PAYE handles employee payroll taxes deducted by employers before payment. Self-Assessment requires self-employed individuals to calculate and pay their own income tax and National Insurance directly to HMRC annually. New founders choose based on business structure and income sources.

What Is PAYE, and When Do New Founders Use It?

PAYE stands for Pay As You Earn. Employers operate PAYE to deduct income tax and National Insurance from employee wages before paying them. Founders use it when hiring staff or becoming directors with salaries.

PAYE processes payroll taxes automatically. HMRC collects taxes through this system. Employers register for PAYE within 3 months of hiring the first employee.

New founders activate PAYE for salaried directors. Directors count as employees under UK tax rules. The company deducts tax at source.

PAYE covers Class 1 National Insurance contributions. Employees pay 12% on earnings between £12,570 and £50,270 annually. Employers add 13.8% on top.

Founders register via HMRC’s online portal. Registration takes 10 minutes. Approval arrives within 5 working days.

PAYE ensures real-time tax reporting. Employers submit a Full Payment Submission monthly. This reconciles payroll data with HMRC records.

What Is Self-Assessment and Who Needs It as a Founder?

Self-Assessment is HMRC’s system for individuals to report and pay income tax and National Insurance themselves. Founders use it for sole trader profits, dividends, or rental income without employer deductions.

Self-Assessment demands annual tax returns. Individuals file by 31 January following the tax year. Taxpayers calculate liability using HMRC forms.

New founders file if self-employed. Sole traders report business profits minus expenses. Threshold starts at £1,000 trading income.

Dividends trigger Self-Assessment. Founders taking dividends from their limited company declare them. Dividend allowance sits at £500 for 2025/26.

HMRC penalises late filers. Fines start at £100 for returns up to 3 months late. Interest accrues on unpaid tax.

Online filing dominates. 95% of taxpayers use the HMRC portal. Paper returns face rejection after 2019.

How Do PAYE and Self-Assessment Differ in Tax Calculation?

PAYE uses real-time tax codes from HMRC to deduct precise amounts monthly. Self-Assessment requires manual profit calculations and tax estimates with payments on account twice yearly.

PAYE applies cumulative tax codes. HMRC adjusts codes yearly based on prior returns. Code 1257L allows £12,570 tax-free.

Self-Assessment aggregates all income sources. Founders add salary, dividends, and profits. Personal allowance reduces by £1 for every £2 over £100,000.

PAYE is deducted instantly from wages. No end-of-year surprises occur. Self-Assessment demands provisional payments by 31 January and 31 July.

68% of UK SMEs mix both systems. Founders with salaries use PAYE. Dividend income shifts to Self-Assessment.

PAYE ignores non-wage income. Founders declare dividends separately regardless. Self-Assessment captures everything in one return.

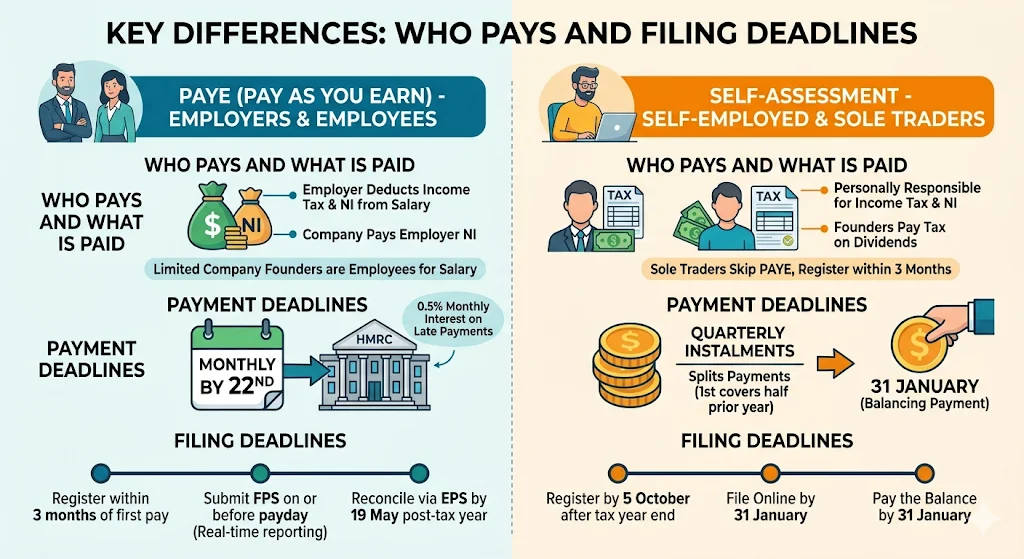

What Are the Key Differences in Who Pays and Filing Deadlines?

Employers remit PAYE taxes monthly by the 22nd. Self-employed individuals pay quarterly instalments and file annually by 31 January. Founders pay personally under Self-Assessment.

PAYE payments hit HMRC by payment deadlines. Automated payroll software handles 80% of submissions. Late payments incur 0.5% monthly interest.

Self-Assessment splits payments. First instalment covers half the prior year’s liability. Founders estimate accurately to avoid underpayments.

Limited company founders receive salaries via PAYE. The company pays employer NI. Founders handle personal tax on dividends via Self-Assessment.

Sole traders skip PAYE entirely. They register for Self-Assessment within 3 months of trading. HMRC sends unique taxpayer references.

Deadlines bind both. PAYE real-time reporting runs year-round. Self-Assessment closes the loop annually.

PAYE Filing Timeline

- Register within 3 months of first pay.

- Submit FPS on or before payday.

- Reconcile via EPS by 19 May post-tax year.

Self-Assessment Filing Timeline

- Register by 5 October after the tax year end.

- File online by 31 January.

- Pay the balance by the same deadline.

When Must New Founders Choose PAYE Over Self-Assessment?

New founders choose PAYE when paying salaries to employees or themselves as directors. Use Self-Assessment exclusively for sole trader profits or untaxed dividends.

Hiring triggers PAYE registration. One employee demands compliance. Founders avoid £100 daily fines for non-registration.

Director salaries require PAYE. Companies House records confirm director status. Salaries above £12,570 activate deductions.

Dividends bypass PAYE. Shareholders report via Self-Assessment. Tax rates hit 8.75% basic, 33.75% higher.

Sole traders select Self-Assessment. No employer exists. Profits fund personal tax bills.

Limited companies blend systems. PAYE covers payroll. Self-Assessment handles dividends and other income.

Transition carefully. Switching from sole trader to limited company demands a PAYE setup. Deregister Self-Assessment if fully salaried.

For seamless PAYE setup, explore PAYE Registration Assistance to register correctly and avoid penalties.

What Compliance Risks Arise from Mixing PAYE and Self-Assessment?

Incorrect PAYE setup leads to HMRC audits and backdated NI payments. Self-Assessment errors trigger £100 fines plus 5% tax penalties. Founders face both if mishandling salaries and dividends.

PAYE non-compliance costs rise fast. HMRC audits recover unpaid employer NI at 13.8%. Interest compounds daily.

Self-Assessment underpayments incur surcharges. Over £1,300 owed adds 5% after 30 days late. Larger sums double to 10%.

Founders overlook dividend caps. Allowance drops to £500. Excess taxes at 39.35% for additional rate payers.

PAYE demands accurate RTI submissions. Errors flag HMRC reviews. 72% of audits stem from payroll discrepancies.

Self-Assessment requires records. HMRC demands 6 years of invoices and receipts. Non-compliance voids deductions.

Learn more about selecting specialists in

What to Look for in a UK Payroll and PAYE Setup Specialist.

How Do Costs Compare for New Founders Using PAYE vs Self-Assessment?

PAYE adds employer NI at 13.8% plus software fees averaging £20 monthly. Self-Assessment incurs accountant fees of £150–£500 yearly with no employer costs.

PAYE burdens companies directly. Employer contributions total £4,380 on a £50,000 salary. Employees see their net pay reduced.

Self-Assessment saves on NI for dividends. No Class 1 contributions apply. The effective rate drops to 27% combined.

Software varies. PAYE tools like Xero charge £24 monthly. Self-Assessment uses free HMRC calculators.

Accountants charge per return. Sole traders pay an average of £ 250. Limited company founders add £400 for corporation tax.

Time costs mount. PAYE monthly filings take 2 hours. Self-Assessment annual prep averages 10 hours.

Founders scale efficiently. PAYE suits growing teams. Self-Assessment fits lean startups.

Also explore,

Common PAYE Myths Debunked for Small UK Business Owners

How to Pay Yourself a Salary as a UK Limited Company Director

What Steps Do Founders Take to Set Up PAYE Correctly?

Register online via HMRC Government Gateway. Provide company details and expected payees. Receive PAYE reference in 5 days for payroll runs.

Access the portal first. Create accounts for the employer and employees. Verify with unique taxpayer references.

Gather employee data. Collect NI numbers and addresses. Assign tax codes from HMRC P45 forms.

Run payroll software. Input hours and rates. Generate payslips compliant with itemised requirements.

Submit Real Time Information. File before or on payday. HMRC processes instantly.

Pay taxes promptly. Use BACS to the HMRC account. Reconcile annually via EPS.

Outsource for accuracy. Services handle registration and ongoing compliance.

Decide today with

our PAYE Assistance Package: Register Your Business Today.

FromMyCompany provides expert PAYE Registration Assistance. The service ensures HMRC compliance from day one. Founders avoid fines through a precise setup.

Frequently Asked Questions

What is PAYE registration assistance?

PAYE registration assistance guides businesses through HMRC’s online portal to set up Pay As You Earn for employee taxes. It includes providing company details, expected payees, and securing a PAYE reference number within 5 working days. FromMyCompany handles verification to ensure compliance from the start.

How long does PAYE registration take for new businesses?

PAYE registration typically completes in 5 working days after HMRC approves the online application. Businesses must apply within 3 months of hiring their first employee or paying salaries. MyCompany’s PAYE Registration Assistance streamlines submission to meet deadlines.

Do new founders need PAYE registration assistance?

New founders require PAYE registration when hiring staff or paying director salaries, as employers must deduct income tax and National Insurance at source. Sole traders skip it, but limited companies comply via HMRC. FromMyCompany offers targeted PAYE Registration Assistance for seamless setup.

What happens if you don’t register for PAYE on time?

Late PAYE registration incurs daily fines up to £100 from HMRC, plus backdated employer National Insurance at 13.8%. Audits recover unpaid taxes with interest. MyCompany’s PAYE Registration Assistance prevents penalties through prompt, accurate filing.

Can FromMyCompany help with PAYE registration and ongoing compliance?

FromMyCompany provides PAYE Registration Assistance covering initial HMRC setup and references. It extends to Real Time Information submissions and payroll reconciliation. Services ensure businesses meet monthly reporting without disruptions.