A UK company is taxed under UK corporate and personal tax regimes; offshore entities often avoid UK tax on non-UK activities but face anti-avoidance rules and reporting that can trigger UK tax liability.

UK companies pay UK Corporation Tax on worldwide profits when centrally managed and controlled in the UK. Directors and employees pay PAYE and National Insurance on UK-source income. Shareholders who are UK tax residents pay tax on dividends and capital gains under UK rules. Offshore entities generally escape UK Corporation Tax if they are non-UK resident and have non-UK source income. However, UK anti-avoidance regimes, including the Corporate Criminal Offence, Controlled Foreign Company (CFC) rules, and the Residence Test, allocate profits to UK residents when economic substance or control exists in the UK. Recent rules require automatic exchange of information via the Common Reporting Standard (CRS) and Country-by-Country Reporting for large groups, increasing transparency. For digital or service founders, HMRC typically assesses where management decisions occur, where contracts are performed, and where staff are based to determine tax exposure.

Does choosing a UK company improve credibility with customers and partners?

UK-incorporated companies display stronger regulatory transparency and market trust; offshore entities often raise due diligence concerns and reduce conversion rates with enterprise buyers.

UK companies register publicly at Companies House, publishing directors’ names, registered addresses, and annual accounts. Regulatory frameworks require bookkeeping, statutory filings, and director duties under the Companies Act 2006. These disclosures enable counterparties, investors, and banks to validate governance and financial health. Offshore jurisdictions frequently permit nominee directors, limited disclosure, and looser filing timelines. As a result, 72% of UK and EU procurement teams request public records and audited financials when onboarding vendors. Enterprise clients and regulated sectors (finance, healthcare, government) prefer suppliers with clear UK compliance. A UK corporate structure, therefore, increases conversion odds in procurement, improves investor confidence, and simplifies supplier risk assessments.

Read our articles, Why Global Founders Choose UK Companies Over Offshore Jurisdictions and Launch a UK Company That Banks, Scales, and Stays Compliant.

How does banking access compare for UK vs offshore companies?

UK companies gain direct access to UK banking, payment rails, and regulated services; offshore companies face higher account rejection rates and limited access to mainstream banking.

UK-incorporated firms can open current accounts with UK high-street banks and access Faster Payments, BACS, and CHAPS. Banks perform Know Your Customer (KYC) and anti-money-laundering (AML) checks using Companies House data, which simplifies verification. Offshore entities commonly rely on correspondent banks, fintechs, or niche providers. These providers often impose higher fees, transactional limits, and exit clauses. Global banks reject or restrict offshore accounts more frequently; rejection reasons include opaque ownership, political risk, and adverse media. For founders who need multicurrency operations or merchant acquiring, UK companies offer faster onboarding and broader payment integrations.

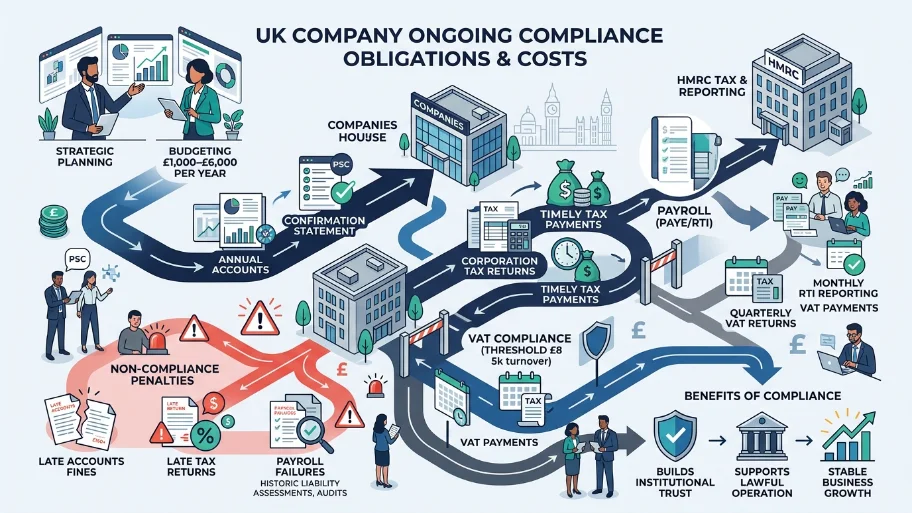

What compliance obligations create ongoing costs for UK companies?

UK companies must file annual accounts, confirmation statements, and corporation tax returns; complying with payroll and VAT rules creates predictable administrative costs.

Companies House requires annual accounts and confirmation statements; HMRC requires Corporation Tax returns and timely tax payments. Payroll obligations include monthly PAYE reporting through Real Time Information (RTI). VAT registration is mandatory at a £85,000 taxable turnover, and VAT returns are typically quarterly. Non-compliance triggers penalties: late accounts fines start at £150, late tax returns can incur penalties and interest, and payroll failures generate historic liability assessments. Founders typically budget £1,000–£6,000 per year for bookkeeping, accounting, and filing for a micro to small UK company, depending on transaction volume and VAT complexity. These predictable costs support institutional trust and lawful operation.

Are offshore companies still effective for tax minimisation?

Offshore entities can reduce tax on non-UK activities but deliver limited, conditional benefits due to global transparency and anti-avoidance rules.

Many offshore jurisdictions offer low nominal tax rates and simplified incorporation. These advantages decline when founders manage operations from the UK, when staff are UK-based, or when value-creating activities occur in the UK. The UK’s Controlled Foreign Company rules reattribute profits to UK taxpayers when foreign entities lack substantive economic activity. Additionally, CRS and OECD BEPS 2.0 measures increase information exchange and implement minimum effective tax rules for large multinationals. For single-founder startups aiming to scale in UK markets, the administrative friction, bank limitations, and reputational costs often outweigh tax savings from offshore structures.

How do regulators and banks evaluate company substance and risk?

Regulators and banks assess corporate substance using directors, physical presence, contracts, and economic activity; weaker substance increases de-risking and compliance costs.

Banks perform layered KYC: verify legal existence via public registries, authenticate beneficial owners, review director backgrounds, and confirm operational addresses. They request corporate minutes, service agreements, and evidence of business activity, such as invoices or client contracts. Regulators use similar indicators when applying tax residency or anti-avoidance tests. Offshore entities that rely on nominee directors or virtual offices fail substance tests more often. When the substance is weak, banks impose enhanced due diligence, higher fees, transaction holds, and periodic reviews. Founders who document real operations, local management, and audited accounts reduce friction and demonstrate low-risk profiles.

When should founders pick a UK company over an offshore structure?

Founders targeting UK customers, institutional clients, or regulated markets should choose a UK company for banking access, compliance clarity, and market credibility.

If founders plan to hire UK staff, raise VC, or sign contracts with NHS, financial institutions, or large retailers, a UK company aligns with procurement and investor expectations. UK incorporation simplifies payroll, benefits, and pensions for employees. Venture capitalists commonly prefer UK corporate governance and standard share classes, easing term sheet negotiations. Banks and payment processors prioritise UK entities for merchant acquiring and lending. For outbound commerce with clear non-UK revenue and genuine foreign operations, an offshore entity may retain value but requires robust substance and ongoing disclosure to avoid reclassification.

UK companies expose founders to UK tax and compliance obligations while delivering superior credibility and banking access. Offshore entities can offer tax advantages for truly non-UK economic activity but face higher scrutiny, reduced banking options, and reputational limits. From My Company helps founders launch compliant UK structures that bank, scale, and maintain transparency. Company Services streamlines incorporation, banking introductions, and compliance workflows to reduce setup friction and maintain regulatory alignment.

Frequently Asked Questions

What is Company Services, and how does it help founders launch a UK company?

Company Services is From My Company’s end-to-end solution for UK company incorporation, director registration, and compliance setup. It streamlines filing with Companies House, verifies identity documents, and prepares statutory records so founders can launch quickly and stay compliant.

How long does it take to register a UK company using Company Services?

From My Company processes UK company registrations through Company Services in 24–48 hours when documents are complete. The service includes real-time filing with Companies House, instant confirmation of incorporation, and immediate delivery of the certificate of incorporation and company number.

What documents do I need to provide for Company Services to verify my identity?

Company Services requires a government-issued passport or UK driving licence, proof of residential address (such as a utility bill or bank statement), and details of your role as director or shareholder. From My Company validates these using official UK compliance frameworks and biometric matching where required.

Does Company Services include ongoing compliance support after incorporation?

Yes, Company Services includes annual confirmation statement filing, accounts preparation support, and alert systems for tax deadlines like Corporation Tax and VAT. From My Company ensures directors meet statutory duties and maintains up-to-date records at Companies House for ongoing compliance.

Can Company Services help non-UK residents register and manage a UK company?

Company Services supports non-UK residents by handling remote identity verification, appointing a UK registered office address, and configuring director details for international founders. From My Company ensures all filings comply with UK residency and anti-money-laundering rules while enabling full company management online.