Open a Business Bank Account

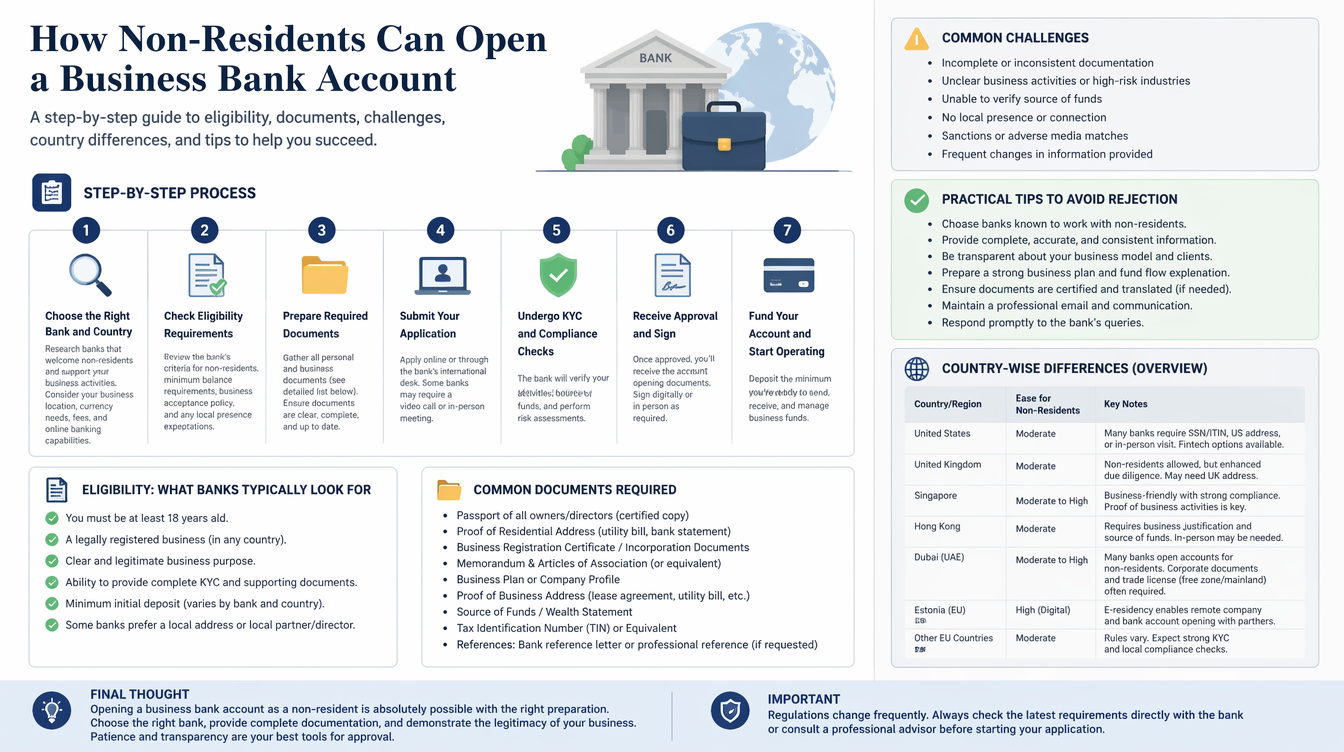

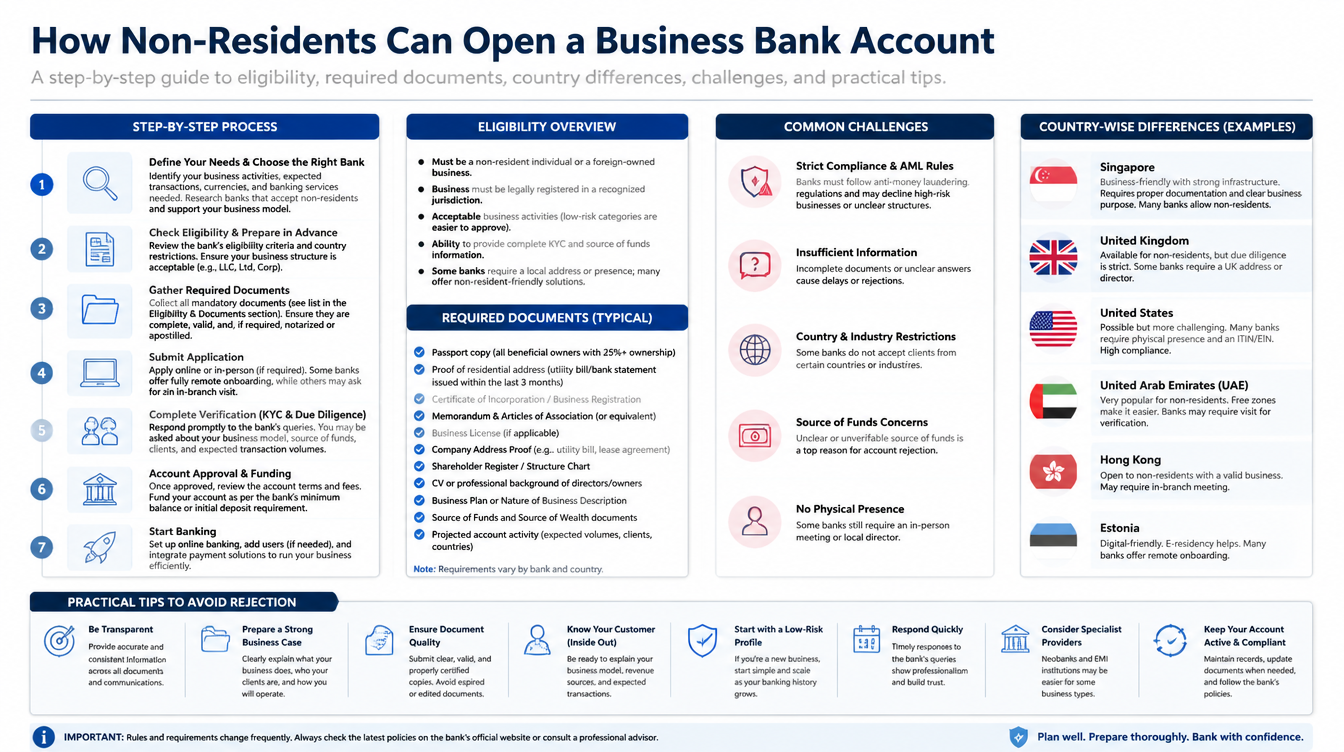

Opening a business bank account as a non-resident is often the moment overseas founders discover just how strict UK banking rules can be. The good news is that thousands of non-residents open UK business accounts every year, and the process is far more manageable once you know how to prepare. At Form My Company, we help international founders form their UK companies and connect them with banking partners that welcome non-resident applicants. In this guide, we walk you through the practical steps of applying, so you know exactly what to do at each stage.

Because requirements can change and providers update their criteria, this guide focuses on the process in principle, and we recommend checking specific terms directly with any provider before applying.

Before You Apply: Understand Your Realistic Options

The single biggest mistake non-residents make is applying to the wrong type of provider first. Most UK high street banks such as Barclays, Lloyds, NatWest, and HSBC generally expect at least one director to live in the UK and hold a UK residential address, and some may require an in-person branch visit. This is largely due to strict anti-money-laundering (AML) and Know Your Customer (KYC) rules. For a non-resident applying from abroad, this often means these providers aren’t a realistic starting point.

That’s why most non-residents apply to digital and fintech providers designed for remote onboarding. Providers like Wise Business, Revolut Business, Tide, and Airwallex accept non-resident directors, offer fully online applications, and can typically approve applications within days rather than weeks.

Step 1: Get Your UK Company Fully Set Up First

You cannot open a UK business account without a UK company, so this is the essential foundation. That means:

- Incorporating your UK limited company with Companies House. You’ll receive a Certificate of Incorporation and a unique company registration number (CRN), which every banking provider will ask for.

- Setting up a UK registered office address. As a non-resident, you can’t use a home address abroad. We provide a compliant Bolton BL1 address in our Non-Residents package.

- Completing director and PSC records. Every director and Person with Significant Control (PSC), typically anyone owning 25% or more, needs to be recorded correctly on the Companies House register. Banks verify these details during onboarding, so accuracy from day one matters.

Get this foundation right and your banking application will move far more smoothly. Get it wrong and even minor inconsistencies (like a mismatched address or date) can cause delays or rejection.

Step 2: Prepare Your Documents in Advance

Almost every provider asks for the same core documents. Preparing them properly before you start the application saves significant time:

- Certificate of Incorporation and CRN. Proof your UK company is officially registered.

- Valid photo ID. A current passport is the most widely accepted document, needed for all directors and PSCs.

- Proof of address. A recent utility bill or bank statement (usually issued within the last three months). Whether a non-UK address is accepted varies by provider; digital fintechs are generally more flexible than high street banks.

- Business activity information. A clear description of what your business does, expected transaction volumes and currencies, and often a website, storefront, or social media presence.

- Board resolution or authorisation letter. Sometimes needed if the applicant isn’t a director.

Tip: make sure names, dates, and addresses match across every document. Mismatched details are the single biggest cause of application delays.

Step 3: Choose the Right Provider for How You’ll Trade

The “best” provider depends on how your business actually operates. As a general guide:

For international trade and multi-currency operations, providers like Wise Business or Airwallex tend to be strongest, thanks to their mid-market exchange rates and local receiving accounts in multiple currencies.

For UK-focused operations, Tide or Revolut Business often suit well, offering fast setup and low-cost UK banking.

For FSCS deposit protection on larger balances, providers like Tide (via ClearBank) offer FSCS cover, which some non-residents value particularly for holding capital.

Step 4: Complete Identity Verification

Once you begin the application, you’ll need to complete KYC identity verification, which is a legal requirement for every UK business account. For digital providers, this is fully remote, typically involving:

- Uploading photos of your passport or ID. Follow the app’s instructions carefully; blurry or off-angle photos are a common cause of delays.

- Completing a selfie or liveness check. Usually done through a mobile app, checking that you’re a real person matching your ID.

- Verifying your proof of address. Upload a clear photo or scan of your utility bill or bank statement.

- Confirming business details. Answer questions about your business activity, expected transactions, and ownership structure.

Digital providers can often complete verification within one to a few working days, though more complex ownership or higher-risk jurisdictions can take longer, up to around 10 working days.

Step 5: Understand the FSCS vs E-Money Point Before Depositing

Before you start moving money in, it’s worth understanding a distinction that isn’t obvious from provider marketing. Fully licensed banks offer FSCS deposit protection on eligible balances up to the scheme’s limit. E-money providers (like Wise) are FCA-authorised and safeguard customer funds, but those funds sit outside FSCS. Neither is wrong, but it matters when deciding where to hold larger balances. Many non-residents use both types of provider: a fintech for day-to-day operations and multi-currency payments, and a fully licensed bank account for reserves.

Step 6: Set Up Your Account for Trading

Once approved, get the basics in place quickly:

- Connect accounting software. Link to Xero, QuickBooks, or FreeAgent to keep bookkeeping clean from day one.

- Activate currencies you’ll use. For multi-currency accounts, activate the currencies you’ll invoice in or pay in.

- Order your business debit card. Where available, so you can spend from your balance directly.

- Connect payment gateways. If you sell online, link your gateway (like Stripe or Shopify Payments) to your new account.

Common Problems Non-Residents Run Into (And How to Avoid Them)

A few issues come up repeatedly, and they’re largely preventable:

- Being rejected by a high street bank due to residency requirements. Fix: start with a non-resident-friendly digital provider rather than a traditional bank.

- Application delays from mismatched documents. Fix: check every name, address, and date matches across your Companies House records, ID, and proof of address before applying.

- Rejection due to your business category. Fix: check the provider’s acceptable use policy against your business activity (some restrict adult goods, gambling, crypto, and other categories) before you apply.

- Slow verification because of missing information. Fix: respond promptly to any provider request for extra information, and check your email regularly during the review.

- Assuming approval is guaranteed. Fix: final decisions always rest with the provider based on their risk checks. A well-prepared application significantly improves your chances but doesn’t guarantee acceptance.

How Form My Company Helps

We take the biggest hurdle out of the process. First, we form your UK limited company quickly and correctly, giving you the Certificate of Incorporation, company registration number, and registered office address you’ll need for any banking application. Second, we introduce you to banking partners suited to non-resident founders, so you’re not searching alone or navigating unfamiliar providers by yourself. Final account approval always rests with the provider, but our support significantly smooths the path.

Open Your Business Bank Account from Anywhere Today

Opening a business bank account as a non-resident is far more achievable than most founders realise, once you know how to prepare. With a properly formed UK company, the right choice of provider, and a well-organised application, most non-residents can be trading with a UK business account within days. With Form My Company, getting your company formed and finding suitable banking is quick and fully supported. Get started today, and check current provider terms before applying to be sure it’s the right fit.

Frequently Asked Questions

Can I open a UK business bank account as a non-resident?

Yes. There’s no law preventing it, though most high street banks require UK-resident directors. Digital providers like Wise, Revolut, Tide, and Airwallex accept non-residents and offer remote onboarding, which is why most overseas founders use them.

What documents do non-residents need to apply?

You’ll typically need your Certificate of Incorporation, company registration number, UK registered office address, valid photo ID such as a passport, recent proof of address, and business activity information. We provide the UK registered office address in our Non-Residents package.

Do I need to visit the UK to open an account?

Not with digital and fintech providers, which typically offer fully remote onboarding via a mobile app or secure web platform. Traditional high street banks may still require in-person verification, which is why most non-residents don’t start with them.

How long does it take to open the account?

Digital providers often approve applications within days, sometimes hours, once verification is complete. More complex ownership structures or higher-risk jurisdictions can take longer, up to around 10 working days. Traditional banks are typically much slower.

Why do applications get rejected?

The most common reasons are residency requirements at high street banks, mismatched details across documents, business categories restricted by the provider’s acceptable use policy, or incomplete verification. Preparing a well-documented application significantly reduces these risks.

Is my money protected in a UK business account?

It depends on the provider. Fully licensed banks offer FSCS deposit protection on eligible balances. E-money providers like Wise safeguard funds but sit outside FSCS. Many non-residents use both types depending on what they hold in each.

Do I need a UK company before applying for a business account?

Yes. Virtually every provider requires a UK-registered company to open a UK business account. We form your UK limited company and provide a compliant registered office address, giving you the credentials most providers ask for.