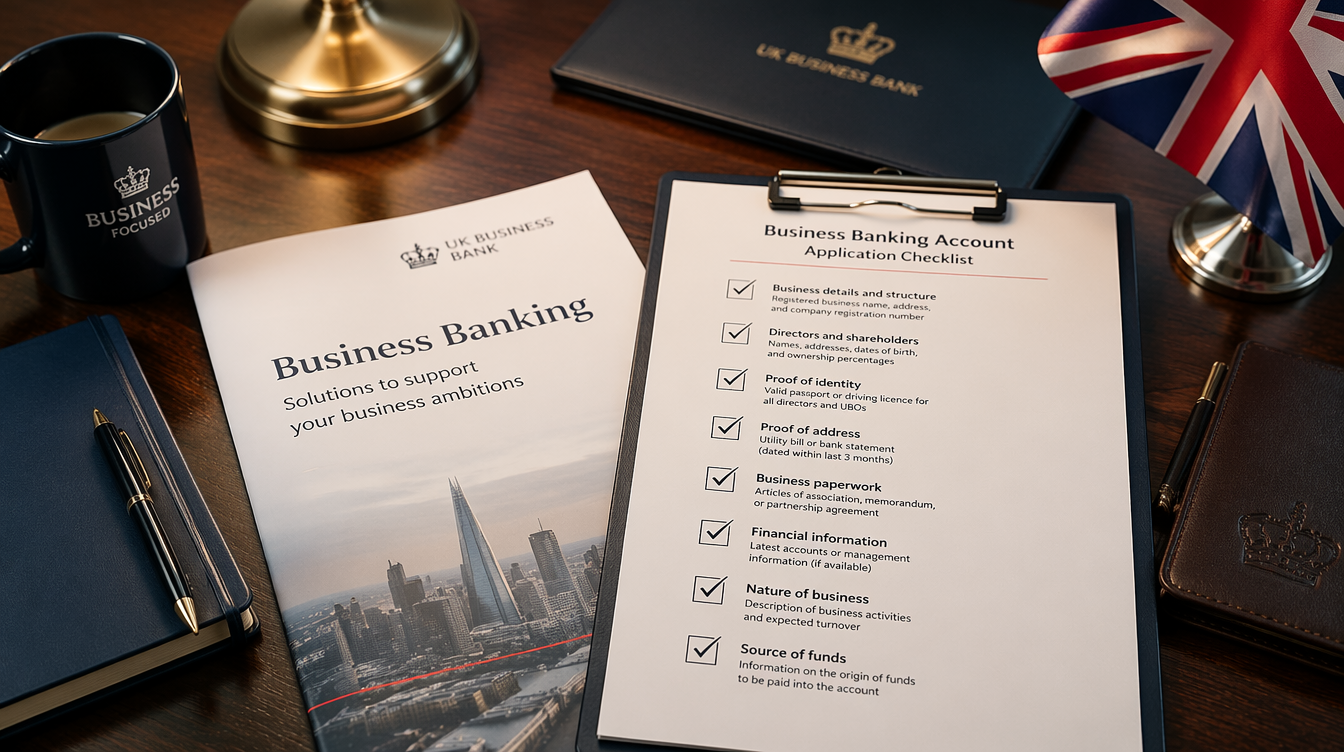

Open a UK Business Account

Getting rejected or delayed on a business bank account application is almost always down to one thing: paperwork. Missing documents, mismatched details, or unclear information can hold your application up by weeks. The good news is that most providers ask for the same core set of documents, and preparing them properly before you apply gives you the best chance of fast approval. At Form My Company, we help founders form their UK companies and connect them with banking partners suited to their needs. In this guide, we walk you through exactly which documents you need, both for UK residents and non-residents.

Because specific requirements vary slightly between providers and can be updated, this guide focuses on the core documents almost every provider asks for, and we recommend checking the exact list with your chosen provider before applying.

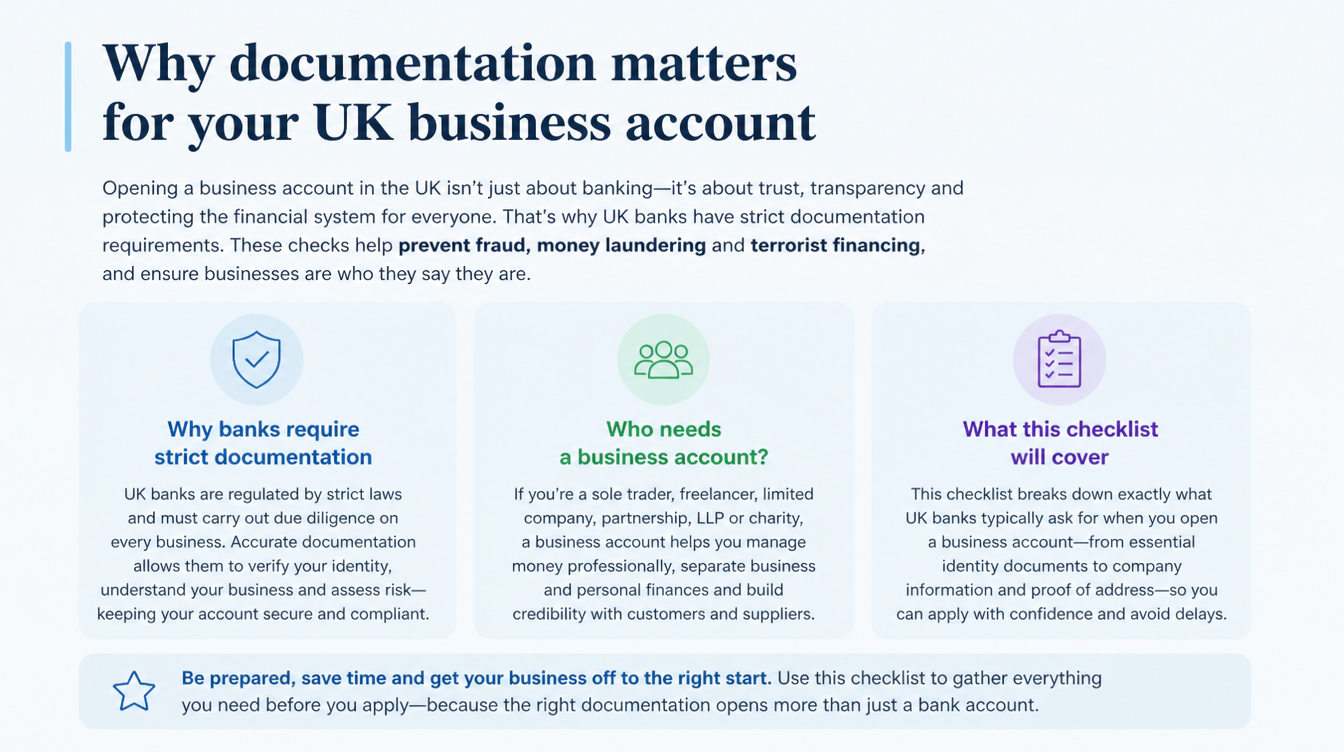

Why UK Business Accounts Ask for So Many Documents

Before we get into the checklist, it helps to understand why the paperwork matters. UK banking is heavily regulated, and providers must comply with strict anti-money-laundering (AML) and Know Your Customer (KYC) rules. This means verifying who you are, who really owns and controls the business, and what the business actually does. Every document you provide is helping the bank confirm one of those three things. A well-prepared application makes the checks easy and quick. A patchy one raises questions and slows things down.

The Core Documents Every Provider Asks For

Whichever provider you apply to (high street bank, digital fintech, or e-money account), you’ll almost always be asked for these:

1. Certificate of Incorporation and Company Registration Number (CRN)

This is the official Companies House document confirming your UK limited company exists and shows its unique company registration number. It’s the foundation of your application. Providers use this to verify your company is real, active, and properly registered. If you’ve formed your company with us, this is delivered digitally as part of your incorporation.

2. Company Details and Trading Address

You’ll need to supply:

- Registered company name (exactly as on Companies House)

- Company registration number (CRN)

- Registered office address (a UK address, which we provide in our Non-Residents package)

- Trading address, if different from the registered office

- Company structure (limited company, LLP, and so on)

Everything must match your official Companies House records exactly. Even small mismatches like an extra space or a shortened name can cause delays.

3. Director and Shareholder Information

Providers need details of everyone who runs and owns the company:

- Full names and dates of birth of all directors

- Home addresses and contact details

- Details of shareholders, particularly anyone who’s a Person with Significant Control (PSC), typically anyone owning 25% or more of shares or voting rights

Accurate PSC information is essential, as it goes to the heart of AML compliance.

4. Valid Photo ID

Every director and PSC will need to provide a valid, in-date government-issued photo ID. Most providers accept:

- Passport (most widely accepted worldwide)

- UK driving licence

- National identity card, depending on the provider

The document must be clear, unexpired, and match the details you’ve supplied. Blurry or off-angle photos are one of the most common causes of verification delays with digital providers.

5. Proof of Address

You’ll need a recent proof of address for each director and PSC. Providers typically accept:

- Recent utility bill (gas, electricity, water)

- Recent bank statement

- Council tax bill (UK residents)

- Rental agreement or mortgage statement

Documents usually need to be dated within the last three months. Non-residents may find some providers accept international proof of address (digital fintechs are generally more flexible), while others require a UK address.

6. Business Activity Information

Providers want to understand what your business actually does:

- Clear description of your products or services

- Your main sales channels (marketplace, own website, offline, and so on)

- Expected transaction volumes and average payment sizes

- Currencies you’ll receive and send in

- Countries you’ll trade with, particularly if there’s any cross-border activity

Some providers also ask for a link to your website or an online presence. Having a professional website ready significantly speeds up verification.

7. Selfie or Liveness Check

Digital providers typically use a mobile app to verify you’re a real person matching your ID. This is usually done as part of the application by:

- Taking a selfie

- Following a short video prompt (turning your head, blinking)

It’s quick, but only works if the lighting is good and your ID photo is clear.

Extra Documents That May Be Required in Some Cases

Depending on your business structure, ownership, or activity, providers may ask for additional documents:

Memorandum and Articles of Association. The formal documents outlining how your company is run.

Shareholder register. A record of who owns the shares in the company.

Board resolution or authorisation letter. If the person applying isn’t a director, they’ll need documented authority to open the account on the company’s behalf.

Additional company documents. Particularly for LLPs, partnerships, or more complex ownership structures.

Tax registration information. Some providers may ask about VAT registration if applicable.

Source of funds documentation. For larger initial deposits, providers may want to understand where the money is coming from.

These extras are usually only needed in specific situations, but it’s worth knowing they can come up.

Additional Documents for Non-Resident Applicants

If you’re a non-resident director, you’ll usually need the same core documents, but a few areas need extra care:

Passport rather than national ID. A passport is the most universally accepted photo ID for non-residents.

International proof of address. Some providers accept this happily; others prefer UK proof, so check before applying. Digital fintechs like Wise, Revolut, and Airwallex are generally more flexible than high street banks.

A UK registered office address. Your company needs one, which we provide in our Non-Residents package. Without it, you won’t get through virtually any application.

Clearer business rationale. Non-resident applications sometimes attract more scrutiny, so a well-explained business description and online presence help significantly.

If you’re a foreign director based abroad, digital providers are almost always the practical route, since most high street banks require UK-resident directors.

Common Documentation Mistakes That Cause Delays

Preventable problems that hold up applications include:

- Mismatched names or addresses across documents (fix: check every detail matches your Companies House records exactly)

- Expired ID (fix: check your passport or driving licence is in date well before applying)

- Blurry ID photos or poor lighting (fix: take clear, well-lit photos following the app’s instructions)

- Old proof of address, older than three months (fix: get a fresh utility bill or statement before applying)

- Missing PSC information (fix: make sure your Companies House PSC register is up to date and matches your application)

- Vague business descriptions (fix: write a clear one-paragraph summary of what you actually do)

Getting these right upfront often makes the difference between approval in a day and delays of a week or more.

Quick Checklist to Prepare Before You Apply

Before hitting “apply” on any provider, make sure you have:

- Certificate of Incorporation and CRN

- Company registered office address (UK)

- Full names, dates of birth, and addresses for all directors and PSCs

- Valid photo ID for each director and PSC (passport preferred)

- Recent (under three months old) proof of address for each director and PSC

- A clear, one-paragraph business description

- Estimated monthly transaction volumes and currencies

- A website or online presence link, if you have one

- Details of expected international activity, if applicable

Have all of these ready before you start, and your application will move as smoothly as possible.

How Form My Company Helps

We take the biggest hurdle out of the process by giving you the foundation every banking application needs. Form your UK limited company with us and you get your Certificate of Incorporation, company registration number, and a UK registered office address in Bolton BL1 as part of our Non-Residents package, plus identity verification support. From there, we introduce you to banking partners suited to your business, so you’re not searching alone. Final account approval always rests with the provider, but a well-prepared application significantly improves your chances.

Get Your Documents Ready and Apply Today

Opening a UK business bank account comes down to preparation more than anything else. With the right documents ready, a properly formed UK company, and a clear business description, most founders (both UK-based and non-resident) can move from formation to trading within days. With Form My Company, getting your company formed and finding suitable banking is quick and fully supported. Get started today, and check the exact document requirements with your chosen provider before applying.

Frequently Asked Questions

What documents do I need to open a UK business bank account?

You’ll typically need your Certificate of Incorporation and CRN, UK registered office address, director and PSC details, valid photo ID (usually a passport), recent proof of address, and a clear description of your business activity. Some providers ask for additional documents in specific cases.

Do I need to provide ID for all directors?

Yes. All directors and Persons with Significant Control (PSCs), typically anyone owning 25% or more, need to provide valid photo ID and recent proof of address as part of KYC verification. This applies at almost every provider.

What counts as proof of address?

Usually a recent utility bill (gas, electricity, water), bank statement, council tax bill, or rental agreement, typically dated within the last three months. Requirements vary slightly by provider, so check before applying.

Can non-residents use non-UK proof of address?

It depends on the provider. Digital fintechs like Wise, Revolut, and Airwallex are generally more flexible about accepting international proof of address than high street banks, which often require UK proof.

What is a PSC and why does it matter for banking?

A Person with Significant Control (PSC) is anyone owning or controlling more than 25% of the company. Providers verify PSC details during onboarding as part of KYC and AML checks, so accurate Companies House records are essential.

Why do providers ask about my business activity?

As part of AML compliance, providers must understand what your business does, expected transactions, and countries you’ll trade with. A clear business description significantly improves approval chances and speeds up verification.

What’s the fastest way to get approved?

Preparation. Have your Certificate of Incorporation, company details, ID, proof of address, and business description all ready before applying, and check that names and details match exactly across every document. This alone avoids most delays.