IR35 and How Does It Affect Contractors

IR35 is one of the most talked-about and often misunderstood topics in UK contracting. If you work through your own limited company, understanding it is essential, because your IR35 status directly affects how you’re taxed and how much you take home. At Form My Company, we help contractors set up their limited companies correctly, and in this guide we explain what IR35 is, how it works, and what it means for you, in plain English.

Because IR35 is complex and the consequences of getting it wrong are significant, this guide explains the principles, and we strongly recommend a specialist IR35 assessment or contractor accountant for your specific contracts.

What Is IR35?

IR35, also known as the off-payroll working rules, is UK tax legislation designed to tackle what HMRC calls “disguised employment.” It targets contractors who work like an employee but use a limited company, or personal service company (PSC), to pay less tax, and seeks to reclaim the additional Income Tax and National Insurance they would have paid as an employee.

In simple terms, IR35 asks a question: if you stripped away your limited company, would you look like an employee of your client, or like a genuine independent business? The answer determines your tax treatment.

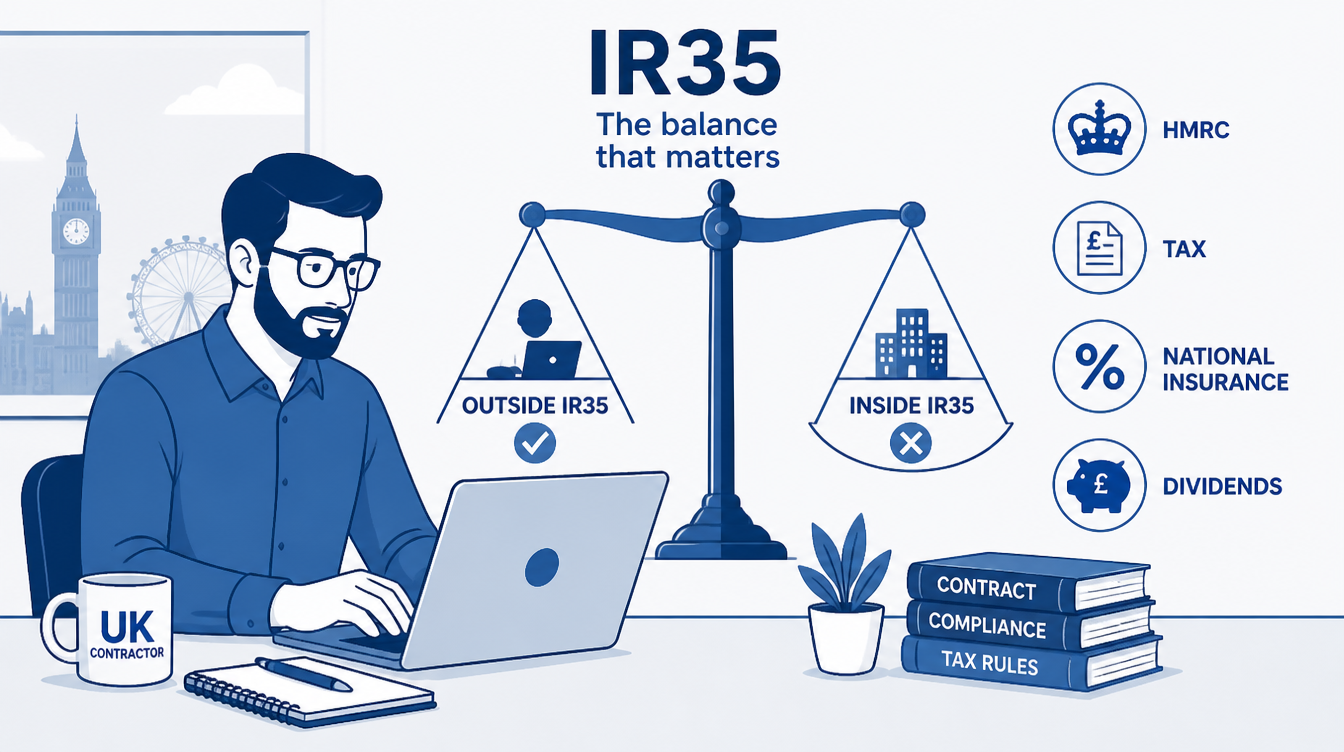

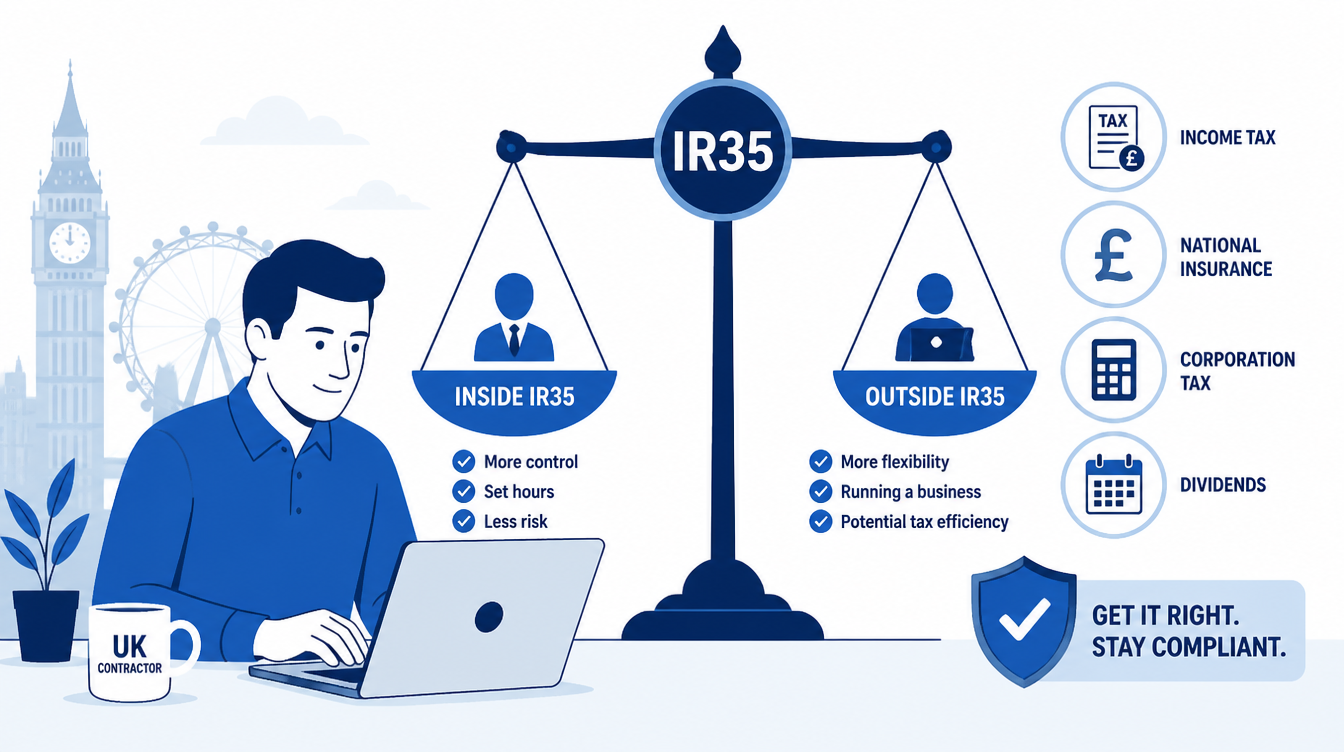

Inside IR35 vs Outside IR35

Your IR35 status falls into one of two categories, and the difference matters enormously for your finances.

- Inside IR35 means HMRC considers you an employee for tax purposes. Inside IR35 means PAYE-style deductions apply at source, so Income Tax and National Insurance are taken much like an employee’s, reducing your take-home pay.

- Outside IR35 means you’re operating as a genuine business. Outside IR35 means you operate through a limited company, paying Corporation Tax on profits and drawing a mix of salary and dividends. This is the more tax-efficient position, which is why establishing genuine outside-IR35 status matters so much to contractors.

The Three Tests HMRC Uses

There’s no single factor that decides your status. HMRC and employment tribunals assess IR35 status using three tests rooted in employment law, and no single test is decisive, as status is determined by the overall picture of the working relationship. The three key areas are:

- Control. How much say does the client have over how, when, and where you work? The more control they exert, the more the arrangement looks like employment.

- Substitution. Could you send a qualified substitute to do the work in your place? A genuine, unfettered right to substitute another person is one of the strongest indicators of self-employment, though the key word is genuine.

- Mutuality of obligation (MOO). Is the client obliged to offer you work, and are you obliged to accept it? An ongoing expectation of work points toward employment, whereas genuine contractors typically work on specific projects with defined ends.

Crucially, your actual working practices matter as much as your written contract. HMRC focuses on how you actually work, not just what the contract says, so if your day-to-day role looks like employment, no amount of clever wording will protect you.

Who Decides Your IR35 Status?

This depends on the size of your end client, and it’s an area that recently changed.

For medium and large private sector clients, and all public sector bodies, the client decides your status. These clients must issue a Status Determination Statement (SDS) to contractors, setting out whether the contract is inside or outside IR35 and why.

For small private sector clients, and clients based wholly overseas, responsibility sits with you. PSCs engaged by small companies, or by engagers based wholly overseas, are responsible for their own IR35 decision-making under Chapter 8, and the decision-maker must demonstrate reasonable care.

The Important 2026 Changes

Two recent changes are worth every contractor’s attention.

First, the small company thresholds increased. From 6 April 2026, the limits are turnover not exceeding £15 million (up from £10.2 million), a balance sheet total not exceeding £7.5 million (up from £5.1 million), and no more than 50 employees. The practical effect is significant. Some clients who currently have to make IR35 determinations will drop out of scope, and responsibility for getting the status right will swing back to the contractor’s PSC for those engagements. If you work for a smaller client, you may now be responsible for your own status. If you were previously assessed as inside IR35 by a medium-sized client who is now small, that determination no longer applies to future work, and you must make a fresh assessment.

Second, the cost of being outside IR35 changed slightly. The IR35 status rules did not change in April 2026, but dividend tax rose on 6 April 2026, which directly affects how much an outside IR35 contractor takes home. The impact is modest but real. The basic dividend rate went from 8.75% to 10.75% and the higher rate from 33.75% to 35.75%, which narrows the outside IR35 take-home advantage but does not remove it.

How IR35 Affects Your Take-Home Pay

The financial difference between the two statuses is substantial. Outside IR35, you can pay yourself tax-efficiently through a salary-and-dividends mix and manage your own taxes through your company. Inside IR35, you’re taxed much like an employee through PAYE, with noticeably less take-home pay and less flexibility. This is why so much attention goes into establishing and defending genuine outside-IR35 status, and why it’s the single biggest factor in whether a limited company is worthwhile for a given contract.

What Happens If You Get It Wrong?

IR35 carries real risk. Incorrect determinations can lead to HMRC investigations, disputes, backdated tax bills, and substantial penalties, with investigations often covering several years and being lengthy and stressful. The exposure can be serious. HMRC can assess up to 20 years of back taxes and NIC in cases of deliberate non-compliance, plus interest and penalties. This is exactly why keeping accurate records of your contracts and working practices, and getting professional advice, is so important.

How to Protect Your Position

While the specifics need a specialist, contractors can generally protect themselves by getting both their written contract and their working practices reviewed for IR35 compliance, keeping detailed records that demonstrate genuine independence, assessing each engagement individually since your status can differ between contracts, reading any SDS carefully rather than treating it as a formality, and challenging a determination you believe is wrong. A contractor accountant or IR35 specialist can guide all of this and represent you if HMRC comes calling.

How Form My Company Helps

We handle the foundation, getting your contractor limited company set up quickly and correctly, with a professional UK registered office address, identity verification support, and banking introductions. IR35 assessment itself is best handled with a specialist accountant, and with your company formed properly and good advice in place, you’re well positioned to contract with confidence. Get started with your formation today.

Frequently Asked Questions

What is IR35 in simple terms?

IR35, or the off-payroll working rules, is UK tax legislation that checks whether a contractor working through a limited company is genuinely self-employed or effectively an employee for tax. Your status determines how you’re taxed.

What’s the difference between inside and outside IR35?

Inside IR35 means you’re taxed like an employee through PAYE, with lower take-home pay. Outside IR35 means you operate as a genuine business, paying Corporation Tax and drawing salary and dividends, which is more tax-efficient.

What three tests does HMRC use for IR35?

Control, substitution, and mutuality of obligation. No single test decides your status; HMRC looks at the overall picture, and your actual working practices matter as much as your written contract.

Who decides my IR35 status?

For medium and large private sector clients and public sector bodies, the client decides and issues a Status Determination Statement. For small private sector clients or wholly overseas clients, you determine your own status.

What changed with IR35 in 2026?

From April 2026, the small company thresholds rose, so more contractors working for smaller clients now assess their own status. Separately, dividend tax rose in April 2026, slightly narrowing the outside-IR35 take-home advantage.

What happens if my IR35 status is wrong?

An incorrect determination can trigger HMRC investigations, backdated tax, interest, and penalties, potentially covering many years. This is why accurate records and specialist advice are strongly recommended.

Does working through a limited company avoid IR35?

No. IR35 specifically applies to contractors working through a limited company or PSC. Your status depends on the reality of your working relationship, not simply on having a company.