UK employers register for PAYE within 3 days of the first employee payment. They deduct income tax and National Insurance Contributions (NICs). Employers maintain records, report via Real Time Information (RTI), and comply with minimum wage and pension auto-enrolment rules. From My Company provides PAYE Registration Assistance to meet these deadlines.

What Does PAYE Registration Entail for New UK Employers?

PAYE registration requires notifying HMRC online within 3 working days of the first employee pay. Submit business details, employee numbers, and payment start date. HMRC issues a PAYE reference and tax code.

New employers access the HMRC Government Gateway portal. They create an account if none exists. The form captures employer type, address, and contact information. HMRC processes applications instantly during business hours.

PAYE stands for Pay As You Earn. This system collects income tax and NICs directly from wages. Employers act as HMRC collectors. Registration activates this obligation.

Failure to register triggers penalties. HMRC fines £100 per month for late notification. Repeat delays increase charges to £400 per month. Accurate registration prevents these costs.

From My Company streamlines this process through PAYE Registration Assistance. Experts verify submissions and secure the reference number fast.

When Must Employers Start Deducting Taxes and NICs?

Employers deduct income tax and employee NICs from the first payroll run. Employers pay employer NICs at 13.8% on earnings above £175 weekly per employee. Submit full payment to HMRC by the 22nd of the following month.

Payroll software calculates deductions automatically. Basic rate tax sits at 20% on earnings from £12,571 to £50,270 annually. Higher rate applies above that threshold.

Employee NICs apply at 8% on earnings between £12,571 and £50,270. Rates drop to 2% above £50,270. Employers add their NIC share without deducting from wages.

RTI mandates reporting payroll data on or before each pay date. Full payment deadlines align with bank holidays. Use HMRC’s Basic PAYE Tools for small teams under 9 employees.

Late payments incur 0.5% daily interest on overdue amounts. HMRC issues assessments for underpayments. Precise calculations avoid these charges.

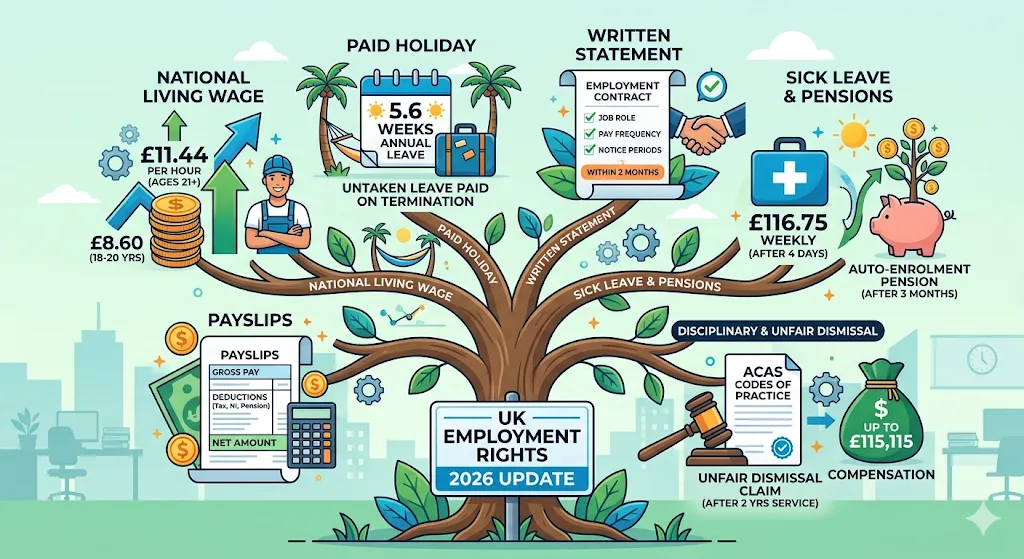

What Employment Rights Do UK Workers Gain in 2026?

Employees receive statutory minimum wage, holiday pay, and sick leave entitlements. Employers provide written statements of terms within 2 months of start. Workers qualify for auto-enrolment pensions after 3 months.

National Living Wage rises to £11.44 per hour for ages 21+ in April 2026. Younger workers follow scaled rates: £8.60 for 18-20 year-olds.

Annual leave totals 5.6 weeks, pro-rated for part-time staff. Employers pay the untaken holiday on termination. Sick pay kicks in after 4 consecutive days at £116.75 weekly.

Employers issue itemised payslips showing gross pay, deductions, and net amount. Statements detail job role, pay frequency, and notice periods.

Disciplinary procedures follow the ACAS codes. Unfair dismissal claims arise after 2 years’ service. Tribunals award compensation up to £115,115.

How Do Employers Comply with RTI Reporting Rules?

Submit RTI via HMRC-compatible software on or before every payday. Report full payment summaries monthly by the 22nd. Corrections file as needed through payroll systems.

RTI replaced annual returns. Each submission includes earnings, tax, NICs, and student loan data. HMRC uses this for real-time compliance checks.

Software vendors like Sage or Xero integrate directly. Test submissions before live payroll. Starters and leavers require special FPS entries.

HMRC audits 1 in 10 payrolls annually. Errors trigger compliance notices. Accurate RTI reduces inspection risks.

Keep payroll records for 3 years. HMRC requests data during enquiries. Digital storage suffices if accessible.

What Pension Auto-Enrolment Duties Apply to Employers?

Assess all workers on payday. Enrol eligible employees into a qualifying pension scheme. Contribute a minimum 3% of qualifying earnings as the employer share.

Staging dates ended in 2018, but new employers trigger assessment immediately. Eligible workers earn over £520 weekly, aged 22 to State Pension age.

Qualifying earnings range from £6,240 to £50,270 annually. Total contribution reaches 8%, with the employer’s minimum at 3%.

Opt-out windows last one month. Re-enrol non-joiners every 3 years. Use HMRC’s free pension dashboard for compliance.

Penalties for non-compliance start at £400 fixed plus 0.75% of payroll. Escalating fines reach unlimited amounts. Explore the costs in our article:

The Cost of PAYE Assistance vs. Potential HMRC Penalty Fees.

Which Records Must Employers Maintain for Compliance?

Retain payroll records, including payslips, RTI submissions, and payment proofs for 3 years. Store employee contracts, tax codes, and P45/P60 forms securely.

HMRC requires evidence of deductions and payments. Digital records work if backed up. Paper copies optional for small firms.

Employee files include right-to-work checks. Verify visas or passports for non-UK nationals. Update records on status changes.

68% of SMEs face HMRC enquiries yearly. Proper records resolve issues fast. Neglect leads to estimated assessments.

Annual P60S summarise tax year totals. Issue by 31 May. P45S transfer on leaving.

Also explore,

Difference Between PAYE and Self-Assessment for New Founders

How to Pay Yourself a Salary as a UK Limited Company Director

What Happens with Right-to-Work Verification?

Check right-to-work documents before employment starts. Use an online service for digital checks. Retain copies for 2 years after employment ends.

Five document types suffice: passports, biometric residence permits, and visa shares. Manual checks follow Home Office lists.

Employers face £20,000 civil penalties per illegal worker. Criminal charges apply for knowing hires. Recheck sponsored workers annually.

68% of checks are now digital via GOV.UK. Automation reduces errors. Three methods are validated: manual scan, online portal, and the employer checks app.

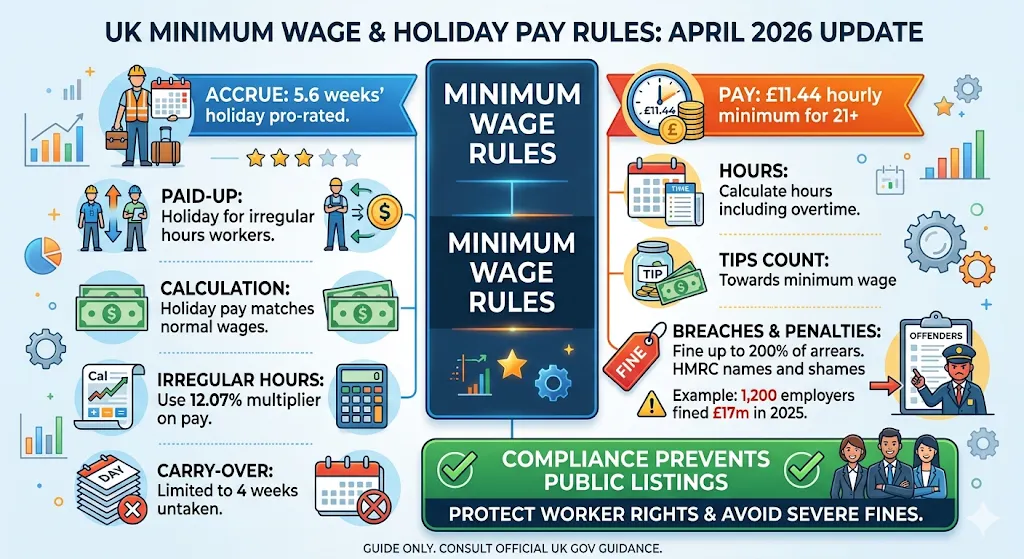

How Do Minimum Wage and Holiday Pay Rules Operate?

Pay at least £11.44 hourly for 21+ from April 2026. Accrue 5.6 weeks’ holiday pro-rated. Paid-up holiday for irregular hours workers.

Calculate hours including overtime. Tips count towards minimum wage. NMW breaches fine up to 200% of arrears.

Holiday pay matches normal wages. Irregular hours use 12.07% multiplier on pay. Carry-over limited to 4 weeks untaken.

HMRC names and shames offenders. 1,200 employers fined £17m in 2025. Compliance prevents public listings.

What Are the Penalties for Non-Compliance in 2026?

Late PAYE registration fines £100-£400 monthly. Payroll errors incur daily interest at 2.75%. Employer NIC underpayments add surcharges.

HMRC issues determination notices for unreported tax. Appeals limited to 30 days. Tribunals uphold 85% of decisions.

Status determination disputes rise 20% yearly. IR35 rules tax contractors as employees if misclassified. Fines double on repeat offences.

Pension non-enrolment penalties escalate automatically. Escalate to tribunals after £4,000.

Get expert support for your first UK HMRC PAYE registration through From My Company’s guidance.

From My Company handles these obligations via PAYE Registration Assistance. Services ensure timely setup and compliance.

UK employer responsibilities centre on PAYE registration, tax deductions, RTI reporting, and worker rights in 2026. Deadlines enforce precision. Records sustain audits. From My Company delivers PAYE Registration Assistance for seamless compliance. Act within 3 days of first pay.

Frequently Asked Questions

What is PAYE registration for UK employers?

PAYE registration notifies HMRC of your role as an employer to deduct income tax and National Insurance from employee wages. New UK employers must register online via the Government Gateway within 3 working days of the first pay. From My Company offers PAYE Registration Assistance to handle this process accurately.

How long do I have to register for PAYE after hiring my first employee?

Register for PAYE within 3 working days from the first employee payment date to avoid penalties. Late registration incurs £100 monthly fines, escalating for delays. From My Company’s PAYE Registration Assistance ensures timely submission and compliance.

What documents are needed for PAYE registration in the UK?

Provide business details, employer address, employee count, and first pay date through HMRC’s online form. No physical documents upload, but verify Government Gateway access. PAYE Registration Assistance from From My Company verifies all details for smooth approval.

What are the penalties for late PAYE registration?

HMRC imposes £100 fixed penalty per month for late PAYE registration, rising to £400 after 3 months. Interest accrues on unpaid tax at 2.75% annually. From My Company’s PAYE Registration Assistance prevents these costs with expert handling.

Can From My Company help with PAYE setup for new employers?

Yes, From My Company’s PAYE Registration Assistance manages full HMRC notification, reference issuance, and initial setup. Services include form completion and deadline compliance for seamless payroll start. This supports UK employers in meeting RTI reporting from day one.