how pricing was set and why value-creating activities occur in a specific jurisdiction. Intercompany service agreements, licensing agreements, and supply contracts must list responsibilities, pricing method, and performance metrics.

Three verification steps help: document functional analysis, select comparables for pricing, and prepare contemporaneous transfer pricing reports. These steps substantiate why profits sit with the entity performing the critical functions, reducing challenges from UK tax authorities and limiting overlapping tax claims.

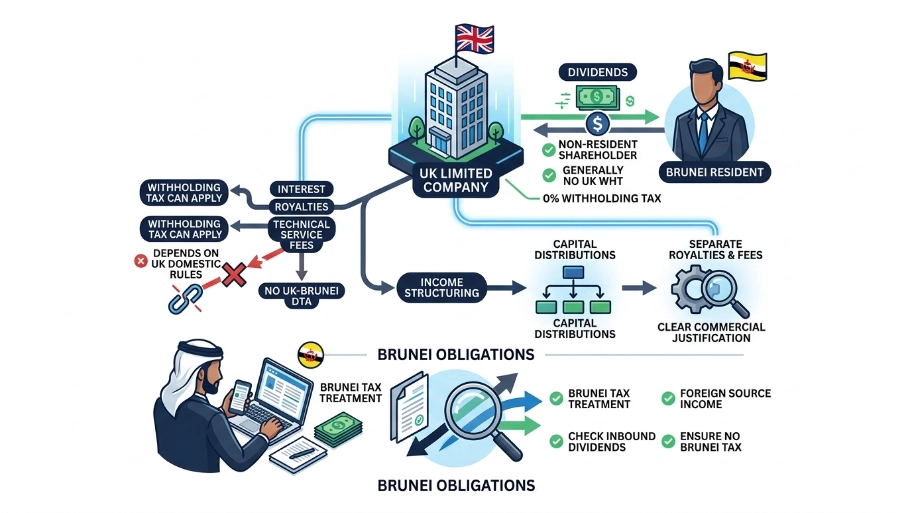

What role do withholding taxes and distributions play for Brunei residents?

Withholding taxes apply to specific UK payments; dividends from a UK company to non-UK residents are generally not subject to UK withholding tax. The UK does not impose withholding tax on dividends paid to non-resident shareholders. However, withholding tax can apply to interest, royalties, or technical service fees depending on domestic rules and any applicable treaty. Since there is no UK–Brunei DTA, withholding exposure depends on UK domestic rules and the nature of payments.

Brunei residents should structure remote receipts as capital distributions where lawful, and separate royalties or service fees with clear commercial justification. They must also check Brunei’s tax treatment of inbound dividends and foreign-source income to ensure distributions do not trigger Brunei taxation.

When do Controlled Foreign Company (CFC) rules affect a UK company owned by Brunei residents?

UK CFC rules apply when UK-resident companies control low-tax foreign entities; they do not typically apply to non-UK resident companies owned by foreign residents.CFC rules target UK parented groups to prevent profit shifting to low-tax jurisdictions. For Brunei residents owning a standalone UK company, CFC concerns are minimal because the UK company sits inside the UK tax net if resident. CFC rules are more relevant when UK-resident entities hold foreign subsidiaries in low-tax jurisdictions.

If a structure involves a UK-resident holding company with Brunei subsidiaries, CFC provisions require profit attribution to the UK parent when artificial arrangements reduce UK tax. Companies must model ownership chains to ensure no unintended CFC exposure arises.

How should Brunei residents document substance and governance to avoid reclassification?

Maintain independent director roles, hold board meetings outside the UK, and record minutes proving strategic decisions occurred abroad. Tax authorities assess central management and control by examining where high-level decisions are made. Practical steps include appointing resident directors in Brunei or another non-UK location, conducting meetings in those jurisdictions, and keeping supporting records: agendas, minutes, and travel records. Operational functions such as payroll, accounting, and contract negotiation should align with the claimed jurisdiction.

Audit trails must match the claimed substance. Shareholder agreements, employment contracts, and bank account locations provide additional evidence. Strong documentation counters reclassification risk and supports the tax position in both jurisdictions.

Explore our Bangladesh guides,

What Bangladeshi Applicants Face When Registering a UK Company: Documents, Delays, Approval Odds.

What practical steps ensure tax-compliant income structuring from Brunei through a UK company?

Register the company correctly, document non-UK management, implement transfer pricing, and obtain professional tax opinions. Step 1: Register a UK limited company and maintain corporate records.

Step 2: Appoint non-UK resident directors and hold board meetings outside the UK.

Step 3: Prepare transfer pricing policies and intercompany agreements for cross-border transactions.

Step 4: Maintain separate accounting, prepare audit-ready minutes, and keep bank accounts consistent with operational claims.

Step 5: Obtain written tax advice or rulings to confirm the anticipated tax treatment in both jurisdictions.

These steps provide an evidence trail for tax authorities and support a defence against double taxation claims. They also align the structure with MOFU intent: evaluation and validation before a commercial decision.

Brunei residents can limit double tax exposure by ensuring the UK company is non-resident for UK tax or by segregating UK-source income and documenting substance. Careful governance, transfer pricing, and professional tax rulings reduce overlap between UK and Brunei tax claims. From My Company provides incorporation and compliance support tailored to Brunei clients to implement these controls efficiently and with audit-ready documentation.

Frequently Asked Questions

Can Brunei residents open a UK company without living in the UK?

Yes, Brunei residents can open a UK limited company without UK residency. From My Company supports non-UK residents by handling registration, director appointments, and compliance for Brunei clients.

What tax rules apply to Brunei residents using a UK company for income?

Brunei residents must follow UK corporation tax rules for UK-source profits and Brunei’s territorial tax rules for foreign income. From My Company provides Brunei-specific guidance to structure income and avoid double tax exposure.

How do Brunei residents verify identity for UK company registration?

Brunei residents verify identity using government-issued ID, passport scans, and address validation documents. From My Company processes these Brunei-specific verification steps securely for non-UK resident directors.

Do Brunei residents need a UK bank account for their company?

Brunei residents can operate a UK company with non-UK bank accounts if they avoid a UK permanent establishment. From My Company advises Brunei clients on banking options that support tax-efficient structures.

What compliance steps must Brunei residents follow for a UK company?

Brunei residents must file annual accounts, confirm statements, and maintain director records with the UK Companies House. From My Company delivers Brunei-focused compliance support to keep UK companies active and audit-ready.